Global markets summary

Following a lacklustre December, global equity markets started 2025 on solid footing, with most major indices ending the month in positive territory. The month-end figures do, however, mask the significant volatility we saw in certain market sectors, with a dramatic sell-off in tech and some energy stocks in the final week. European equities outperformed over the month, supported by low valuations, earnings recovery and improved inflation dynamics. Bond yields remained relatively stable over the month, allowing Government debt to eke out some modest gains. The credit market continued to outperform, benefiting from promising earnings estimates and lower default risks.

Writing this on just the fourth (and second working) day of February, we can say already that it has been an eventful period. Global equity markets were rocked on Monday 3 February after US President Trump announced sweeping tariffs on some of the US’ key trading partners. The very next day, markets staged a sharp rebound after the US President agreed to delay tariffs on Mexico and Canada following negotiations with each country’s leader. We view this as indicative of the increased levels of volatility we expect to navigate over the year as trade tensions and geopolitical uncertainties undermine market stability.

Rather than scrambling to react to erratic markets, we have remained resolute in our positioning within our core multi-asset solution, having tactically derisked the portfolios in December by increasing cash from 3% to 6%. Despite this caution, we retain a modest risk-on stance towards markets, based on an outlook of moderate growth and robust corporate earnings (particularly in the US). We maintain a neutral stance to most equity markets, moderately negative on fixed income and have added an element of ballast to portfolios (where appropriate) via physical gold.

United Kingdom

On the face of it, UK equities delivered strong returns over January, with the MSCI UK All Cap +5.54%. However, the headline index return masks a high degree of dispersion, with large-cap stocks outperforming their mid- and small-cap peers by 4.51% and 5.82% respectively.

The underperformance of mid- and small-cap stocks was largely attributable to the spike in UK Government bond yields during the month. Higher Government bond yields means higher borrowing costs and creates a drag on the economy. This is particularly unhelpful when growth seems to be elusive in the first place. The poor sentiment towards the economic health of the UK was reflected in sterling, which fell dramatically against the dollar.

In truth, higher yields were something that most economies experienced in January, as financial markets became increasingly concerned by the implications of a Trump presidency. However, the issue was exacerbated in the UK by poor economic data and concerns that Rachel Reeves may need to take more action to avoid a breach of her fiscal rules.

The combination of concerns around the domestic economy and a stronger dollar caused investors to seek safety in large-cap names, which also derive proportionally higher levels of revenue from overseas, relative to mid-cap peers.

January marked another difficult month in what has been a tough few years for UK mid-cap stocks, having underperformed their large-cap peers by almost 35% since the start of 2022. Despite this, we see reasons to be positive on their prospects moving forward. January marked a clear turning point in the narrative from the Labour Government, which has turned decidedly positive. Recently announced growth initiatives are being combined with a focus on deregulation, which should help at the margin. However, we also see the potential for more dramatic demand-side stimulus in coming months.

Higher interest rates have been a notable headwind for mid- and small-cap stocks. Weak economic data means the Bank of England is likely to cut interest rates in February, despite inflation remaining above 2%.

The past six months have been difficult for UK equity investors, largely due to the Budget. The overweight to mid-cap stocks within the UK Dynamic Fund has proved a headwind in recent months. However, the shift to more growth-orientated policies and the potential for interest rates to fall over the course of 2025 mean we remain positive for the year ahead.

North America

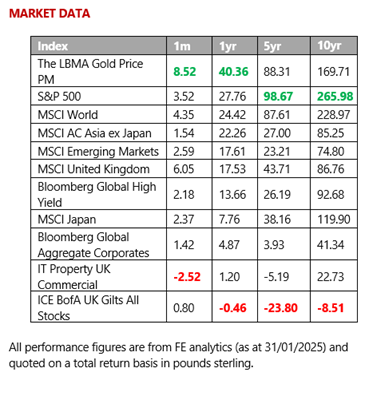

In the US, the S&P 500 delivered 2.76% in local currency over the month; however, the market’s heavy tech concentration weighed on performance towards the end of the month. The emergence of DeepSeek, a Chinese AI ‘challenger’ and its ability to produce efficient low-cost AI models hurt NVIDIA, which was the largest constituent of the S&P 500 index. We cover this in greater detail in the “Ask us anything” section below. US smaller companies enjoyed improved performance, with the Russell 2000 Index showing a recovery. Expectations of lesser regulatory burdens and favourable domestic policies under the new administration, as well as more attractive valuations, drove greater investor interest in the area.

