United Kingdom - April 2022

Our theme this month, in our new format, is spring. The season that (in the UK at least) sees longer days and warmer (ahem, usually warmer) weather is upon us, and the reality that we have to get into the gardens before the weeds take over is very real for the green fingered.

According to T. S. Eliot, humankind ‘cannot bear much reality’ and it is difficult to disagree. The positive implication of this is that we have a built-in optimism. This is probably what allows us to overlook some risks and, however much the evidence is to the contrary, retain a belief that things will get better. We keep getting brief suggestions that the Ukraine/Russia conflict will be de-escalated only for a lack of progress to be reported. In reality, even if we do get some sort of resolution there are going to be continuing problems of policing any such deal, so instability is likely to continue for a protracted period. The instability and volatility caused by sanctions are surely likely to persist too given that removing them immediately as part of any deal would create moral hazard. Similarly at home, we look for positives in the face of a building body of evidence that things are going to be very tough. The cost-of-living crisis is here but will certainly grow in severity over the rest of this year. In his Spring Statement, the Chancellor was only able to offer meagre assistance to those who are likely to struggle with energy and food bills and the stage seems set for social and political debate over what more should be done.

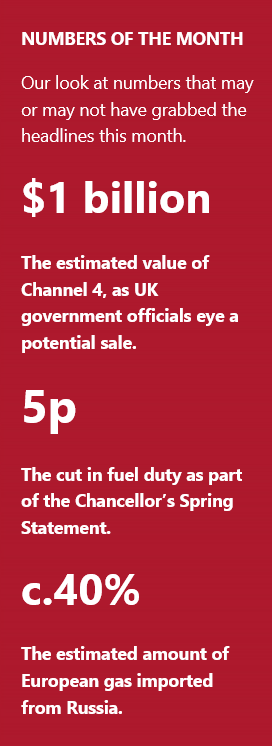

Tinkering with national insurance and an expected trimming of fuel duty are not going to move the dial as energy bills, which have doubled for some, start to hit the doormat. More UK firms are now planning to raise prices than at any time since the 1980s and it feels as if structural price pressures are becoming entrenched. Clearly the UK housing market is driven by its own factors, but it is increasingly difficult to reconcile what is happening in the wider economy with the fact that UK residential prices are up by more than 14% over a year. The house price-to-earnings ratio is at an all-time high and the prospects for affordability look bleak considering the pressure on household finances elsewhere. The UK is not unique in this regard but does have an especially inflated housing market compared to many and the historical susceptibility to inflation means that both the UK economy and society face major challenges over the next few years.

The supply side consequences of the Covid-19 crisis and the Ukraine/Russia conflict could not really be planned for by governments, but the pressures facing households are real and inflation has now entered the real economy rather than just asset markets. This has huge implications for inequality and, potentially, for markets at some stage.

So, there is not exactly indifference to the problems in the real economy, but the markets (as ever, for markets read investors) seem remarkably blasé about the events unfolding. Faced with geopolitical conflict and interest rate expectations rising across the globe, equity markets have, in the main, recovered to levels above where they were before the conflict began. Pretty remarkable. Some of this of course is due to the fact that bond yields are drifting higher and the fixed income space is seen as offering less than a safe environment for investors. Also, there is an acceptance that yields are going higher but a hope that inflation will be contained to a sufficient degree not to undermine equities.

There is also perhaps the naïve view that bonds and equities will continue to be negatively correlated – something that is far from having been the case historically. Considering that commentators are now seriously discussing whether tightening will induce a recession, it doesn’t seem as if current market levels are accurately reflecting the risks that are facing investors, though that is not to say there isn’t increased daylight ahead. Equities do protect well in inflationary environments up to a point, and they do survive a rate tightening cycle if earnings remain robust, but a recessionary environment with some inflation? That is a different story altogether. For now, drastic reductions in risk do not seem warranted, but the issues we have warned about seem to be becoming more palpable.

