Global markets summary

May was a constructive month for markets, though the mood was more measured than April’s powerful rebound. US stocks reached fresh record highs, driven by a handful of mega-cap technology companies, even as the ongoing Middle East conflict and disruption to the Strait of Hormuz kept energy prices elevated and reinforced a reflationary mood. Re-accelerating inflation added to the pressure on government bonds and prompted investors to push back their expectations for interest rate cuts.

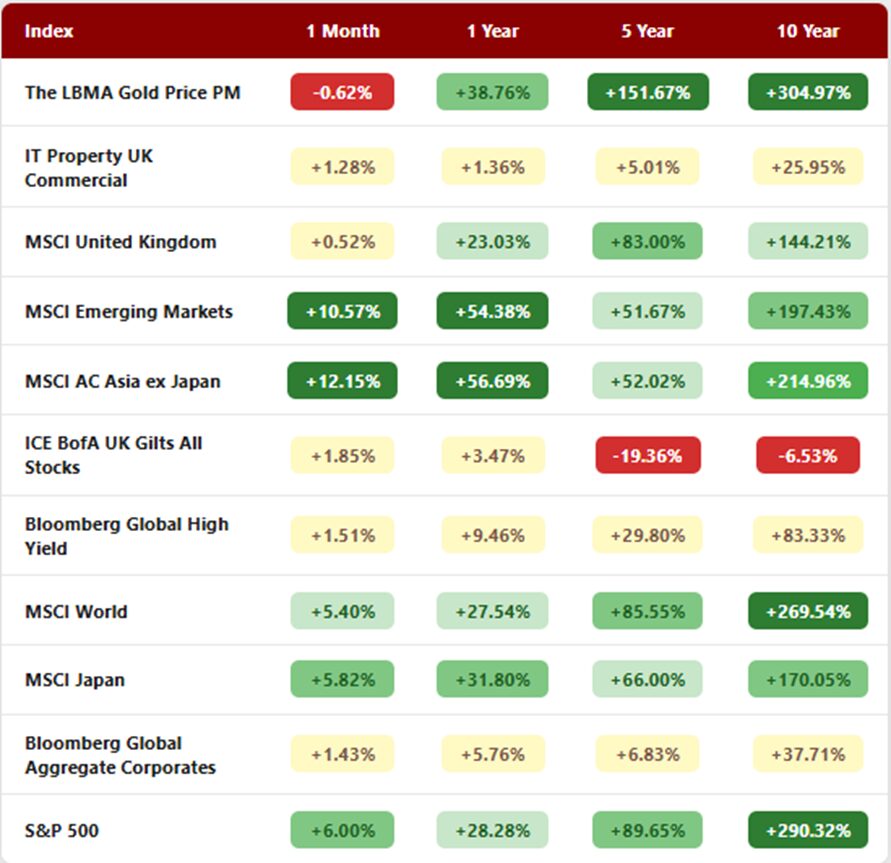

Global equities have delivered solid returns in sterling terms year to date, with Asia among the standout performers. Taiwan and South Korea have led the way, their technology giants powering ahead as the AI-driven semiconductor cycle lifted emerging market indices to record highs.

What is striking is how resilient markets have been in the face of a genuinely difficult backdrop. The AI story remains the primary engine of gains, but it now rests on firmer ground than the early hype cycle suggested. Corporate earnings have started to catch up with the narrative, real-world productivity benefits are becoming measurable, and investment in AI infrastructure continues to grow. Crucially, investors have grown more discerning, rewarding companies where AI spending links clearly to revenue and returns. The result is a broader and more mature trade, and one that has proved robust enough to keep markets climbing even as risks elsewhere have multiplied.

Crude oil remained central to the macro narrative throughout May, with prices staying elevated and prone to sharp moves as US-Iran tensions and the effective closure of the Strait of Hormuz kept supply risks in sharp focus. Gold, though it has pulled back from its peak at the outbreak of conflict, held at historically high levels, continuing to attract demand as a hedge against geopolitical uncertainty and inflation.

