Global markets summary

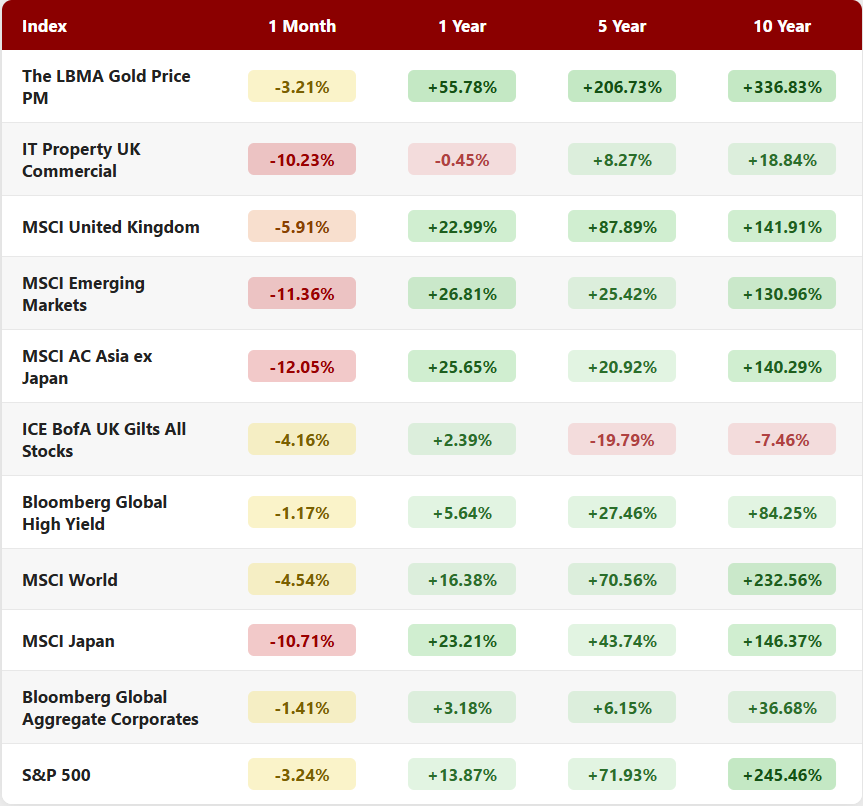

March proved a challenging month for global equities. Escalating tensions in the Middle East drove a sharp rise in energy prices, rekindling inflation fears and pushing volatility higher across financial markets. Despite this pullback, most major markets remain firmly in positive territory over the past twelve months when measured in sterling terms, a reminder that short-term turbulence rarely defines long-term outcomes.

In developed markets, the United States and Japan bore the brunt of the sell-off. Higher oil prices, rising bond yields and renewed concerns over stagflation prompted profit-taking after a period of strong performance. The UK and Europe also retreated during the month, though both continue to deliver solid double-digit gains over the past year. Asia and emerging markets experienced sharper declines. The combination of elevated oil prices, a stronger US dollar and rising global bond yields placed particular pressure on energy-importing economies, triggering a swift unwinding of crowded positions across the region.

Government bonds and investment grade credit also delivered negative returns as expectations for near-term interest rate cuts were scaled back. It is worth noting, however, that the higher yields now available represent a meaningfully more attractive income opportunity for long-term investors than those seen in recent years. Gold, having rallied strongly in prior months, gave back some ground and offered limited protection over the period.

Periods of geopolitical uncertainty are unsettling, but markets have demonstrated remarkable resilience in the face of significant shocks before. Since the onset of the Russia-Ukraine war, through historic interest rate rises and high-profile bank failures, global equities have risen by more than 50%. Examining 14 major geopolitical events over the past 64 years, the S&P 500 has delivered an average forward 12-month return of 9.5%. History, in this respect, tells a consistent and encouraging story.

Our centralised investment proposition is deliberately constructed for environments such as this. Your portfolio is diversified across geographies and asset classes, incorporates built-in inflation protection, and is tilted towards areas we believe are best placed to benefit as conditions stabilise.

The incentives for all parties involved favour de-escalation, and while the precise timing remains uncertain, we are confident that markets will ultimately look through the current period of conflict, as they have done on every previous occasion. We continue to monitor developments closely and remain committed to guiding your wealth through periods of uncertainty with care and conviction. Please do not hesitate to reach out to your adviser if you would like to discuss your portfolio in more detail.