There is certainly a lot of reality to bear for investors. We won’t be shying away from confronting the challenges ahead and retain our usual attitude of questioning received wisdom and consensus views. We are also investors and believe in being invested for the long term where that is palatable for the client.

Term or word(s) to watch:

Recovery.

Typically, this refers to a return to a normal state of play, whether it be in terms of physical health, mental health or even economic health. The sense that we were finally over the worst of Covid-19 gave an intense belief that the economies of the world would quickly move on. Of course, in reality, the recovery is being threatened by the effects of the virus on the mechanics of global trade and supply chains, and the war in Ukraine has created the impression that the recovery was but a false dawn. Human beings are robust though, and what is necessary now, as always, is the possession of hope without which recovery never stands much of a chance. Are we going to see all the problems facing the global economy and markets disappear overnight? No, but the road to recovery is rooted in optimism and the belief that better times lie ahead.

North America - April 2022

Well, we now appear to be dealing with a much more hawkish Federal Reserve. The yield curve is starting to invert in several places (shorter-term rates yielding more than longer-term ones), which is often seen as a sign of difficult conditions ahead. Recession is something that commentators are now starting to talk about and, if the central bank is serious about controlling inflation, then it might be that this is what has to happen. Of course, this would not be pretty for equity markets but neither will allowing inflation to become entrenched in the economy. Mostly supply side in cause, if the strong economy means that wages start to enter an inflationary spiral, then the game will have changed – a recession is typically needed to turn around a ‘wage cycle’. For now, the labour market remains tight with almost half a million jobs being added in March to give an unemployment rate of just 3.6%.

Bond markets are now starting to more obviously show the inherent weaknesses that we knew exist and some expect the 10-year bond yield to move out to 3% in the coming months. This will likely place further pressure on the technology space, but although we might think cyclicals and value-led sectors will benefit, the prospect of a recession being induced might cause pause for thought. That said, value has enjoyed a decent run relative to growth names and this has benefited the more value-oriented US funds on our investment list. If we do get stagflationary conditions, financials might find the going tough but utilities, property REITS and energy have a strong historical record in low growth/high inflation conditions and funds with these sector exposures should benefit.

The US may have some defensive characteristics in times of market angst, but at high valuations these look less convincing, and we would not be adding to direct US exposure. Themes remain our way to go here – insurance has been very helpful indeed and healthcare remains a solid long-term bet in our view.

Europe - April 2022

The war in Ukraine continues to cause uncertainty over the economic outlook for Europe, with the energy dependence on Russian gas chief among the causes. Elevated gas prices have caused higher costs for both consumers and industries alike, with some industries unable to rapidly pass on these higher costs to end consumers. While there have been some arrangements made with the US and other producers to import liquified natural gas (LNG), this cannot easily replace the imports from Russia, particularly given the lack of investment in this industry over the last few years. Germany, for example, does not currently have any LNG import terminals, although has pushed to get two new ones built, meaning a significant change in its energy policy.

In recent weeks we have seen Russia threaten to cut Europe off if it does not pay for gas in roubles and a rejection of this from many countries. The political weaponisation of commodities could lead to further volatility.

Energy is not the only industry that continues to suffer from higher cost inputs. Agriculture is also coming under pressure with the price of feed and fertiliser increasing, with Ukraine having previously supplied over half of the region’s corn imports and Russia and Belarus being among the largest fertiliser exporters.

The European Central Bank remains in a tough spot, with inflation and the economic outlook uncertain. The March meeting saw headline interest rates held (at 0%) and an announcement that their bond purchasing programme – which needs to conclude before rates can rise – will end in the third quarter should conditions allow.

Elsewhere, the first round of voting in French elections takes place on 10 April. Given the number of countries in the bloc with unique political calendars, there is always political noise.

While we have been building European equity exposure, on the strengths of the companies rather than the economies, we remain cautious on the outlook and remain neutral at best in portfolios reflecting the uncertain conditions abound.