As May drew to a close, markets were broadly positive but navigating a narrower path than at the start of the year. Earnings are holding up, the AI growth story shows little sign of fading, and risk assets continue to deliver, yet valuations are stretched and the macro environment has grown more complex. The easy gains from simply owning equities and riding the cycle are giving way to something that requires more careful judgement. Looking ahead, we remain cautiously optimistic on risk assets, keeping a close eye on the interplay between energy prices, inflation expectations and central bank policy, which are likely to be the key determinants of returns in the months ahead.

United Kingdom

UK equities underperformed global peers again in May, as investors weigh the consequences of higher energy prices and domestic political turmoil. The UK economy entered May having delivered an encouraging start to 2026, with first-quarter GDP expanding 0.6% quarter on quarter, in line with consensus. Private consumption, Government spending, and business investment all contributed positively, and prior-year data revisions pushed the year-on-year print to 1.1%, ahead of the 0.8% forecast.

The Iran conflict continues to disrupt energy markets, driving up benchmark interest rates and suppressing business and consumer sentiment. This is now feeding visibly into the hard data. May’s flash composite PMI fell sharply to 48.5 (firmly in contraction territory) against a consensus of 51.6, with services particularly weak at 47.9. Retail sales disappointed on both headline and ex-fuel measures, and the GfK consumer confidence reading, while better than feared at -23, remains deeply negative. BRC retail sales for April were also down 3.0%, the first negative print since November 2024, with clothing a notable drag for the third consecutive month.

Political risk has risen materially alongside these macro pressures. Prime Minister Starmer’s position has been weakened by the Middle East conflict, and the prospect of a leadership change is now a live concern for markets. Andy Burnham is regarded as the most likely successor, though his historic policy positions have unsettled investors. A new leader would likely pursue higher taxes, expanded public ownership, and increased worker rights, all of which risk weighing on business confidence.

On the monetary policy front, the Bank of England is expected to hold rates over the summer, as inflation expectations are gradually re-anchored. Money markets have at points priced in hikes, but the more likely path is one where the BoE sounds cautious while allowing some automatic stabilisation through yields.

Despite the headwinds, there are pockets of resilience worth noting. The housing market has continued to hold up, with Nationwide reporting a 0.4% monthly price rise in April, supported by household balance sheets that are in their strongest shape relative to income in around two decades. Private sector balance sheets more broadly remain healthy, providing a cushion. With calmer political conditions and a potential resolution in the Strait of Hormuz anticipated by later in the year, there are reasonable grounds for cautious optimism.

North America

US equities were one of the main engines of global returns in May, extending the rebound from April’s sharp rally. The drivers were familiar: strong earnings, resilient growth and sustained enthusiasm around artificial intelligence. With aggregate US earnings running some 20% above analyst estimates, investors had good reason to look past the macro noise. The economy is not firing on all cylinders, but it remains in decent shape. Household balance sheets are solid, capital expenditure is elevated, and the base case remains slow but solid growth of around 2.2 to 2.3% this year, with core inflation easing gradually and scope for the Federal Reserve to cut rates later in 2026.

Technology and AI names again led from the front, though the picture beneath the surface is more concentrated than headline index strength implies. Market participation has narrowed to levels not seen since the dot-com era, with AI, semiconductors and mega-cap technology doing most of the heavy lifting. That concentration is worth watching. Should momentum in that small leadership group falter or earnings disappoint, the indices could prove more vulnerable than they appear.

Valuations remain a sobering footnote. The S&P 500 trades at around 21 times forward earnings, with the market pricing in growth of roughly 18% in both 2026 and 2027. Much of that optimism rests on AI delivering as a genuine earnings engine, and with so much index performance riding on a handful of names, any sign that AI spending is not translating into returns on capital could ripple through the broader market quickly.

We held an underweight to US equities earlier in the year, cautious on valuations and the macro outlook. We have since moved to neutral. The US economy’s relative insulation from the energy shock, combined with the continued strength of the AI earnings story, made closing that underweight a compelling call.

Within that, the infrastructure layer of the AI build-out strikes us as particularly interesting and somewhat underappreciated. Data centres, power networks and the physical backbone of the AI economy draw in a wide range of smaller American companies, from specialist engineers to utilities and materials suppliers. These businesses stand to benefit meaningfully from the AI cycle without carrying the valuation premiums attached to the mega-cap names. For sterling investors, the key questions are how much US equity exposure to run, how concentrated to be in AI and mega-cap platforms, and how much dollar exposure to leave unhedged given recent pound strength. In a world of firm sterling and elevated valuations, those decisions carry more weight than they did at the start of the year.

