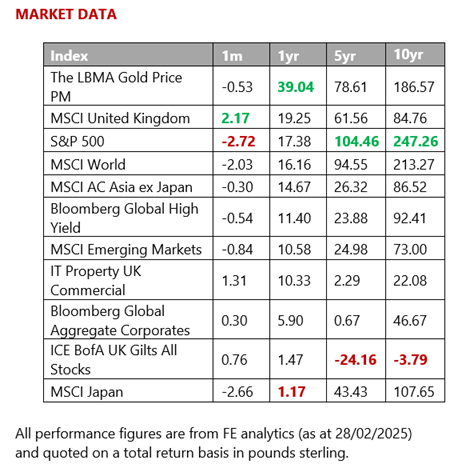

Global markets summary

February saw a continued departure from the status quo in the equity space, with US markets significantly lagging those of the United Kingdom, Europe, Asia Pacific and Japan. The allure of the ‘Trump trade’ following the Republicans’ decisive US election victory last year has waned in recent weeks, to be replaced by concerns over the US President’s tariff policies. Investors began to question the strength of the US economy following the release of softening economic data and a series of policy announcements. Meanwhile, emerging markets enjoyed several tailwinds over the month, namely continued positive momentum in Chinese technology stocks as well as the weakening US dollar.

Most bond markets ended the month in positive territory as investors sought a safe haven from the volatility in the US equity market, while corporate credit (particularly the high-yield market) remained relatively insulated from the uncertainties around inflation.

In the commodities space, cold weather combined with temporary supply shortages boosted US natural gas prices. Despite some mid-month dips in the gold price, the overall trend was positive, reflecting increased demand for gold as a hedge against market volatility.

While the past two years have clearly been dominated by monetary policy, 2025 has experienced factors from trade tariffs to fiscal policy that are likely to play a pivotal role in shaping a more complex macroeconomic landscape. While we expect uncertainty to be prolonged until we have more concrete data on the size and scope of US tariffs and the economic fallout as a result, we remain encouraged by solid earnings momentum and relatively resilient hard economic data. Over the next few months, we believe that strategic and dynamic management of risks and opportunities will be key.

United Kingdom

The UK continued its strong start to the year in February, with the MSCI United Kingdom All Cap delivering performance of +1.43%. The UK market is often criticised for containing ‘boring’ companies. However, during times of geopolitical uncertainty, they can provide a safe harbour for investors. February’s performance means that the UK market is now ahead of broader global equities by almost 5%, in what has been a tumultuous start to the year.

Last month, we commented on the dramatic outperformance of large-cap stocks, over small- and mid-cap during January. This also proved to be the case in February and domestic mid-cap stocks already find themselves c.9.5% behind their larger peers in 2025. As we have mentioned in the past, mid-cap stocks tend to be more exposed to the domestic economy and the data remains mixed.

On a positive note, the Bank of England cut interest rates by 0.25% during February, which helps to ease some of the pressure on consumers and businesses. The issue for central bankers is that inflation is forecast to rise to almost 4% later in the year, making it difficult to advocate for further cuts in the intervening period.

The willingness to cut rates further depends on quite how weak economic data will be over the coming months. While far from stellar in absolute terms, recent data has been better than expected in several cases. Specifically, GDP figures came in at +0.1% versus the -0.1% analysts had forecast, retail sales numbers were better than expected and so were consumer confidence numbers.

While it is too early to be certain about the UK’s trajectory, we believe that there is the potential that the gloom around the domestic economy is overdone. Interest rates should trend lower over time and economic growth should improve over the next year, as public spending plans start to filter through. The Chancellor’s Spring Statement, later this month, will be watched closely. The concern is that further tax rises and/or spending cuts are needed to balance the books. From a polling perspective, the Budget was a disaster for Labour and they will be looking to ensure that the public’s belief doesn’t sink further.

Of course, we invest in companies, not economies and the most attractive returns can often be found by going against the grain. Few would have predicted at the start of 2025 that UK and European stocks would be materially ahead of their US counterparts, given the fanfare that President Trump received. In a similar vein, we continue to believe that the market is being overly pessimistic on the prospects for the UK domestic economy and, though it has hurt so far this year, we retain an overweight to mid-cap stocks in our UK Dynamic Fund and continue to see significant value lower down the market cap spectrum.

