Global markets summary

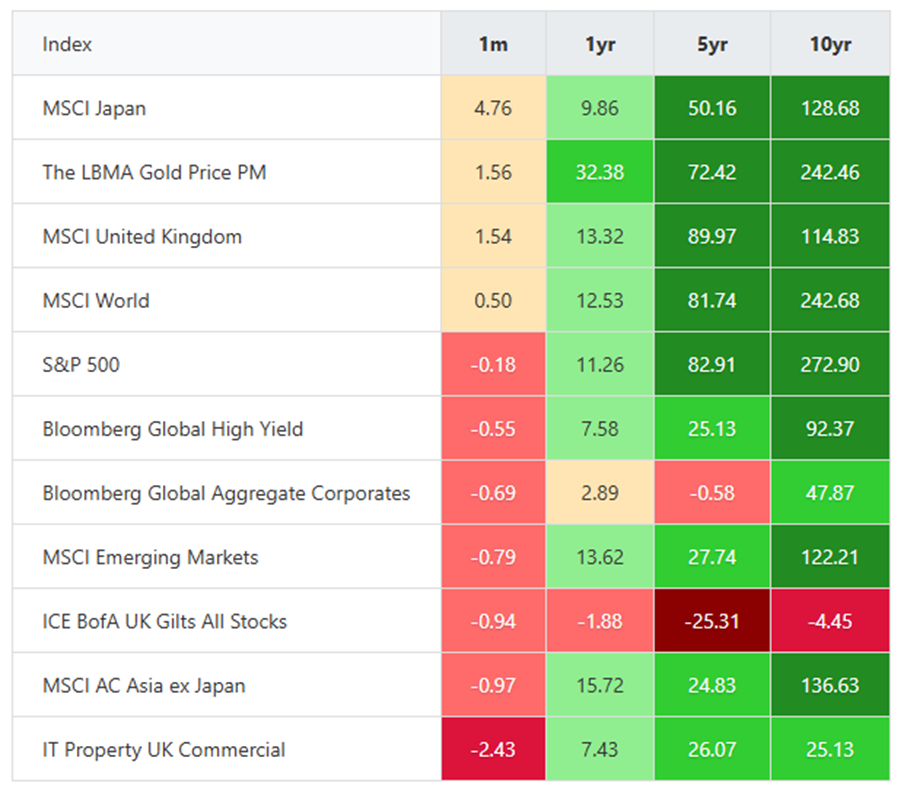

Over the month of August, global equities displayed mixed performance. Japanese equities led the way, with the TOPIX and Nikkei hitting records amid favourable US trade terms and steady monetary normalisation. In the US, the S&P 500 climbed by 1.99% in local currency terms, but sterling’s 2.07% surge against the dollar meant UK investors saw that translated into -0.10% returns – a sobering currency lesson.

At home, UK large caps continued their defensive tilt. Energy giants, utilities and consumer staples found favour as fund managers sought shelter from global headwinds, while smaller companies struggled to keep pace. European markets delivered positive returns but could not match their global peers. France proved the drag, with the CAC 40 slipping 0.9% as political uncertainty flared following a no-confidence vote. Given French firms constitute roughly a fifth of the MSCI Europe ex-UK index, this weighed heavily on regional performance.

The emerging market landscape painted a varied picture. China and the US extended their trade truce to November, offering relief to export-focused businesses. Beijing’s ambitious plan to triple domestic chip production by 2026 gave Chinese tech stocks a boost. However, not all was rosy; South Korean shares stumbled on tax reform concerns and Indian equities felt the sting of a 50% US tariff.

Fixed income delivered muted performance relative to equities, though corporate bonds outpaced their government counterparts. Strong second-quarter earnings provided the primary catalyst, while expectations of deeper Federal Reserve (Fed) easing offered additional support, particularly for longer-duration assets. Emerging market debt found favour, benefiting from both anticipated US rate cuts and modest dollar weakness. In the UK, gilt markets faced headwinds, with 10-year yields climbing 12 basis points to 4.72% as Budget concerns mounted. US Treasuries, by contrast, rallied strongly – yields compressed to 4.23% ahead of the Fed’s anticipated September interest rate cut.