The US economy continues to show signs of resilience, with strong job growth and a slight decrease in the core consumer price index boosting investor confidence. While President Trump’s ‘America First’ policy agenda initially proved supportive for US equities, threats of a 25% tariff on goods from Mexico and Canada (alongside a 10% additional tariff on Chinese goods) have significantly raised the probability of a more economically damaging trade war between the US and its main trade partners. As at time of writing, Canada and Mexico have negotiated a 30-day reprieve but the situation remains fluid and is likely to be a driver of short-term market volatility.

We maintain a neutral stance to US equities, believing that this period has underscored the potential risk of high US stock market concentration and high earnings expectations, highlighting the importance of regional, style and sector diversification.

Europe

European equities have started the year strongly, outperforming US equities by a significant margin, and delivering their best monthly performance in over two years. Over the month, major companies like SAP SE and Deutsche Telekom in Germany reported strong earnings, boosting overall market sentiment, while certain sectors, such as pharmaceuticals in Denmark and natural gas extraction in Norway, experienced significant growth. Overall, the energy and utilities sectors performed well, the former buoyed by rising crude oil prices and the latter benefiting from defensive characteristics.

Despite some underlying vulnerabilities, the European economy is showing signs of stability and modest growth, which has piqued investor interest, with inflows to European equities recording their strongest monthly pace in over a year. It looks like spring may have come early for the region, with green shoots of growth emerging, supported by lower policy rates and easing inflation. The European Central Bank is expected to lower interest rates to 1.75% by mid-2025, which could benefit sectors like telecoms and real estate that are sensitive to interest rates, while strong earnings reports from major companies, especially in the tech and energy sectors, are likely to support market performance.

We also saw another tailwind for consumers across the region emerge over the month as European gas prices fell from their 15-month highs on the back of China’s tariffs on US liquefied natural gas imports. Traders are anticipating China will resell further cargoes it takes from the US into Europe, a step the country has already taken due to waning domestic demand and high prices in Europe.

We have a balanced exposure to European equities across our multi-asset funds retaining a neutral stance to the region. While we see some relative value in European stocks, we believe that the recent investor enthusiasm underestimates the potential risks, including geopolitical uncertainties and economic slowdowns.

Rest of the world

In terms of developed markets, Japanese equities were the laggard over the month, with the upward pressure on the yen acting as a headwind for the export-oriented equity market. However, the outlook for the region remains relatively stable as the Bank of Japan (BoJ) delivered a 0.25% interest rate hike as its confidence in the sustainability of domestic wage growth increased.

Overall, emerging markets underperformed the majority of their developed peers, as a strengthening dollar acted as a headwind while uncertainty over US trade policies, particularly potential tariff implementations, led to cautious investor sentiment. Chinese equities eked out marginal gains over the month thanks to more optimistic domestic economic data and less aggressive tariff threats from President Trump than the 60% he floated on the campaign trail.

However, the Asia Pacific market was weighed down by Indian equities, driven by challenges in the banking sector as well as a combination of multiple compression and reduced earnings. In contrast, South Korea’s KOSPI index rose by 2.3%, driven by gains in the semiconductor and automotive sectors.

There is a small exposure to Asia Pacific and emerging markets across our multi-asset funds. Our stance on the area is neutral as we recognise market headwinds such as US dollar strength and the impact of trade tariffs.

Fixed income

Corporate credit continued to outperform developed market government debt over January. In the UK, gilt yields moved higher, briefly touching the highest level since 2008, as concerns around the stagflationary domestic outlook grew. However, a weaker-than-expected UK December inflation print calmed the market and UK bonds eked out 0.8% over the month.

US Treasury yields were relatively stable over the month, supported by the Federal Reserve decision to maintain its interest rates at 4.25-4.50%, citing a stable labour market. While future rate cuts are anticipated, they are not expected before June 2025. In contrast, Europe’s Central Bank (ECB) cut rates to 2.75%, noting progress in disinflation, increasingly the likelihood of monetary policy diversion across developed markets.

In the credit space, high-yield bonds continued their rally with the Bloomberg High Yield Index posting a total return of 1.37%. This performance was influenced by a combination of stable economic conditions and investor confidence in the high-yield sector.

Overall, we maintain our preference for shorter-dated (less sensitive to interest rate changes) bonds, for now, given the lingering threat of inflationary pressures.

