United Kingdom - August 2021

Our theme this month is work. August is often the month where the workers of continental Europe, and many in the UK, do quite the opposite and head for a holiday. However, recent and (as we see it) imminent conversations about the nature, locations and even hours of work brought us to pick work as our theme.

Property company Landsec deserve kudos for their marketing department, who put out a headline ‘Majority of workers have already returned to London offices’ when in fact the truth was ‘over 70% of London office workers have already started to spend at least one day in the office’. So, 70% are spending about 20% of their time back in?

Further afield, Spain is set to become the first country in the EU to try a 32-hour, four-day working week. In the Netherlands, while not countrywide, a four-day working week is relatively normal following an experiment started in the depths of the 1990s recession as companies tried to save money by shortening working hours. Although Winston Churchill is often quoted as having originated ‘Find a job you love, you’ll never work again’, this can be traced back to Confucius. Writing and thinking about work has been around as long as anyone could define the word. It just feels different now, and that is important for investors.

If as a result of new ways of working (whether the advent of more working from home, shorter working weeks, new tech and more) we can see productivity gains, then, in the UK in particular, there could be significant benefits for investors. UK listed equities lag their global counterparts significantly, a situation exacerbated by the Covid-19 pandemic. It seems unthinkable that at some stage, despite some clear sector differences (the UK is tech-light, for example), this won’t be reversed. When that happens, the UK may outperform other global markets in a meaningful way. As ever, a date would be nice …

Our editors are loving the Olympics from Tokyo and seeing Team GB perform so well in so many areas, surprising many along the way, might just be a metaphor for the potential surprise that could come from UK listed equities. For now, riding the coat-tails of a global recovery feels fine. We continue to prefer the excess potential of smaller companies, though not without some enhanced risk.

Term or word(s) to watch: coal – statistics show that in the UK, coal is almost at nil in respect of power generation. One of the most carbon-intensive fossil fuels, and responsible for harmful air pollution, huge progress has been made in reducing the use of coal across the power sector, now accounting for only 1.8% of the UK’s electricity mix last year, compared with 40% almost a decade ago. Other countries aren’t doing so well …

In 2019, coal-powered energy accounted for more than 57% of China’s energy consumption. Just last year, China added 38.4 gigawatts of coal-fired power to its capacity – more than three times the combined amount built that year in the rest of the world. However, climate change has arrived in China, as in the rest of the world, and in some areas power has been rationed due to unseasonably high temperatures resulting in overloaded power grids. President Xi Jinping’s push for carbon neutrality by 2060 has cut coal output, which in turn has raised prices. Coal still matters.

The momentum behind cleaner energy looks assured; this will shine an increasingly bright light on coal in particular. Expect to read and hear more in the coming months. Listen out for the canary …

North America - August 2021

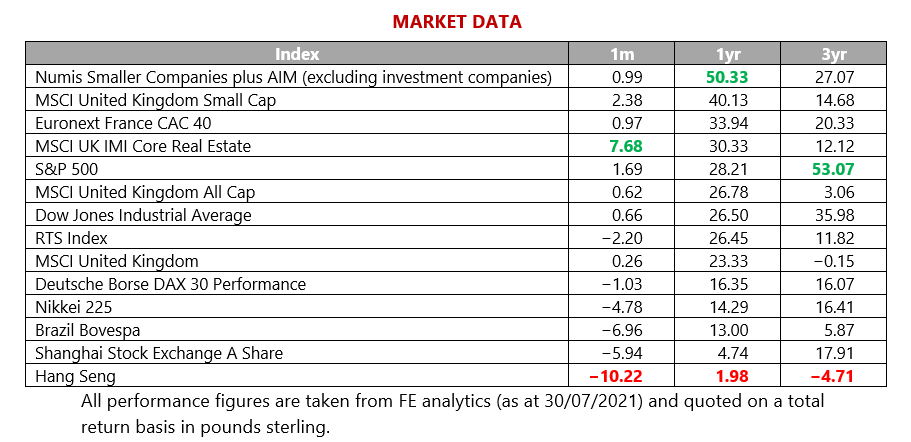

US markets made modest gains in July with the S&P 500 returning 1.69% for the month. The overall figure does however mask the underlying inconsistency over the month with the index hitting record highs one day then faltering the next. US markets remain embroiled in a ‘tug of war’ between positive earnings reports and economic data plus fear over economic growth and the tapering of accommodative monetary policy.

The Federal Reserve (Fed) must walk a fine line between keeping inflation contained while nurturing a fairly fragile recovery. Following some slightly more hawkish comments in June, the Fed assuaged market anxiety after the July meeting by opting to maintain its current accommodative policy stance. Fed chair, Jay Powell, was careful to acknowledge the continued risk to the recovery posed by the current uptick in cases resulting from the Delta variant of the Covid-19 virus. Powell’s recent comments have given investors greater confidence that while the Fed is monitoring whether inflation is becoming more entrenched, they are cognisant of the harm that tightening monetary policy too soon could cause to economic growth.

Towards the end of the month US gross domestic product (GDP) data disappointed analysts. For the second quarter of 2021, the US economy grew at an annualised rate of 6.5%, falling short of the 8.5% figure analysts had anticipated. The dollar – which had been on a downward trajectory – slipped further after the data was released. Curiously, the weaker than expected US growth data buoyed investor sentiment as it cemented expectations that the Fed would maintain its pandemic-era stimulus.

