United Kingdom - November 2023

This monthʼs theme is later life. Naturally enough, you may have read that and thought ‘old ageʼ, and indeed ‘oldʼ and ‘elderlyʼ (followed by ‘get 30 minutes of moderate exercise …ʼ) usually follow when one searches Google. You will however, read about late cycle economics, old industries etc., and we will be positive about experience and the benefits of wisdom etc.

Starting with the human, most of us have an idea of when ‘later lifeʼ is, maybe even what it looks like, and yet, due to diseases, accidents and indeed improved healthcare and longevity, our assumptions may be some way off. Infant mortality has completely changed in the last century and a bit. The average life expectancy at the turn of the last century was c.65 years, now it is c.85 years. Why does this matter?

It matters for us personally, it matters for our own financial planning (always better to have run out of breath before we have run out of money, if possible?) and it matters significantly for our economies. While we do not have time to consider the ‘age waveʼ in the western world, created and fed by the baby boom, or compare it to Chinaʼs life expectancy ‘explosionʼ (just 50 in 1960, to 78 today), our own longevity changes the economy and vice versa. Letʼs move then to financial matters more broadly.

When is an economic cycle ‘lateʼ, and why does it matter to be conscious of that? A typical economic cycle looks a bit like this: expansion, peak, contraction, trough. As one might imagine, different types of assets do better at different stages. Currency often fluctuates, interest rates and inflation usually play a part at different stages. If one has a later life (old, industrial) business and a younger, exciting but less established business, the chances are they may be successful at different stages, though all businesses can/should benefit at some stage.

The young, dynamic ‘tech-entrepreneurʼ (do they have to be young, is it not possible to be dynamic and not young, and vice versa?) may seem to have many/most things going for them but have they ever run a business/ invested during a downturn, when money cost more to borrow, and not every answer from early investors was ‘yesʼ? Some of the worldʼs very best businesses were of course established and cut their teeth during such time. Equally, those who had the experience gained wisdom (not just information) and remained enthusiastic about their product or service, they dealt equally well with tough times, maybe better. (This description is, to some extent, a Utopian world but is used to make a point.)

Not all old industries are ‘over the hillʼ, just as not all pensioners have stopped working (words chosen carefully there!). Not all new, small businesses will be successful, not all big businesses will fail – in both cases, many will. It is our job, as custodians of other peopleʼs money, to gain and apply wisdom, to consider history, yes, and to shield that very money from a dystopian ending.

We remain happy to invest client money into great UK businesses; some smaller, some larger, some newer, some later life.

North America - November 2023

October proved to be a difficult month for risk assets as bond yields remained elevated and concerns continued to increase around the Middle East. Both the S&P 500 and the Nasdaq – two of the main US equity indices – recorded their worst Octobers since 2018, with the former recording its longest monthly losing run since March 2020. Corporate earnings have been surprisingly robust but expectations for the fourth quarter of this year are being marked down by many as economic conditions tighten. The movement in the bond market means the inversions in the yield curve has now narrowed dramatically, which is usually a sign that recession is not far away. Remarkably, in our view, the consensus is still not that a recession is likely, but we feel there is sufficient evidence for one to continue to be cautiously positioned.

Another sign of the times is the awarding of a significant pay deal to the United Auto Workers union workers. One might contrast Bidenʼs support for the workers with Reaganʼs arguments against unions in the 1980s. So, yet another inflationary force to contend with that might make the landscape resemble the 1970s more than the 1980s. Remember too that inflationary waves usually come in pairs and investors might not have things as easy as they think in terms of conditions normalising. Still, investors are likely to be emboldened by the most recent Federal Reserve statement, which suggests that rate rises may have gone far enough, though parsing the statements from central banks remains a less than perfect science!

Old age can undoubtedly bring wisdom, but the age profile of US politicians is truly remarkable. The average senator is now over 65 years old but Dianne Feinstein recently died having reached 90!

Of course, the US has outperformed stupendously since the financial crisis and left many afraid to bet against its run continuing. We think there is enough of concern – valuations, elevated margins, a lower probability of recession being factored in compared with elsewhere – to question this view. The US government finances are in a truly appalling condition and dismissing this is now looking reckless. Running a budget deficit of 8% in a robust economic environment should make investors nervous about what will happen in a downturn and the idea the situation will somehow not affect sentiment towards US risk assets looks naïve to us.

Sometimes going against the herd can be painful but we believe that playing the US on our terms will bear fruit.

Europe - November 2023

Over the year, we have written extensively about the issues faced by the European economy and stock market. Not to be spared from the risk-off sentiment last month, European stocks recorded their worst month since September 2022. Interestingly, investors are getting increasingly unforgiving in how they react to disappointing results, which is a sign that here, as elsewhere, the mentality has switched. Certainly, it is not the time to announce, as Siemens did, that guarantees are being sought from government, which resulted in a 35% drop in the company share price. Sanofi has been another high- profile example of a severe response to poor news with Renault and ABB also producing less than inspiring numbers.