Overall, August was a broadly positive month for markets. Investor sentiment held up as data releases suggested global activity remains resilient and inflation remains under control, despite less positive US labour market news and a sobering report highlighting the lack of profitability among most AI companies. However, a supportive outlook is already reflected in equity valuations, which broadly sit above their long-run averages, especially in the US. Thus, investors should ensure their portfolios are well-diversified across both regions and assets, to protect against the chance of a delayed, trade-related slowdown, as well as against any re-emergence of inflationary pressures as tariff rises continue to feed through to consumer prices.

United Kingdom

UK equities delivered strong performance in August, outpacing global markets despite challenging headlines. Much attention focused on rising borrowing costs, with 30-year gilt yields reaching levels not seen since 1998. The primary market concern remains stagflation – stagnant growth combined with persistent inflation.

August CPI data reinforced these concerns, showing inflation at 3.8% year on year, above the 3.7% consensus and moving further from the Bank of England’s 2% target. Services inflation accelerated from 4.7% to 5.0%, also exceeding expectations at 4.8%. This trajectory suggests policymakers may need to maintain higher rates for longer, making the recent narrow interest rate vote appear prescient.

Political uncertainty continues to weigh on sentiment. While Labour campaigned on “growth”, delivery has been limited, with the previous Autumn Budget’s implications persisting through higher employment costs, adding to inflationary pressures while reducing business confidence. Last year’s Budget saw a prolonged period of speculation around tax rises, which stalled decision making. It seems that this year we are facing a similarly rampant rumour mill, with ideas from windfall taxes on banks to additional property taxes being floated in the media.

However, several factors provide grounds for measured optimism. Rising borrowing costs are a global phenomenon, not unique to the UK, while higher inflation and yields partly reflect underlying economic resilience. Consumer confidence recently reached its highest level since December 2024 and several key business confidence indicators are delivering positive readings. Though the latest GDP figures showed a slowdown to +0.3% in July, the number exceeded analyst expectations.

UK equities have delivered strong returns this year, though with significant dispersion between market segments. Large-cap stocks have delivered double the performance of mid-caps year to date. While negative domestic headlines persist, they contrast with decent fundamental economic data and solid corporate earnings. The large-cap outperformance has impacted our UK Dynamic Fund’s relative performance but, after a strong run, we believe numerous large-cap stocks now trade on increasingly unattractive valuations. More compelling long-term opportunities reside in the mid- and small-cap segments, where we maintain our focus.

North America

Sterling investors experienced a rather different August than their American counterparts. While the S&P 500 posted a respectable 1.99% gain in dollar terms, currency headwinds told another story entirely. The greenback’s 2.07% retreat against sterling effectively erased these gains, leaving UK investors marginally in the red at -0.10%.

Behind the headline figures lay a month of notable turbulence. Historic downward revisions to US employment data (among the largest outside the pandemic era) rattled investor confidence and raised questions about economic visibility. Meanwhile, technology shares faced headwinds following an MIT study suggesting AI pilot programmes have yet to meaningfully boost corporate revenues.

Yet it wasn’t all doom and gloom. Corporate America delivered where it mattered: three-quarters of S&P 500 companies exceeded (admittedly modest) earnings expectations, marking the strongest beat rate since 2021. Manufacturing sentiment also brightened, with August’s PMI survey painting an encouraging picture. In a strategic move, Washington unveiled plans to acquire a 10% stake in Intel, signalling commitment to domestic chip production. Smaller companies emerged as August’s winners, outpacing their larger peers as investors positioned for anticipated rate cuts while taking comfort from resilient economic data.

Our view

We maintain a measured stance on US equities. While earnings have stabilised, limited forward guidance and elevated valuations suggest vulnerability to disappointment. We continue to favour geographic diversification, with better value opportunities evident elsewhere. Our US allocation remains deliberately balanced across market capitalisations and investment styles – from small cap to large cap, value to growth – ensuring we’re not overly concentrated in any single segment.

Europe

European equities (EURO STOXX) delivered a modest 0.49% return in sterling terms for August, lagging their global counterparts despite pockets of encouraging data. Manufacturing strength pushed the eurozone’s composite PMI to 51.1, while credit growth remained robust through July.