North America

US equity markets have been weak year to date, hampered by inflation concerns, and global tariff policies, as well as a significant drop in consumer confidence to an eight-month low. The technology sector has felt the pain most acutely, with the tech-focused NASDAQ the clearest underperformer of the bigger indices with a 6% decline, leaving the 2025 total return in the red.

We have consistently noted that certain areas of the US equity markets were somewhat expensive and heavily reliant on blockbuster earning releases and guidance for future results to sustain momentum. As these have not come to pass, equities have responded accordingly. Notably, although NVIDIA’s earnings report exceeded forecasts, its release led to a decline in the stock price due to lower-than-expected gross margin guidance.

Alongside technology, communication services and consumer discretionary were the worst performing sectors over the month. However, we continued to see evidence of a rotation inside the index with more value-orientated sectors such as consumer staples, energy and real estate all delivering healthy positive returns over the month.

There seems to be growing evidence that the uncertainty created by tariffs is taking a toll on confidence. As a reminder, President Trump reinstated a 25% tariff on steel imports and increased the tariff on aluminium imports to 25% while imposing new tariffs of 25% on goods from Canada and Mexico and an additional 10% tariff on Chinese goods, bringing the total tariff on these imports to 20%. Over the past few weeks, US data has been weaker than expected; consumer confidence showed the largest month-on-month fall since the summer of 2021, when inflation and the Covid-19 delta variant were on the rise. Alongside this slump in overall sentiment, there was an increase in inflation expectations, while forecasts for the labour market weakened.

Within core portfolios, we retained a neutral allocation to US equities but amended the composition to further reflect our positivity on value over growth. This was a well-timed move given the falls in US large-cap growth stocks towards the end of the month. Similarly, we further diversified into specialist mid- and small-cap funds given ongoing concerns around large-cap valuations and index concentration.

Europe

So far this year, European indices have fared far better than their US counterparts, with the EURO STOXX 50 delivering 2.15% over the month. We saw strong performance from several sectors, including financials benefiting from improved bank profitability and favourable monetary policy while consumer discretionary and industrials stocks were supported by signs of a recovery in economy activity.

Political news has been dominated by the German elections and the theme of Europe stepping up defence spending given the collective view in Europe that continued US support under President Trump is far from guaranteed. There was also cautious optimism about a potential resolution to the conflict in Ukraine, which reduced geopolitical risks and encouraged investment.

Towards the end of the month, however, European indices pulled back from all-time highs as US President Trump proposed 25% tariffs against the European Union. The details of these tariffs remain limited, with the US President mentioning, “cars and all of the things”. We expect markets to be sensitive to news flow on this subject over the near term.

Despite the prevailing positive sentiment, our view on European equities remains neutral as we see a number of risks on the horizon. Although recent figures have been modestly optimistic, we remain concerned about the region’s growth outlook. For instance, the German economy is smaller now than it was before the Covid-19 pandemic, and it appears that without additional government spending, stronger economic growth will likely remain elusive.

Rest of the world

Asia Pacific markets enjoyed a strong February led by the Hang Seng Index, which was driven by strong gains in consumer and technology stocks. The announcement of a $HK1bn (Hong Kong dollar) investment in AI research and development boosted market sentiment too. China’s Shanghai Composite Index also ended the month in positive territory following the release of more upbeat economic data and further government stimulus measures. Over the month, investors were pleased to see the Chinese government show a more favourable attitude towards the private sector with promises to remove obstacles to fair market competition and make financing easier for private companies.

In contrast to US counterparts, the Asia Pacific technology sector saw substantial gains, driven by advancements in artificial intelligence and other high-tech industries. Excitement about the implications of DeepSeek, the advanced AI platform developed by a Hangzhou-based startup, continued to support the broader Chinese tech complex while high-profile meetings between Xi Jinping and senior business leaders alluded to an improved regulatory environment. However, these returns were concentrated in the export-focused offshore market as continued worries about the weak real estate market meant that GDP-sensitive domestic equities lagged.

Japanese markets were mixed, with strength in consumer discretionary and industrials offset by weakness in financials and utilities. The TOPIX delivered negative returns over the month with the yen-sensitive market suffering as the currency appreciated by 2.8% against the dollar.

We retain a small broad exposure to Japanese, Asia Pacific and emerging market equities across portfolios, acknowledging the upside potential of the region but also mindful of persistent headwinds to performance, such as the ongoing tension between the US and China.