Ask us anything

Q: Why did NVIDIA’s share price fall so dramatically at the end of January and what does this mean for US tech?

A: At the end of January, a sell-off of global technology shares wiped up to $1 trillion off US stock markets, with the US chipmaker NVIDIA falling more than 13%, and losing $465 billion off its market value – the biggest such fall in US market history. Given that a group of mega-cap AI-related companies (i.e. ‘the Magnificent Seven’) has driven the US market over the past few years, the moves sparked investor consternation.

The popularity of a new Chinese AI app from the startup DeepSeek (DS) has emerged as a major challenger to the established AI names in the West. The DS app is essentially a version of OpenAI’s ChatGPT. Not only is it free to use – and DS has published a paper on how it developed it – it uses less data and runs off lower-level hardware. The US has banned exports of the highest-end chips to China, including those made by NVIDIA. The DS model uses 2,000 older chips and has been ‘trained’ for much lower costs than rival AIs. Investors are viewing this as a legitimate challenge to the perceived superiority of Silicone Valley’s AI and indispensability of its infrastructure.

While the recent sell off is likely overblown, AI is no longer an ‘easy’ trade. Increased competition means that investors will have to do a bit more research and companies must deliver on earnings.

The AI super-race is seeing new challengers emerge and not everyone is going to win. The companies that enjoyed first-mover advantage will now be under pressure to launch something even better or be left behind. DS’ success confirms that leading-edge model efficacy is being commoditised faster given the pace of innovation and competition. It’s natural evolution; when a company launches a product or service that sees strong demand, another will always try to undercut the market leaders with a cheaper version.

While the algorithmic progress made by DS is legitimate, the competitive moat for the model makers is weak, and algorithmic innovations are typically easy to replicate by competition. A lack of sustainability of competitive advantage also suggests temporary mind share may not result in a sustainable market share for DS. In addition, DS faces risk from further increases to US chip export restrictions that prevent access to the calibre of compute they will need in order to continue marching along the same trajectory as US peers.

There are also some features that will likely be seen as unpalatable to international audiences; the DS app appears to censor answers to sensitive questions about China and its government. Chinese generative AI must not contain content that violates the country’s “core socialist values”, according to a technical document published by the national cybersecurity standards committee. This includes content that “incites to subvert state power and overthrow the socialist system”, or “endangers national security and interests and damages the national image”. Down the line, DS could find itself embroiled in legal troubles like TikTok parent ByteDance.

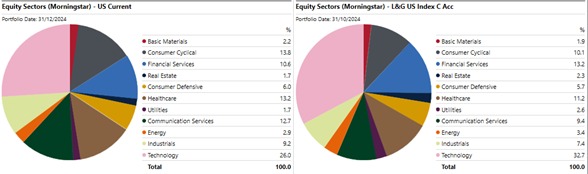

Our core multi-asset funds were well insulated from the sell-off. Our exposure to technology is slightly lower than the benchmark due to our blend of growth and value-style funds. The sector exposure of our current US sleeve is shown below against the benchmark (represented by an index tracking fund).

Our decision to move towards actively-managed US funds should also be helpful because, as we noted above, the AI landscape is maturing to a point where winners will be emerging, and fundamental stock analysis is key when identifying the victors.

Key points

- The emergence of a Chinese AI app has called the dominance of Silicone Valley tech companies into question, leading to a sell-off in US tech companies at the end of January.

- Increased competition is part of the evolution of a new technology.

- The AI trade is no longer ‘easy’ and will require in-depth fundamental stock analysis to identify winners.

- The MW Multi Asset Funds are well insulated given their balanced exposure to growth and value stocks and active management skew within US equities, where the ‘Magnificent Seven’ stocks dominate the index.

If there is a question you’d like to pose to our team, please reply to this email or write to [email protected].

The Monthly Market Commentary (MMC) is written and researched by Scott Bradshaw, Lauren Hyslop and Jonathon Marchant for clients and professional connections of Mattioli Woods and is for information purposes only. It is not intended to be an invitation to buy, or to act upon the comments made, and all investment decisions should be taken with advice, given appropriate knowledge of the investorʼs circumstances. The value of investments and the income from them can fall as well as rise and investors may not get back the full amount invested. Past performance is not a guide to the future.

Mattioli Woods is authorised and regulated by the Financial Conduct Authority.

Sources: All other sources quoted if used directly, except fund managers who will be left anonymous; otherwise, this is the work of Mattioli Woods.