Europe

European equities rose 4.4% in May in sterling terms, bringing year-to-date gains to 6.5%. The region benefited from positive spillovers from the US technology complex and continued global risk appetite, but the eurozone’s status as an energy-importing, manufacturing-heavy bloc left it more vulnerable to elevated oil prices than its US counterpart. Earnings momentum and macroeconomic data remained less compelling, and Europe continues to lag the US over the cycle.

Valuation remains one of Europe’s more compelling features. Broad European benchmarks still trade at a discount to US equivalents on forward earnings and book value, even after the rally from the 2022 lows. That gap is no longer extreme, but it is sufficient to provide some support, particularly if AI-driven enthusiasm remains concentrated in a small group of US names and European earnings continue to recover.

That said, we remain tactically underweight European equities. The central questions are whether the ECB can deliver a gradual easing cycle without reigniting inflation, and whether the earnings recovery proves durable against a backdrop of geopolitical and growth risks. Europe is more exposed than the US to energy prices, industrial demand and events in its near neighbourhood, and any renewed stress around Ukraine, energy supply or internal EU politics could weigh on sentiment quickly. We want to see more evidence that the recovery has genuine legs before adding further exposure.

For sterling investors, Europe nonetheless continues to offer a useful complement to the US: lower valuations, a more balanced sector mix and the potential for a further re-rating if growth surprises on the upside and policy remains supportive. The investment case is improving. It simply needs a little more proof.

Rest of the world

Beyond the US and Europe, May was another strong month across Japan, Asia Pacific and broader emerging markets, with each region telling a distinct but compelling story. Japanese equities extended their remarkable run, building on a powerful 2025 that took both the Nikkei and TOPIX to record levels. First quarter GDP surprised to the upside, earnings were solid, and the structural backdrop remains unusually supportive. Corporate governance reforms continue to push companies towards better capital allocation and shareholder returns, while modest real wage growth is helping domestic demand. Exporters and semiconductor-related businesses have been particular beneficiaries, drawing on both the global AI capital spending cycle and a still-competitive yen.

Asia Pacific ex-Japan carried strong momentum into May on the back of an extraordinary April, when Korea and Taiwan led the regional index to a 15% gain. May was more measured but still positive, with first quarter earnings in the region running at around 40% year on year, heavily concentrated in technology. The fundamental backdrop remains supportive: a softer dollar, expectations of Federal Reserve easing, proactive domestic policy in China and parts of ASEAN, and differentiated growth drivers across AI, green transition and advanced manufacturing. For UK investors, the region delivered strong sterling returns, with the scale of the equity move comfortably overshadowing any currency noise.

Emerging markets more broadly had another standout month, rising around 9.7% against 4.6% for developed markets, again led by Korea and Taiwan. This builds on an exceptional 2025, when emerging markets delivered roughly 33% versus 17% for the S&P 500, their best relative performance since 2017. The case for continued outperformance rests on valuations that remain genuinely attractive at around 14 times forward earnings, improving profitability, and positioning that is still light after a decade of under-ownership. The cycle is being driven by a mix of secular themes, including AI, re-industrialisation and domestic consumption stories in India and elsewhere, alongside cyclical tailwinds from easing global financial conditions. Volatility will remain part of the bargain, but for sterling investors, emerging market allocations have been a significant contributor to multi-asset returns and the structural arguments for the asset class continue to strengthen.

Fixed income

Rising inflation expectations and higher oil prices made May a difficult month for government bonds, pushing yields sharply higher and steepening yield curves, while credit held up well on the back of solid earnings.

UK gilts bore the brunt. The ten-year yield rose sharply, at one point touching above 5%, while the thirty-year reached its highest level in almost three decades, reflecting a combination of energy-driven inflation, fading expectations for Bank of England rate cuts and domestic political uncertainty. US Treasuries told a similar story, with yields pushing back towards cycle highs as markets reassessed the pace of Federal Reserve easing. For the second time in recent months, government bonds failed to provide their traditional cushion against equity volatility, underlining the challenge of finding effective hedges during a reflationary shock. We have kept duration underweight as a result.