Forecasts are still for an 8% increase in company earnings for 2024, which looks optimistic to us. There is significant scope for margins to fall from here and we think that a focus on large-cap, quality names make sense given that higher rates will start to impact balance sheets.

There is some encouragement for investors around the fact that the European Central Bank may have ended its tightening cycle after the central bankʼs recent pause but given the possibility for an external shock from energy prices or another source, taking a victory lap looks a bit premature. It is true that recent inflation data from Spain and Germany has been encouraging but thoughts may turn to recessionary concerns rather than inflationary ones soon.

We continue to keep an eye on the sovereign debt position of European countries. Bond yields globally are causing issues for governments, and it can only be matter of time before countries such as Italy start to present challenges to investor thinking. Looser budget rules announced recently (tax cuts and pay rises have been introduced to aid faltering growth) mean the country has attracted focus of late and this is another reminder of how unresolved weaknesses in markets and economies always return in times of stress.

Italy is the country in Europe with the highest old age dependency ratio – that is the number of people over 65 per 100 people of working age. Currently at 57, the number is only set to increase and is a reminder of the challenges ahead for the continent.

No changes to European allocations this month.

Rest of the world - November 2023

October was a negative month for global equities, which was reflected across all the rest of the world regions. As measured by their respective investment association (IA) sector averages, which includes the impact of active management, the average IA Global fund was down -3.5% over October, as concerns over the potential negative impact of higher-for-longer rates swept markets.

The IA Asia Pacific (excluding Japan) sector and IA Global Emerging Markets sectors were similarly down -3.5% and -3.2% respectively. Year to end of October, both sectors continue to lag the IA Global sector, with Chinese equities – along with not being home to the listing of any of the ‘magnificent sevenʼ AI stocks – holding back the region. The IA China/Greater China sector is down -15.8% over this period. As we have previously covered, Chinaʼs economy has struggled to regain momentum following its Covid-19 reopening and debt in its property market remains a headwind. While we have seen more measures to stimulate the economy from Chinese authorities, these have not been significant enough to regain confidence.

Japan has the oldest population in the world, with over 10% of its population aged over 80 (and 29.1% aged 65 and above) according to population data released by the Ministry of Internal Affairs and Communications in September to mark ‘Respect for the Aged Dayʼ. It is perhaps unsurprising that many world records for oldest person to achieve a feat are held by Japanese people, including Shigemi Hirata, who in 2016 (aged 96 and 200 days) became the oldest graduate ever. Mr Hirata received a Bachelor of Arts degree from the Kyoto University of Art and Design, completing a Ceramic Arts Course that he had started aged 85 in 2005.

While China has become more difficult to justify investing in, Japan has been heading in the opposite direction. Despite the IA Japan sector slightly lagging IA Global over the month, it remains ahead over the year to end October, up 3.6% against IA Globalʼs 1.7% return and is over 6% ahead over a year. Continuing evidence that Japan is becoming more focused on shareholder returns and unlocking the value on corporate balance sheets has seen more investors attracted to the region, helped by famous business magnate Warren Buffett giving his stamp of approval following investments.

Completing our tour of the rest of the world, the IA India/Indian Subcontinent sector and IA Latin America sectors are both ahead of IA Global so far this year. India has returned 8.8% despite a negative October and while we like the long-term economic story, this market looks expensive to us especially relative to other markets, which saw us take profit in positions early this year. IA Latin America had the worst October of all the sectors covered, down 4.7%, with the cyclical commodity bias impacted by lower growth expectations. The region does still look attractive to us and we have selective direct exposure in higher-risk portfolios. Latin American economies have benefited from being later in their rate cycle and companies have gained from re-shoring (mainly to Mexico) as companies have looked to rely less on China in their supply chains.

We maintain a healthy position in Japanese equities across portfolios based on our view that better fundamentals, momentum from reforms and foreign investor interest, as well as less restrictive monetary policy all provide opportunities for the market to outperform other regions.

Fixed income - November 2023

Nearly two years after the first interest rate hike of this cycle – a 0.15% rise by the Bank of England (BOE) in December 2021 – we have seemingly reached the end. Over the past month, the BOE, the US Federal Reserve and the European Central Bank (ECB) all confirmed they would hold interest rates at current levels, rather than enacting any further hike. The first two holding for the second consecutive meeting while the ECB halted for the first time, breaking a 15-month hiking streak.

After a relatively sluggish start, as central bankers held to the ‘transitoryʼ inflationary narrative, the pace of rate hikes has been extraordinary – from a historic low of 0.15% in the UK, intended to stimulate the economy through the post-pandemic recovery, via 14 rises to the current 15-year high of 5.25%. Similarly, in the US, we have seen both the fastest and largest pace of rate-hikes in recent history. Since March 2022, the Federal Reserve (Fed) has made 11 hikes, taking rates from 0.5% to 5.5%.

