The facts:

- The Maternity and Parental Leave etc. Regulations 1999 and the Paternity and Adoption Leave (Amendment) Regulations 2014 confirm that employers must provide pension contributions during any period of paid maternity leave (statutory or contractual). However, it makes it lawful for an employer not to maintain an employee’s pension contributions in respect of periods of unpaid maternity leave.

- Currently, maternity leave is for 52 weeks, 39 weeks of which is paid. Employers are therefore not obliged to continue making pension contributions during unpaid maternity leave (i.e. the last 13 weeks of the maternity leave period).

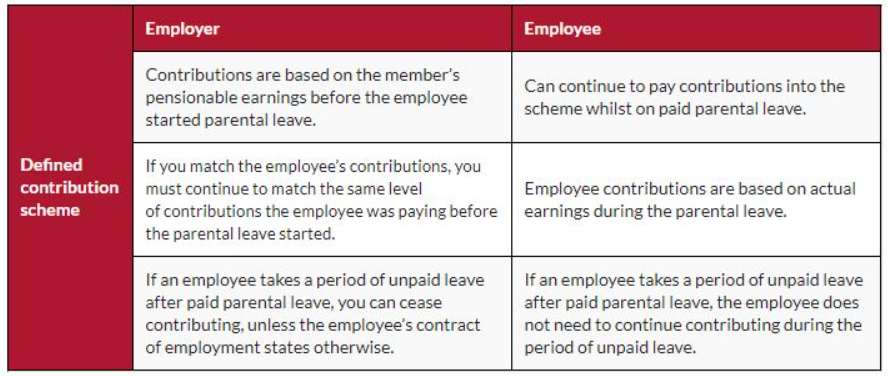

- If an employee takes parental leave, they should remain a member of the staff pension scheme, and both the member and the employer will continue to make contributions, unless the member decides to stop contributing. In this case, the employer can also stop their contributions and the member will be treated as having left the scheme.

But what about salary sacrifice?

Pension salary sacrifice arrangements are essentially the same as other salary sacrifice arrangements in all respects, save for a debate about the position during unpaid maternity leave. Most legal opinion believes that HMRC guidance on salary sacrifice indicates that HMRC considers pension contributions to be a ‘non-cash benefit’ for maternity leave purposes, as are childcare vouchers.

Employer pension contributions should continue during any paid period of maternity leave at the same rate as before leave, based on the employee’s actual salary. Any matching employee’s pension contribution only needs to be based on the pay they are receiving at the time (i.e. SMP).

However, ‘normal’ under a sacrifice arrangement may be the total pension contribution, i.e. if an employer contribution is 5% and the employee’s 3% into a DC scheme. The employee makes their contribution by salary sacrifice, making the employer’s normal contribution 8%. As a salary sacrifice arrangement is a contractual change, the employer is required to continue to contribute 8% as if the employee were in receipt of full pay.

Employees in receipt of statutory maternity/paternity/ adoption pay cannot have a contribution deducted as statutory payments are protected earnings. As such, the amount cannot be recovered from the employee, so the employer must fund the full contractual employer pension contribution.

An employee will need to take their own legal advice. Employers with salary sacrifice arrangements may need to consider placing caps on sacrifice to ensure that the employer doesn’t end up holding the baby!

– Karena Woodall, Wealth Management Consultant, February 2017