Yet France cast a long shadow over regional performance. With French companies comprising roughly a fifth of the MSCI Europe ex-UK index, the CAC 40’s 0.9% decline weighed heavily on broader returns. Political turbulence took centre stage as confidence votes on deficit-cutting measures stoked fears of governmental gridlock, potentially derailing efforts to address fiscal challenges.

Markets responded predictably. French borrowing costs climbed to their highest levels since March, with 10-year yields touching 3.53%. Domestic-facing sectors bore the brunt, with the nation’s banking giants – BNP Paribas, Société Générale, and Crédit Agricole – each sliding more than 4% as investors treated them as proxies for economic health. While France dominated headlines, malaise extended beyond its borders. The STOXX Europe 600 remained stubbornly below its early March peak, suggesting continental challenges run deeper than any single nation’s political drama.

Our view

We maintain a neutral stance on European equities. Attractive valuations and cyclical exposure position the region to benefit should market leadership broaden, while German fiscal commitments offer long-term support. However, trade policy uncertainties and political instability continue to temper our enthusiasm. We’re watching for clearer signals before adjusting our positioning.

Rest of the world

August belonged to Japan. In a remarkable display of strength, the TOPIX shattered the psychologically important 3,000-point barrier for the first time in its history, crowning what has been an extraordinary year for Japanese equities. The catalyst? A veritable tsunami of foreign capital. International investors have poured $35.7 billion into Japanese stocks this year, with the bulk arriving after “liberation day” when investors began to look beyond US equities. This flood of overseas money reflects growing confidence that Japan Inc. has genuinely turned a corner.

Geopolitics provided additional tailwind. A timely trade agreement with Washington quelled fears of potential tariffs on Japanese exports, while Tokyo’s status as America’s key regional ally offered investors a haven from broader Asian uncertainties. The timing couldn’t have been better, as US-China trade tensions showed signs of thawing, lifting sentiment across the region.

Yet as August progressed, cracks began to appear in the broader Asian equity story. South Korean shares stumbled on domestic tax reform concerns, while Indian markets reeled from the imposition of punitive 50% US tariffs. These headwinds transformed what began as a pan-Asian celebration into a more nuanced picture of winners and losers.

Sterling’s summer strength added another layer of complexity for UK investors. While the TOPIX still delivered an impressive 4.80% return in pound terms, currency headwinds turned positive local returns negative elsewhere: MSCI Emerging Markets fell 0.79% and Asia ex-Japan dropped 0.97% for sterling-based portfolios.

Our view

We maintain a neutral stance on the region. Valuations remain compelling, particularly in Japan, and emerging markets appear under-owned, potentially offering opportunity should the dollar weaken. However, geopolitical wildcards and the spectre of escalating trade disputes keep us cautious. We are positioned to participate in further gains while remaining mindful of the risks that could quickly shift sentiment in these dynamic markets.

Fixed income

Credit markets painted a broadly constructive picture in August, with investment grade spreads tightening on both sides of the Atlantic. Strong second-quarter earnings provided the foundation, while growing conviction around Federal Reserve rate cuts offered additional support to these duration-sensitive securities. The high-yield space told a tale of two continents. American issuers outpaced their European peers, buoyed by robust PMI data and superior earnings delivery that kept risk appetite intact despite softening employment figures. Meanwhile, emerging market debt found favour as dollar weakness and rate cut expectations created a supportive backdrop for the asset class.

In government bond markets, US Treasuries rallied following Federal Reserve (Fed) Chair, Jay Powell’s, pivotal Jackson Hole address. The Fed Chair’s acknowledgement that economic risks had shifted – citing subdued inflation and concerning employment revisions – sparked a repricing of rate expectations. Markets swiftly moved to price a September cut as near-certainty, while also lowering terminal rate expectations. Notably, the yield curve steepened as investors demanded greater compensation for longer-dated bonds, perhaps reflecting growing unease about institutional independence.

UK gilts, by contrast, endured a torrid month. July’s upside inflation surprise forced investors to recalibrate Bank of England expectations, pushing short-end yields higher. The long end fared even worse, with 30-year gilt yields touching 5.6% – levels not seen since 1998. Thin summer liquidity amplified moves, but persistent concerns about Britain’s fiscal trajectory provided the underlying narrative.