While holding rates, and turning the focus to economic data, all key decision makers have reiterated a desire to return inflation to the de facto (and frankly, arbitrary) 2% target level. Andrew Bailey, BOE Governor, commented “We will keep interest rates high enough for long enough to make sure we get inflation all the way back to the 2% target”, while Jerome Powell (Fed Chair) said, “…my colleagues and I are united in our commitment to bringing inflation down sustainably to two percent”. Any possibility inflation targets may be raised to mitigate the impact of higher-rate policy, or to reflect a changed employment market, clearly not being entertained.

Central bankers are in no mood to call time yet and recognise that, while inflation is clearly falling from recent highs, the job is not yet done. Market expectations for UK rates appear to be for some form of ‘plateauʼ, suggesting current levels will be held, as necessary to combat inflation, until the middle of 2024. The lagged effect, typically understood to be 18 months of interest rate rises to date is still to be fully seen. The BOE recognised this drag on UK growth, anticipating Q4 will see a continuation of the zero economic growth registered in the third quarter. The Fed has a larger economic problem to contend with – a buoyant US consumer resulted in the US economy notching up an impressive 4.9% annual growth rate in Q3.

It is likely even with peak rates we will continue to see gyration in bond yields as markets react to fresh data releases, particularly US job and gross domestic product (GDP) numbers. The plateau for rates may well become extended, and when considered alongside heavy issuance and a central bank, namely the BOE, which is actively selling bonds back into the market, we could yet see upward pressure on bond yields. However, this remains speculation and the rate-cycle ending is clearly a positive for bonds.

As such, bond yields have eased lower over the past month, correspondingly sending bond prices higher. This has been particularly apparent in the shorter maturity, circa six months, point of the UK sovereign yield curve, where yields have moved significantly lower, from 5.75% to 5.4% (at the time of writing), pricing out further rate rises. This is a dynamic we will likely continue to see, shorter maturity bonds falling as market pricing of future rate policy becomes more certain while longer maturity bonds remain volatile, and possibly static, reflecting economic conditions, other factors such as deglobalisation, and the need for governments to continue tapping investors.

For investors, it implies a need to continue actively monitoring the duration, or interest rate sensitivity (even if rates are not rising, yield moves will impact pricing) of your bond positions. Quantitative easing effectively removed any need for term premium when holding longer maturity bonds, now that has returned, so you need to be certain you are being compensated adequately for taking term risk.

Yale University hold the worldʼs oldest and still interest bearing, perpetual bond, issued in 1624 by the Hoogheemraadschap Lekdijk Bovendams to pay for flood defence repairs in the lower Rhine area of the Netherlands. Though the issuer no longer exists, the bondʼs liability, a princely sum of around £13 per annum, is paid by its successor Stichste Rijnlanden.

Our fixed income allocations comprise healthy exposures to a mix of high- quality US Treasury bonds, where we are actively managing interesting rate sensitivity, investment grade (the strongest) corporate bond issuers and to take advantage of attractive real yields, exposure to emerging market debt. Even as rates peak, the commitment of central banks to traditional inflation targets will likely see short-term fluctuations in bond yields. However, with yields in many cases above cash rates, with the additional benefit of a potential capital return, the opportunity in bonds is undeniably attractive.

Healthcare - November 2023

We have often written about healthcare equities and how they are set to benefit from long-term drivers of demand growth. We continue to believe this is the case but we must confront the fact that over this year, the sector has underperformed other areas.

Although healthcare encompasses a broad range of subsectors (with disparate drivers of returns), in the main, healthcare companies have been squeezed by cost pressures. Earnings for companies in the healthcare industry have declined 5% per year over the last three years, while the revenues for these companies have grown 7.7% per year. This means that although more sales are being generated, either the cost of doing business or the level of investment back into businesses has increased, leading to decreased profits.

There is still a tremendous amount of innovation within the sector evidenced by continued developments in the space. Obesity drugs are currently an area of excitement for the industry, with some forecasts estimating the total addressable market as well north of £100 billion. Analysts are also optimistic on the health-tech industry (technology specifically developed for the purpose of improving any aspect of the healthcare system) expecting annual earnings growth of 31% over the next five years.

While it is true that fledgling healthcare companies have been challenged by the higher interest rate environment, we expect to see an uptick in M&A, driven by the fact that pharmaceutical companies are facing big cliffs toward the end of the decade, with roughly £200 billion in revenue that will erode as a result of patent expirations that will allow for competition from generic drugs.