United Kingdom

Despite its exposure to energy and generally being seen as a more defensive market, UK equities underperformed the global benchmark over the month. Large cap names fared much better than mid cap, with the latter more exposed to the domestic economy and the associated negative impact of higher energy prices, inflation and borrowing costs.

Given that economic data is backward looking, there was little to signal how businesses and consumers are feeling about the current situation. However, what we did receive was a string of the lacklustre indicators, suggesting a challenging environment, even before the conflict started.

Growth remained elusive at the start of the period, with GDP flat in January against a consensus expectation of +0.2%, continuing the sluggish trend seen in recent months. Flash PMI data for March offered only modest reassurance. The Composite PMI came in at 51.0, below the 52.8 consensus and well down from 53.7 in February, with both the services and manufacturing components disappointing relative to expectations. While still in expansionary territory, the direction of travel is a concern.

On inflation, the picture remains uncomfortable. Headline CPI held at +3.0% year on year in line with expectations, but core CPI edged up to +3.2%, marginally above consensus. Against this backdrop, the Bank of England opted to hold rates at 3.75% in a unanimous 9-0 vote, citing risks from elevated energy prices, a decision that will have been further complicated by mortgage market disruption, with lenders withdrawing nearly 500 products amid the repricing of rate expectations linked to the Iran conflict.

The labour market showed further signs of softening. The unemployment rate held at a post-pandemic high of 5.2%, while average weekly earnings growth decelerated to +3.8%, with private sector pay growth of just +3.3% falling short of forecasts. This wage moderation may provide some comfort to the MPC but does little to support consumer spending power.

After a better start to the year for cyclical businesses and those with a domestic focus, conflict in the Middle East has halted any burgeoning momentum. The spectre of local elections looms large over the current Government and a change in leadership is unlikely to be taken well by financial markets. This risk, combined with the conflict in Iran and softer economic data led us to moderate our cyclical exposure within the UK Dynamic fund during the month and reappraise our longstanding view on the prospects of a number of domestic businesses.

North America

US equities retreated in March, with the S&P 500 falling just over 3% in sterling terms, leaving the index slightly negative year to date, though it remains close to 14% higher over twelve months following a powerful run through 2025.

The pullback reflected an uncomfortable combination of surging oil prices, rising bond yields and fading expectations for near-term Federal Reserve rate cuts, which together placed valuation pressure on growth-oriented assets and prompted investors to reassess what they are willing to pay for future earnings. Sector performance was sharply polarised: energy stocks were clear beneficiaries as crude moved above 90 dollars per barrel, while technology and other interest rate sensitive areas lagged as higher discount rates weighed on already stretched valuations.

Most economists and strategists characterise this as a mid-cycle correction rather than the end of the equity advance. The US economy remains resilient and earnings growth is still anticipated across most sectors, though a more volatile, rotation-driven environment looks probable as markets contend with persistent inflation risks and uncertainty over the Federal Reserve’s ultimate policy path. It is notable that equity markets have, to a considerable degree, chosen to look through the current conflict, encouraged by the belief that a resolution is close at hand. Rates markets, by contrast, have been considerably quicker to price in the inflation shock. Should the geopolitical situation deteriorate further, there is a risk that equities move to reflect the growth consequences more fully, and current valuations leave limited room for disappointment.

The stronger US dollar provided some welcome relief for sterling-based investors. Having broadly appreciated against the dollar over the past year, sterling reversed course in March, slipping from the mid-1.35s towards the low 1.32s as higher US yields and safe haven demand supported the greenback. Currency gains therefore partially offset the weaker performance of US equities in local currency terms.

The US remains a core allocation within our portfolios, given its market depth, sector diversity and consistent corporate profitability. Near-term performance is likely to be shaped by the trajectory of inflation and the Federal Reserve’s ability to balance persistent price pressures against an already mature economic cycle. We are monitoring developments closely and managing your exposure with both care and conviction.

Europe

European equities spent March caught in the cross‑currents of geopolitics and economics, with the Middle East conflict amplifying an already uncomfortable mix of higher energy prices, rising yields and fragile growth. The renewed disruption around the Strait of Hormuz has been particularly problematic for Europe as a major net energy importer, feeding directly into higher input costs for industry and squeezing real household incomes, at a time when activity data was already pointing to a sluggish backdrop. This has left investors wrestling with a classic stagflationary dilemma: policymakers need to lean against the inflation impulse from dearer oil and gas, yet tighter financial conditions risk tipping a weak economy into recession.