Rest of the World - April 2022

Regular readers of our various publications will know of our misgivings regarding China and that we have been removing exposure to China funds from client portfolios. We have now completed this exercise by selling exposure in even our Adventurous portfolios. It remains a controversial topic. The bulls will point to cheap valuations, recent statements from the political leadership that intervention will be reduced and the fact that it is a major Congress year and that a 5% GDP target will be met through whatever stimulus or other means are necessary.

The Chinese have the scope to reduce rates at a time when other countries are moving in the opposite direction, which could also be helpful though inflationary pressures could become a problem. We are not convinced by the arguments. In the short run, there could be a relief rally as some of the concerns go away, but longer term, China is not what it was. The forces of globalisation that were so helpful to her cause are now in abeyance and overseas investors have been made nervous by several political and economic developments.

Alternative manufacturing centres are becoming established in other Asian and also Latin American countries and China is no longer the ‘no-brainer’ choice it was for companies wishing to outsource and drive down costs. Though still a tail risk for some, the deteriorating relations with the West are a threat and sanctions may be a way off for now but will remain a background risk given the possibility of souring relations and newsflow.

Chinese New Year is also known as Spring Festival and features varied celebrations and a week-long holiday.

Latin America might be an area that benefits from a move away from globalisation and US companies moving to outsource closer to home. The region also represents an interesting way to play the commodities theme.

However, the political environment remains pretty much uniformly horrible and the skew of the available opportunities to Brazil means we are making a substantial bet on this country despite its chequered political and economic track record! Others losing faith in China may choose to look at emerging markets in Asia that are set to benefit from the changes underway and this does feel more compelling.

Some niche opportunities do undeniably exist, but emerging markets – to the degree they can be meaningfully assessed as a homogeneous category – look to be facing significant headwinds.

Spotlight on: Energy - April 2022

We have recently taken the plunge and added some thematic energy exposure to our more adventurous portfolios. Yes, prices are currently high, but the investment case is grounded more in medium-term supply challenges and the opportunities for corporates in the space to enjoy strong cash flows even at significantly lower oil prices.

Even at $70 per barrel, many oil majors would be trading on earnings yields of 11%. Dividend payouts will account for around a third of those earnings, with capex taking another third and the rest being employed in buybacks that further support share prices.

The fact that recessionary conditions (however remote at the current time) would impact the space significantly have limited our use to the most risky portfolios for now, though there is an investment case applicable to more balanced investors too. The fact remains that the renewables revolution is going to take time to materialise and, in the meantime, there will be demand for more conventional sources of energy as both an alternative and an enabler of green solutions. And let’s not forget the investments that conventional energy companies are making in these newer areas too. Where they choose to participate, they are likely to be able to establish themselves as market leaders.

The urgent need to move away from reliance on fossil fuels and also, crucially, fossil fuel producing nations such as Russia, has reawakened investor interest in other areas such as uranium. Nuclear power is likely to play a role in the energy mix, certainly for Europe (with the debate particularly strong in Germany), and uranium prices have risen strongly of late. There is even talk that the US will introduce bans on Russian uranium, which would be a catalyst for further price appreciation. So, there are some interesting niche opportunities here to play the dramatic transformation underway in the energy industry.

Non-renewable energy could help us make the transition to a green future – where we all want to be. Silent Spring by Rachel Carson is an Environmental Science book from the 1960s actually focused on the damage caused by pesticides, but which had a huge impact in raising environmental awareness among the US population.

Portfolios already have an exposure to the renewable piece through some of our environment and infrastructure holdings. If we become convinced by the investment themes for other ideas in the energy space, we will of course add these to client portfolios if we believe they can compete with our current ideas.

