Not only is it possible to secure yields in bond markets in excess of 5%, but high-yield equity also provides comparable yields, along with the prospect of share price growth. The UK market leads the world in high-yield equity – yielding more than the other developed markets and over double that being generated from the US. With interest rates likely to fall over the next year or two, this is a window of opportunity not to be missed.

The past few years have been fraught with unforeseen challenges, from enduring a global pandemic that shifted lifestyles dramatically, to increased geopolitical tumult. As investors, we have had to confront inflation and rising interest rates for the first time in a decade. We have in the last few years alone lived through more ‘once in a blue moon’ events than most of us could ever have imagined. I, for one, would be happy never to hear the word ‘unprecedented’ again. However, amid the tumult, there is some good news, rising interest rates have created a better environment for income investors.

The prospect of near-term central bank rate cuts, following a round of aggressive monetary policy tightening, provides an attractive backdrop for fixed income investors. Following a decade of low bond yields, where there was no real alternative to the stock market as a source of inflation-protected income, equities must now compete with bonds for investor attention.

In our view, the broad equity versus bonds debate misses an important nuance: the potential for the long-term outperformance of equity income. It is safe to assume that central banks are at (or near) the peak in interest rates in much of the developed world. As such, we need to be prepared for falling rates over the medium term. While this creates a relatively stable environment for bond yields, it also provides a more benign backdrop for well-managed companies, making it easier for them to pay and grow their dividends. In our view, it is a mistake to assume that the brighter sentiment will deliver a rising tide that lifts all boats; inflation is unlikely to disappear as an issue, and uncertainty prevails. As such, investors must take this into account when making decisions.

We believe that delivering a (well covered) dividend is the hallmark of a high-quality company. When a company establishes an enduring competitive advantage over its peers, it often starts paying out regular, rising dividends. An exceptional company first must show it has predictable, long-term earnings in order to sustain dividends and this reliability matters more to investors than a spike in short-term earnings growth. Conversely, companies with weak business models, unreliable earnings and a vulnerability to disruptions are unable to sustain dividends (or even pay one), leading the market to ultimately value them lower over the long term than their dividend paying peers. In addition, when we factor in the impact of capital returns, share buybacks, and the erosion of fixed income purchasing power in an inflationary environment, the propensity of businesses to grow their dividends becomes an important consideration for income investors.

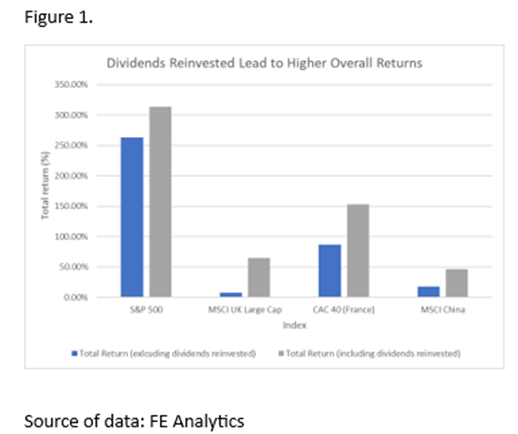

A portfolio of high-quality companies set to deliver reliable long-term returns is not the only benefit of equity income investing. The ability to reinvest dividends can supercharge long-term returns thanks to the power of compounding. The chart in figure 1 illustrates the impact that dividends reinvested can have on overall returns.

The need for active management is another crucial factor. The key to generating a consistently high and growing income has been to look broadly across a range of markets, drawing in diverse sources of growth and mitigating concentration risk. It can also help to own dividend paying companies at different levels of maturity, as in general, more established companies are likely to pay out a lot of their income in dividends. However, it is also important to include growing companies that have the capacity to increase their dividends in the future.

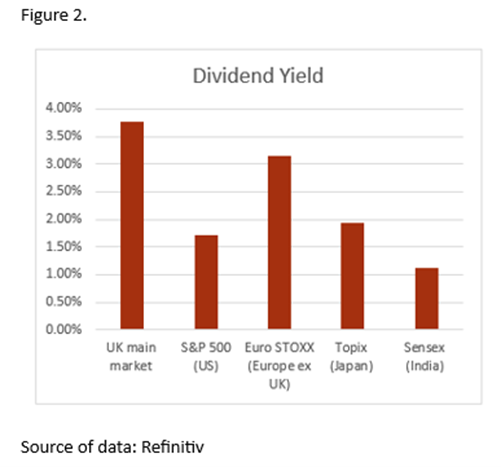

While we advocate a geographically diverse portfolio, we cannot ignore that the lion’s share of income producing companies are listed in the UK. Historically, the UK has generated an attractive dividend yield relative to alternative regional markets. As at today (22 March 2024) the UK market yields more than nearly all other developed markets and over double the income generated in the US (figure 2). Even with interest rates rising rapidly over the last few years, UK equity investors still enjoy a healthy yield. This presents a particularly exciting opportunity for UK investors when we consider the newly announced British ISA, which offers retail investors an additional £5,000 tax-free allowance on top of their existing annual £20,000 limit, if the amount is spent solely on UK investments. Tax-free growth by investing in a market offering access to a variety of companies with sustainable dividends at attractive valuations? Yes please!

Macroeconomic factors have converged to provide us with this exciting, but relatively brief window of opportunity to take advantage of a sweet spot for income investing. While the returns from an income strategy are long term, this peak rate environment is fleeting and as such, we implore investors to take advantage of the opportunities. In response, we have developed the Mattioli Woods Diversified Income Portfolio as well as increasing the fixed income and equity income exposure across our core strategies. The Mattioli Woods UK Dynamic Fund, which invests solely in UK equities, has exposure to a wealth of companies paying out sustainable dividends and will be an eligible holding within a British ISA. We have plenty of options to help you capture this ‘blue moon’ for income investing and lock in attractive returns for the long term, ultimately helping you to achieve your financial goals.

The value of investments and the income from them can fall as well as rise and investors may not get back the full amount invested. Past performance is not a guide to the future.

This article has been produced for information purposes only and is not intended to be an invitation to buy or act upon the comments made. All investment decisions should be taken with advice, given appropriate knowledge of the investor’s circumstances. Any forward-looking statements and forecasted returns represent the current views of Mattioli Woods and may be subject to change.

Mattioli Woods is authorised and regulated by the Financial Conduct Authority.