For European equities, this has translated into a sharp pull‑back from recent highs, following a period in which low starting valuations, solid dividend yields and hopes of policy easing had underpinned strong twelve‑month returns. Cyclical and domestically-exposed sectors, such as consumer, real estate and some financials, have been most vulnerable to the deteriorating growth outlook and higher funding costs, while energy has been one of the few clear beneficiaries of the new price regime. At the same time, the debate over how far the European Central Bank may ultimately need to tighten, if the conflict were to escalate and oil prices were to move significantly higher, has added another layer of uncertainty for rate‑sensitive parts of the market.

From our perspective, the key insight is that Europe sits at the sharp end of this energy shock, which makes earnings more sensitive to the evolution of the conflict and to any follow‑through into policy. However, it also means that any credible path to de‑escalation, or even a stabilisation in energy prices, could unlock meaningful upside, given the region’s valuation discount to the United States and generally stronger starting point for bank balance sheets than in the previous crisis. In this environment, a cautious but engaged stance feels appropriate: favouring higher-quality European companies with robust balance sheets and genuine pricing power, keeping overall regional exposure modest relative to risk appetite, and remaining alert to the potential to add on periods of indiscriminate weakness if the macro picture begins to clear.

Rest of the world

Rest of world equities, spanning Japan, Asia Pacific and emerging markets, were at the sharp end of March’s risk aversion. Rising oil prices, a stronger US dollar and higher global bond yields proved a particularly punishing combination for energy-importing and externally-financed economies.

Japanese equities fell by almost 11% in sterling terms, unwinding a meaningful portion of the past year’s gains. Investors weighed the economic cost of higher imported energy against growing concern that the Bank of Japan will eventually be compelled to normalise its ultra-loose monetary policy, tightening financial conditions at precisely the wrong moment in the global cycle.

Elsewhere in Asia, markets such as South Korea and Taiwan, which had been among the strongest performers on the back of enthusiasm for technology and semiconductor demand, gave back ground sharply. Higher discount rates, fears of a global growth slowdown and the prospect of supply chain disruption triggered profit-taking in some of the most widely held names. In India and parts of South East Asia, the combination of higher oil prices and dollar strength raised questions about current account dynamics and inflation, leaving local equities and currencies under pressure even where the underlying domestic growth story remains compelling.

Emerging markets more broadly weakened as hopes for near-term US rate cuts faded. Higher Treasury yields and a resurgent dollar tightened global financial conditions, encouraging an instinctive ‘sell first, ask questions later’ response in the most liquid and widely-owned assets. There is, however, an important distinction worth drawing: commodity-exporting nations, particularly in Latin America and the Middle East, stand to benefit from elevated oil and metals prices. This positive dynamic has been obscured for now by broad risk-off sentiment and currency volatility, but it is not lost on us.

Taking a long-term view, these regions continue to offer genuine appeal. Attractive valuations relative to developed markets, younger demographics and meaningful growth potential all remain intact. March serves as a timely reminder, however, that these markets carry greater sensitivity to energy prices, dollar movements and shifts in global liquidity. Selectivity is therefore paramount: we favour companies and countries with strong balance sheets, healthy external positions and credible policy frameworks, and we are wary of concentration in crowded trades.

While the near-term outlook remains dominated by geopolitical and macroeconomic uncertainty, the indiscriminate selling of recent weeks may yet create opportunities to add exposure to high-quality assets at more attractive valuations.

Fixed income

Fixed income markets endured a bruising March. Rising energy prices and a sharp repricing of interest rate expectations pushed government bond yields materially higher, with UK gilts at the centre of the move. Thirty-year gilt yields posted one of their steepest monthly rises since the Truss-Kwarteng episode, leaving gilts down just over 4% for the month. Across the major central banks, policy rates were held unchanged, but the tone was cautious. The Federal Reserve and the European Central Bank signalled limited scope to ease while energy-driven inflation risks remain elevated, and the Bank of England unanimously held the bank rate at 3.75%, having recently revised its inflation forecasts higher and its growth outlook lower.