Fixed Income - April 2022

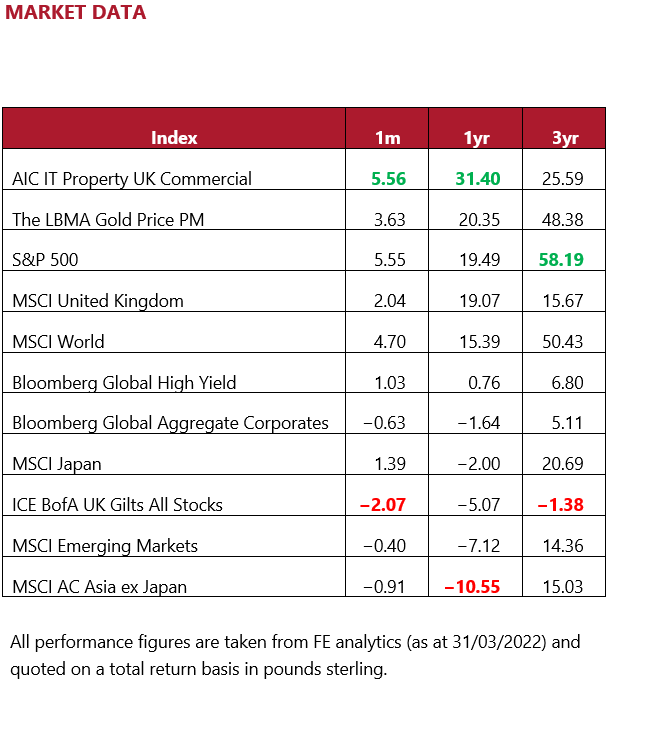

March was a negative month for fixed income assets across the board. US Treasuries had a particularly painful start to 2022 recording their worst quarter on record as yields continued to rise (which move inversely to price) over March. Despite the increased geopolitical risk investors have continued to price in an aggressive pace of interest rate rises from the Federal Reserve based on their recent communications around moderating inflation. Following the 25-basis point rise in March, seven hikes appear to be on the horizon, but the door is open for their pace to quicken and could move in 50 basis point increments, if policymakers deem this necessary.

US government debt came under fresh selling pressure on 1 April after data showed booming jobs growth in March. Although still negative for the month, price movements were less pronounced in European and UK government debt with both the European Central Bank and Bank of England committing to a hawkish stance.

The closely watched US Treasury yield curve caught investor attention as the yield on the 2-year Treasury note rose above that on the benchmark 10-year note in a so-called inversion, not once but twice in one week. An inverted yield curve tends to unnerve investors as it is seen as an indicator of a possible recession ahead. In response to this, the Federal Reserve released a statement cautioning investors not to become too pessimistic and move to risk-off mode thereby enacting a self-fulfilling prophecy.

Since the Covid-19 pandemic we have seen an even greater divide between developed and emerging market central banks. Policymakers in emerging markets did not have the luxury of postponing action until they were sure inflation was embedded rather than transitory; they had to act imminently. The upshot is that most central banks in emerging markets are now either finished or very close to finishing their rate hiking cycle as developed markets just begin. We do however see some indication that the Russia/Ukraine conflict has caused some additional pressures that may prompt further action.

The corporate debt space – though still negative – was more resilient than developed market government bonds over the quarter. January and February got off to a slow start in terms of issuance but, despite the escalation of the Russia/Ukraine conflict, March turned out to be the busiest month since September 2020 for euro investment-grade sales. Although borrowing costs have risen, on a historical basis they still look reasonably attractive at present.

In the UK, the Chancellor’s Spring Statement is one of two major financial statements given in a financial year. The duty to publish two annual economic forecasts was created by the Industry Act 1975.

We remain underweight to the fixed income sector as a whole but have taken strategic positions in areas where we see some value, such as convertible bonds and sterling corporate debt.

Commodities - April 2022

With fuel prices hitting record highs, many are wondering if now is the time to make the switch to an electric vehicle. Over the past 10 years, battery costs have fallen dramatically, making electric vehicles far more accessible. With many car manufacturers betting that battery costs will continue to fall, recent moves in commodity markets could reduce the attractiveness of the energy transition.