Fixed income

Overall, bond markets have had a relatively strong start to the year. We have seen fluctuations in US Treasury yields as the benchmark 10-year yield rose following the advancement of President Trump’s tax cutting plan, but later experienced movements influenced by concerns around economic growth and consumer confidence following the release of generally disappointing economic data from the region.

UK gilt yields also experienced some turbulence influenced by various factors, including economic data releases and market sentiment. While the Bank of England cut interest rates by 0.25% to 4.50% at its February meeting, the chances of further rate cuts reduced after higher-than-expected inflation figures have been released in the weeks since.

Corporate credit has continued to benefit from solid corporate fundamentals and favourable technical tailwinds. In the high-yield space, default rates have increased marginally but remain below their historic average.

Overall, we maintain our preference for shorter-dated (less sensitive to interest rate changes) bonds, for now, given the lingering threat of inflationary pressures.

Ask us anything

Q: Are sustainable/responsible strategies still worth investing in?

A: The decision to invest with a sustainable or responsible focus is very much a personal choice. While there has been a lot of noise around the space lately, we can look at some of the factors influencing the investment thesis.

It is clear that the latter half of 2024 brought about some sustainability-related headwinds. Responsible investment strategies often have a significant allocation to companies related to decarbonisation. Over the period, companies involved in the energy transition, such as renewable energy firms, faced operational and financial challenges (including supply chain disruptions and increased costs) that negatively impacted their stock prices. Furthermore, shares in clean energy groups fell immediately after Donald Trump was elected president of the United States, as investors fretted over a potential dismantling of US support for renewables and climate policy. We have not yet seen prices recover as the President’s plans on climate policy remain unclear.

There are, however, a number of reasons to be positive on this sector, as while growth in renewable investment will likely slow in the US under Trump’s presidency, we do not expect it to decline. Many Republican states benefit from renewable investment, and utility-scale wind and solar continue to represent the lowest-cost forms of electricity even without tax credits/subsidies. It is also key to note that during President Trump’s first term, solar and wind investment grew.

Over the past few years, equity market returns have been very concentrated and driven by a handful of large-cap US stocks. Broadly, sustainable strategies have greater exposure to mid/small-cap companies than peers. In 2025, we have seen a rotation away from the large cap ‘Mag 7’ stocks and stronger performance from other areas of the market. We have discussed elsewhere that there are a number of drivers of the broadening of stock market performance and tailwinds for US mid/small-cap stocks as well as non-US-developed market stocks. As such, sustainability-led funds can often be a good diversifier within a portfolio as (generally) they outperform during periods where small/mid-cap companies rally and can be less reliant on the continuation of US exceptionalism than the majority of peers.

That said, it is worth noting that sustainable strategies tend to be slightly more expensive than those without such a mandate given that they tend to require greater levels of scrutiny and analysis, with investment managers committed to review the financial and sustainability thesis of each holding. For the more cost-sensitive investor with less conviction around the efficacy of sustainable investing, this is unlikely to be the right strategy.

Over the short term, it’s unlikely to be plain sailing for these strategies but there are still some compelling reasons to invest, particularly if you have a long-term time horizon and an interest in the area.

Key points

- President Trump’s decisive victory sparked a sentiment-led sell-off in stocks related to sustainability; however, there are reasons to be positive and await a recovery in these names.

- Sustainability-driven funds tend to have a greater allocation to small/mid-cap companies and, as such, can be a good diversifier within a portfolio.

- These funds are generally a little pricier.

If there is a question you’d like to pose to our team, please reply to this email or write to [email protected].

The Monthly Market Commentary (MMC) is written and researched by Scott Bradshaw, Lauren Hyslop and Jonathon Marchant for clients and professional connections of Mattioli Woods and is for information purposes only. It is not intended to be an invitation to buy, or to act upon the comments made, and all investment decisions should be taken with advice, given appropriate knowledge of the investorʼs circumstances. The value of investments and the income from them can fall as well as rise and investors may not get back the full amount invested. Past performance is not a guide to the future.

Mattioli Woods Limited is authorised and regulated by the Financial Conduct Authority.

Sources: All other sources quoted if used directly, except fund managers who will be left anonymous; otherwise, this is the work of Mattioli Woods.