Credit markets proved more resilient than sovereign bonds, though they did not escape unscathed. Global investment grade corporate bonds delivered negative returns, with indices down between roughly 0.5 and 4% in sterling terms, as higher underlying yields and modestly wider spreads weighed on prices. The picture was not entirely negative, however. Primary markets in the United States and Europe remained open, with several sizeable transactions successfully placed by high-quality issuers, demonstrating that access to funding for stronger borrowers remains intact. Crucially, the rise in risk-free rates means that all-in yields on investment grade bonds are now materially higher than at any point in the past decade, meaningfully improving the prospective return on offer.

Global high yield and emerging market debt also posted negative returns in March, reflecting higher funding costs, wider risk premia and dollar strength. Both segments nonetheless continue to offer attractive carry and have delivered solid three-year returns as income accumulated since the 2022 repricing compounds over time. Secondary market liquidity in core US and European credit has remained broadly functional, allowing investors to adjust positioning in an orderly manner.

While March brought further short-term pain, the prospective return profile across fixed income has improved considerably. Gilts, government bonds and investment grade credit now offer starting yields not seen for many years, with income set to play a far greater role in driving total returns than it has for much of the past decade. Selectively managed high yield and emerging market debt can contribute further carry within appropriate risk parameters. We continue to manage duration and credit exposure deliberately, and we are well positioned to add interest rate or spread risk when volatility creates the right entry points.

Ask us anything

Ask us anything

Q: What happened to the gold price this month?

A: Over March 2026, gold moved from being one of the strongest performing assets to delivering a sharp negative month. Prices fell significantly from earlier highs as investors reassessed the outlook for interest rates and inflation, after a very strong run in the preceding months. This felt surprising to many because gold is often thought of as a safe haven, but the main driver in March was the change in expectations for interest rates rather than a sudden improvement or deterioration in world events.

The key point is that gold does not pay an income. When government bond yields rise, or are expected to stay higher for longer, investors are effectively being paid more to hold very low risk bonds instead. That increases the ‘opportunity cost’ of owning gold. In March, markets moved to expect fewer and later interest rate cuts, which pushed bond yields and the US dollar higher. A stronger dollar also tends to weigh on the gold price globally, because gold is priced in dollars. At the same time, because gold had risen so far in previous months, many investors decided to lock in profits and reduce positions. These profit-taking flows can accelerate a move lower once certain price levels are broken.

So, while gold is often used as a protective asset, it can still be volatile over shorter periods when interest rate expectations, currencies and investor positioning all shift together. What we think matters more for your portfolio is the longer-term picture. Here, the structural case for gold remains in place. Central banks have been steadily increasing their gold holdings, partly to diversify their reserves away from the US dollar and to reduce the risk that their foreign exchange reserves are affected by political decisions. This gradual move towards holding more gold and slightly less in a single reserve currency is often described as ‘de-dollarisation’, and it provides a supportive backdrop for gold over time.

In addition, the world continues to face elevated geopolitical tensions and fiscal pressures, which keeps the appeal of real assets and diversifiers such as gold. Periods like March are uncomfortable, but they are not unusual for an asset that is influenced by both macroeconomic expectations and investor sentiment. In our view, the recent pullback does not undermine the long-term role of gold as a useful, diversifying and potentially protective element within a well-balanced portfolio.

If there’s a question you’d like to pose to our team, please reply to this email or write to [email protected].

Four key takeaways from March 2026:

• Middle East tensions triggered a global sell-off – rising oil prices reignited inflation fears.

• Rate cut hopes evaporated – all major central banks held rates and signalled no imminent easing.

• Gold fell despite the turmoil – heavy profit-taking after months of gains accelerated the decline.

• The longer-term picture stays relatively positive – most markets remain up double digits over 12 months. History shows the S&P 500 averages 9.5% in the year following major geopolitical events.

MARKET DATA

All performance figures are from FE analytics (as at 31/03/2026) and quoted on a total return basis in pounds sterling.

The Monthly Market Commentary (MMC) is written and researched by Scott Bradshaw, Lauren Hyslop and Jonathon Marchant for clients and professional connections of Mattioli Woods and is for information purposes only. It is not intended to be an invitation to buy, or to act upon the comments made, and all investment decisions should be taken with advice, given appropriate knowledge of the investorʼs circumstances. The value of investments and the income from them can fall as well as rise and investors may not get back the full amount invested. Past performance is not a guide to the future.

Mattioli Woods Limited is authorised and regulated by the Financial Conduct Authority.

Sources: All other sources quoted if used directly, except fund managers who will be left anonymous; otherwise, this is the work of Mattioli Woods.