According to the International Energy Agency (IEA), electric vehicles require 6-7× more minerals during the production process compared with internal combustion engines. One particularly important metal for the energy transition more broadly is nickel. With the market already tight and Russia accounting for 11% of the world’s supply, prices have risen sharply.

Spot prices for another important commodity, lithium carbonate, have more than doubled in 2022 alone. Part of the reason that prices have raced ahead could be to do with the nervousness of manufacturers, scarred by the impact of the recent semi-conductor shortages and scrambling to secure future supply.

Industry estimates suggest that around a third of electric vehicle prices are accounted for by the cost of battery materials. Some have questioned whether manufacturers’ enthusiasm for electric vehicles may wane, as margins are squeezed by higher input costs and supply chain difficulties. Tesla, which arguably has the most integrated supply chain, says that it raised retail prices for cars by 5–10% in March. Other producers are likely to have to increase prices further.

Clearly, rising prices of the vehicles and charging are likely to impact demand in the short term. However, the benefits of lower emissions are clear and, ultimately, we continue to see the energy transition as a key tailwind for a number of commodities.

Property - April 2022

One area of increasing interest for UK investors is life sciences. The Covid-19 pandemic has highlighted the strength of the UK in this area and there is growing demand for space from a range of different organisations, in the public and private sectors. Governments appear to be taking more interest in the sector too, with the G9 economies significantly increasing spending towards the space in recent years and the UK government has set out a £1bn investment programme.

The type of site used ranges from purpose built assets to converted business park units. Assets tend to be concentrated in the ‘golden triangle’ of London, Oxford and Cambridge. The sector extends beyond the laboratories that many expect and into areas such as offices and data centres.

Asset managers are increasingly interested in the space and there is now a dedicated UK-listed REIT investing in such assets. AXA IM announced in 2021 that it would spend almost €2bn acquiring specialist laboratory space and offices in Europe. The sector is relatively well established in the US, with the likes of Brookfield and Blackstone reportedly have significant exposure to the sector.

Europe certainly has some catching up to do. In March, Canary Wharf Group laid out their plans to build one of the largest commercial labs in Europe. Their plan involves the development of a 22-storey site in east London into a mix of wet labs and office space.

Universities have been willing to cash in on the spike in interest. Magdalen College is selling a stake in the Oxford Science Park, in order to aid development. According to the Financial Times, the price tag represents a seven-fold increase in value since they purchased the asset five years ago.

There is a breadth of options in the UK-listed REIT space. Life sciences is an area of interest and we do have a small amount of exposure through our Property Securities Fund. We continue to follow developments in the sector closely.

The Monthly Market Commentary (MMC) is written and researched by Simon Gibson, Richard Smith, Scott Bradshaw, Jonathon Marchant and Lauren Wilson for clients and professional connections of Mattioli Woods, and is for information purposes only. It is not intended to be an invitation to buy, or to act upon the comments made, and all investment decisions should be taken with advice, given appropriate knowledge of the investor’s circumstances. The value of investments and the income from them can fall as well as rise and investors may not get back the full amount invested. Past performance is not a guide to the future. Mattioli Woods is authorised and regulated by the Financial Conduct Authority.

The MMC will always be sent to you by the seventh working day of each month, usually sooner, is normally delivered via email, and is free of charge as the MMC is generally made available to clients who have assets under our management in excess of £200,000, and to all clients under our Discretionary Portfolio Management Service (DPM). Normally, the MMC costs £397 + VAT per annum. Professional advisers and their clients should contact us if they are interested in receiving a monthly copy.

Sources:

www.bbc.co.uk,

www.bloomberg.com,

Financial Express,

www.thedragonsblade.com,

www.express.co.uk,

www.pitstoppin.co.uk,

www.sibcyclinenews.com,

www.vr-12.com,

www.smalltalkbigresults.wordpress.com,

www.anonw.wordpress.com

www.avantida.com,

www.plazmedia.com,

www.viewzone.com,

www.mmn.com.

All other sources quoted if used directly; except fund managers who will be left anonymous; otherwise, this is the work of Mattioli Woods.