In credit, the picture was more encouraging. Sterling investment grade returned broadly flat to mildly negative as rising gilt yields offset stable spreads but carry remained attractive and corporate fundamentals held firm. High yield fared better still, with spreads well supported by low default expectations and healthy balance sheets. Valuations are no longer distressed, but the asset class continues to benefit from the risk-on tone and the search for income.

Globally, investment grade credit benefited from tightening spreads in dollar markets, while global high yield remained one of the better performing corners of fixed income. Emerging market debt had a more mixed month, as higher US yields and a firm dollar offset some of the tailwind from elevated oil prices for commodity exporters. It continues to earn its place as a source of diversified carry, though position sizing warrants care, given its sensitivity to dollar moves and shifts in global risk appetite.

Ask us anything

Q: Why has the AI story come back into vogue so strongly, have the issues raised previously around productivity been resolved? Are we confident that it’s not a bubble?

A: The AI trade has returned with force, but it’s a more mature and better-grounded version of what came before. Understanding why requires a brief look at what went wrong, and what has since changed.

Through late 2024 and into early 2025, markets went through a necessary and healthy reckoning. AI-related stocks had re-rated sharply on the promise of transformational change, but investors began asking harder questions: was all this capital spending actually earning its cost? When would the productivity gains show up in earnings? That scepticism triggered a notable period of underperformance in tech and AI names, with some of the worst relative drawdowns versus the broader market since the 1970s.

What has changed is that the evidence has started to arrive. Technology is now the sector with the strongest positive earnings revisions globally, and a meaningful share of S&P 500 earnings growth is now explicitly tied to AI investment and monetisation rather than expectation alone. Over 90% of businesses report using AI in some form, with productivity improvements of around 40% in certain workflows. Crucially, corporate AI budgets are still growing, not rolling over, with AI-related investment expected to run well into the trillions through 2030.

The market has also grown more discerning. Investors are now distinguishing clearly between AI spending that links tightly to revenue and returns, and spending that looks more speculative. Companies demonstrating this connection have been rewarded; those that cannot are being penalised. The AI trade has also broadened well beyond a handful of model developers and mega-cap platforms. Semiconductors, data centres, power infrastructure, developer tools and vertical software applications with proprietary data are now recognised as distinct and monetisable layers of the same structural theme.

Is it a bubble? The honest answer is that pockets of excess almost certainly exist, and concentration risk remains real. But the broader picture looks less like a bubble and more like a maturing capital cycle, one where the narrative has shifted from “AI will change everything someday” to “AI is already quietly embedded across operations”. Many of the companies benefiting most in 2026 do not even describe themselves as AI businesses. They are simply using it to drive efficiency and margins under the hood.

That is arguably a healthier and more durable foundation than what existed two years ago. The risks are execution and crowding rather than pure speculation, and that is a meaningful distinction.

If there’s a question you would like to pose to our team, please reply to this email or write to [email protected].

Four key takeaways from May 2026:

• Equity markets continued to advance in May, though the pace was tempered compared to the sharp rally that had characterised April.

• The Strait of Hormuz remains restricted to commercial shipping and the world’s oil buffers are nearly exhausted.

• Rising inflation expectations and higher oil prices made May a difficult month for government bonds while credit held up well on the back of solid earnings.

• Asia Pacific ex-Japan carried strong momentum into May on the back of an extraordinary April, when South Korea and Taiwan led the regional index to a 15% gain.

MARKET DATA

All performance figures are from FE analytics (as at 31/05/2026) and quoted on a total return basis in pounds sterling.

The Monthly Market Commentary (MMC) is written and researched by Scott Bradshaw, Lauren Hyslop and Jonathon Marchant for clients and professional connections of Mattioli Woods and is for information purposes only. It is not intended to be an invitation to buy, or to act upon the comments made, and all investment decisions should be taken with advice, given appropriate knowledge of the investorʼs circumstances. The value of investments and the income from them can fall as well as rise and investors may not get back the full amount invested. Past performance is not a guide to the future.

Mattioli Woods Limited is authorised and regulated by the Financial Conduct Authority.

Sources: All other sources quoted if used directly, except fund managers who will be left anonymous; otherwise, this is the work of Mattioli Woods.