This year, Dr Howard Tucker, a neurologist from Cleveland, Ohio was named the ‘Oldest Practicing Doctorʼ at the age of 101, by Guinness World Records. Dr Tucker has an impressive track record and served as chief of neurology of the Atlantic fleet during the Korean War. In addition to these impressive accolades, he undertook his law degree and passed the Ohio Bar exam in his late 60s. Itʼs never too late!

We continue to hold a measured position in healthcare equities across portfolios, using a blend of an actively managed fund with a highly flexible mandate and a passive index tracker, in order to manage costs and provide a broad exposure to the space.

Commodities - November 2023

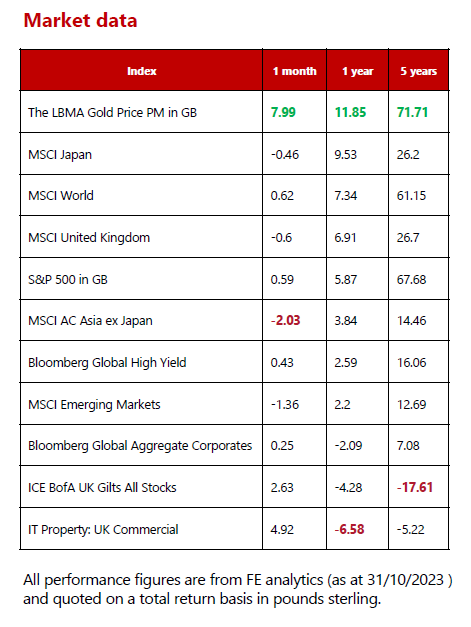

The eagle-eyed among you will have noted that the LBMA Gold Price (used as a global benchmark for gold and gold derivative assets) has been one of the best performing assets over a one-month, one-year and five- year period. This may be surprising because over nearly two decades, gold prices have been heavily influenced by 10-year US government bond yields, as the precious metal tends to be viewed as a proxy for very low-risk bonds. Higher real yields generally mean a fall in the gold price … but not this year. As you can see from the chart on the final page, gold returned more than 7% over October, despite the yield on the US 10-year treasury breaking above 5% – so, what is going on?!

Gold has certain unique supply and demand drivers affecting its price. During periods of increasing uncertainty and stress within financial markets worldwide, investors tend to flock to gold as a ‘safe havenʼ asset. This is particularly evident during periods where market participants are nervous about geopolitical conditions. Over October, the Hamas attack on Israel and subsequent escalation of conflict prompted a move away from risk assets (such as equities) and towards gold as a store of value.

Over the past five years, we have lived through some extraordinary events that have driven investors to seek shelter in assets that are perceived as defensive or safe. Indeed, the gold price tracker we use within portfolios was one of the few to deliver a positive return over March 2020 (2.94% versus -10.62% from the MSCI All Companies World Index, which captures a range of large and mid-capitalisation global equities), a period you may remember well as the onset of the Covid-19 pandemic and beginning of UK and US lockdowns.

When thinking about later life, it is important to have hope and few things encapsulate that powerful feeling as much as the celebration of Diwali; a festival celebrated by Hindus, Jains, Sikhs, and some Buddhists. The common thread is that it symbolises the victory of light over darkness. Hindus celebrate the return of Lord Ram, with his wife Sita and brother Lakshmana, after defeating demon Ravana and serving 14 years in exile. Divas (oil lamps) were put in windows to show the way home.

Although gold will generally underperform in a rising equity market, we continue to believe that exposure to the asset can provide useful diversification benefits. We see enduring tailwinds for the precious metal over the short term, as Poland has recently announced its intention to add to its gold reserves again over the coming months as well as the upcoming Diwali celebrations during which gifts of gold are considered auspicious.

Within portfolios we continue to have a meaningful exposure to an exchange-traded commodity that tracks the spot price of gold, which has delivered over 9% year to date (to 31 October).

The Monthly Market Commentary (MMC) is written and researched by Simon Gibson, Richard Smith, Scott Bradshaw, Mark Moore and Lauren Wilson for clients and professional connections of Mattioli Woods and is for information purposes only. It is not intended to be an invitation to buy, or to act upon the comments made, and all investment decisions should be taken with advice, given appropriate knowledge of the investorʼs circumstances. All content correct at time of writing. The value of investments and the income from them can fall as well as rise and investors may not get back the full amount invested. Past performance is not a guide to the future. Mattioli Woods is authorised and regulated by the Financial Conduct Authority.

The MMC will always be sent to you by the seventh working day of each month, usually sooner, is normally delivered via email, and is free of charge as the MMC is generally made available to clients who have assets under our management in excess of £200,000, and to all clients under our Discretionary Portfolio Management Service (DPM). Normally, the MMC costs £397 + VAT per annum. Professional advisers and their clients should contact us if they are interested in receiving a monthly copy.

Sources: All other sources quoted if used directly; except fund managers who will be left anonymous; otherwise, this is the work of Mattioli Woods.