Our view

We are maintaining short duration positioning, particularly in government bonds where valuations offer little cushion against disappointment. Despite recent gilt weakness, we are neutral on UK government debt – the Bank of England appears better positioned than the Fed to navigate the current environment. Investment grade credit remains unappealing at historically tight spreads; we see superior risk-reward elsewhere. Emerging market debt, however, continues to attract us. Dollar weakness provides a helpful tailwind, while improving fundamentals (evidenced by upgrades consistently outpacing downgrades) suggest the asset class remains on solid footing.

Ask us anything

Q: Why did tech stocks, especially AI, pull back this month when earnings results were so strong?

A: An excellent question that gets to the heart of August’s market paradox. The culprit? A sobering reality check from the Massachusetts Institute of Technology (MIT) that sent shivers through Silicon Valley. MIT’s latest report, The GenAI Divide: State of AI in Business 2025, landed like a bucket of cold water on AI enthusiasm. Its headline finding, that 95% of enterprise AI implementations have failed to deliver measurable profit increases, triggered immediate selling across the tech sector. NVIDIA, Palantir, Oracle, AMD, and AppLovin all suffered single-digit declines as investors suddenly questioned whether we’re witnessing innovation or simply inflating another bubble.

The research credentials were impeccable: 150 leadership interviews, 350 employee surveys, and 300 deployment analyses. Yet rather than spelling doom for AI, we believe the findings offer a roadmap for success.

MIT’s data reveals fascinating patterns. Companies that partner with specialised AI vendors succeed roughly 67% of the time, while those attempting to build internally succeed only a third as often. The message? Collaboration trumps isolation in the AI revolution. Perhaps more intriguingly, the report exposes a glaring misallocation of resources. While over half of AI budgets flow into sales and marketing tools, the real returns lie elsewhere – in unglamorous back-office automation that slashes outsourcing costs and streamlines operations. It’s the corporate equivalent of looking for your keys under the streetlight rather than where you dropped them.

Here’s what MIT’s metrics missed: the rise of ‘shadow AI’ – employees quietly wielding ChatGPT and Copilot to transform their daily workflows. These informal productivity gains don’t appear on corporate dashboards, yet they may represent AI’s true transformative power. The revolution isn’t always televised; sometimes it’s happening in countless small improvements across millions of desktops.

We are witnessing AI’s awkward adolescence, not its demise. Volatility will remain a feature, not a bug, as markets grapple with separating substance from hype. We maintain exposure to companies leading this technological shift while balancing our portfolios with US mid- and large-cap value positions. This ensures we capture AI’s upside without being hostage to sentiment-driven selloffs that periodically grip the sector. The August pullback reminds us that even revolutionary technologies follow messy, non-linear paths to adoption. We’re staying the course but with eyes wide open.

If there is a question you’d like to pose to our team, please reply to this email or write to [email protected].

Four key takeaways from August:

• Sterling’s strength erased gains for UK investors, with the S&P 500’s 1.99% dollar return becoming -0.10% in pound terms.

• An MIT report revealing 95% of enterprise AI implementations fail to deliver profit increases triggered a tech stock selloff, despite strong earnings across the sector.

• Japanese equities hit record highs as foreign investors poured $35.7 billion into the market this year, while European stocks languished under French political uncertainty.

• UK gilts suffered their worst month, with 30-year yields hitting 5.6% (highest since 1998) on inflation surprises, while US Treasuries rallied on Fed rate cut expectations.

MARKET DATA

All performance figures are from FE analytics (as at 31/08/2025) and quoted on a total return basis in pounds sterling.

The Monthly Market Commentary (MMC) is written and researched by Scott Bradshaw, Lauren Hyslop and Jonathon Marchant for clients and professional connections of Mattioli Woods and is for information purposes only. It is not intended to be an invitation to buy, or to act upon the comments made, and all investment decisions should be taken with advice, given appropriate knowledge of the investorʼs circumstances. The value of investments and the income from them can fall as well as rise and investors may not get back the full amount invested. Past performance is not a guide to the future.

Mattioli Woods Limited is authorised and regulated by the Financial Conduct Authority.

Sources: All other sources quoted if used directly, except fund managers who will be left anonymous; otherwise, this is the work of Mattioli Woods.