The consensus is now that we are unlikely to see tapering before early next year with the expectation that the Fed will provide ample notice. Once again, bad news in the data meaning a positive reaction in risk assets.

Over the coming weeks we will be closely watching the US senate and their mission to complete work on the long-awaited $1tn infrastructure investment bill. The bill will deliver incremental new funding for public transit, roads and bridges, and other physical infrastructure as well as a rare bipartisan victory to President Joe Biden. The outcome of this deal sets the stage for the next debate over the Biden administration’s much more ambitious $3.5tn package that includes extensive ‘human infrastructure’ programmes and services, including childcare, tax breaks and healthcare that touch almost every aspect of US life.

Few people can hear the words ‘working nine to five’ without hearing the tune of Dolly Parton’s infectious hit from the movie of the same name, 9 to 5. Dolly actually wrote the song on the film set using only her acrylic nails as an instrument to work out the melody. How is that for workplace ingenuity?!

We continue to invest selectively in US equities, favouring specialist funds in our preferred sectors, namely infrastructure, technology and healthcare.

Europe - August 2021

There is a fair amount of optimism surrounding European stocks at the moment. We have been sceptical for some time of the region’s prospects, but over the last year we have started to add allocations across portfolios. The most recent ECB meeting suggested that accommodative monetary policy is here to stay, which should provide significant support (though it is true that some commentators fear government Covid-19 schemes could be withdrawn too soon).

If we compare the US with Europe, the former is much further ahead in the reopening of its economy, so there is likely to be more to ‘go at’ in Europe. True, there has been the odd disappointing data print – German business sentiment, for example – but most of the recent economic releases have been positive and the feeling is that a corner has been turned. Clearly developments over the Delta variant are going to be highly influential in terms of short-term returns, but one can make the case that things are under relative control on the continent. When economies reopen, we may of course face new challenges on the containment front; for now, a modest allocation (from being underweight) seems justified.

The growing distrust over China and the extent of interventionism in Chinese companies could well represent an opportunity for European exporters, as investors will wish to maintain exposure to the Chinese economy while having greater ‘protection’ through names listed elsewhere. Many European stocks are significant multinational exporters, and the European market could become an interesting, alternative way of accessing China in the new climate.

For those who fret over the debt levels of sovereigns in Europe, the possibility of an inflation shock might not even be a bad thing (to some degree) as it will enable an easing of some of the accumulated debt in real terms.

For various reasons, some of which are obvious, wealthy developed nations’ workers typically work less than those in developing countries. The Netherlands takes the crown for the continent’s fewest hours worked on average, though Greece, Spain and Italy saw reductions of almost 20% in total hours worked over the pandemic-hit 2020.

We can’t shy away from the fact that a stalling of the recovery will impact in this space (and possibly more so than elsewhere given market dynamics and characteristics), but on the base case scenario of a sustained recovery, Europe looks a fair bet, by which we mean decent value.

Japan - August 2021

Over July, Japanese equities were relatively flat, lacking momentum in either direction and finishing behind both the US and European markets. Domestically, the Delta strain has caused an extension of the state of emergency in Tokyo, with cases having spiked over the last month.

At the end of July cases topped 10,000 nationally for the first time, with over a third of these being in the capital city. Progress in rolling out vaccines has been slow in Japan, with less than 30% of the population vaccinated, compared to 72% in the UK.

Japan’s global leaders (equities) also stumbled as concerns over global growth more widely saw a pullback in markets. Of the corporate results that have been announced, there has been mainly positive earnings surprises; however, uncertainty remains with the influence of the virus not yet in the rear-view mirror.

The Japanese word monozukuri, literally translated, means to make (zukuri) things (mono). There may be much here that is lost in translation. A better meaning in English would be ‘manufacturing, artisanship, or making things by hand’. However, even this does not do justice to the weight and influence this idea has in Japan. Monozukuri is the very essence of the Japanese work ethic, always striving for perfection.

We are constructive on the medium-term outlook for Japan, despite it being a laggard compared to its developed market peers when it comes to tackling Covid-19. Further corporate reforms, high quality global companies and relatively cheaper valuation levels remain positive for Japan.

Asia Pacific - August 2021

The recent actions of China have had ramifications across wider Asian markets and left many of them at levels not seen for around seven months. Interventionism and regulatory crackdowns have induced panic in the tech sector, and it is no surprise to see Hong Kong listed shares subject to sell-offs as a result. US and indeed other investors are probably questioning their exposure to the country as they see the regulatory and economic risks increase. Markets do tend to behave dramatically in situations like this, with events in one country even leading to consequences across entire regions, which is partly a reflection of investors being rather undiscriminating when under pressure.

Exceptional opportunities can be thrown up by such falls though and let’s remember that not every market is in the doldrums. If China proves too much for your risk tolerance, perhaps Taiwan is an alternative market that enables access to the Eastern Asia region’s growth story. Yes, the relations with China represent a challenge, but the market is up over 20% this year while mainland China shares are still way off their previous highs.

The key to Asia is always going to be diversification and flexibility. China may struggle at times, certainly internationally, but her importance in Asia will probably prove largely unchanged and if there are also difficulties regionally there are other countries that could step up to offer new supply chains and markets (Vietnam being an obvious example).

Many Asian country workers put in exceptionally long hours, though interestingly this is not always accompanied by greater productivity. Indeed, South Korea has introduced legislation to restrict the maximum number of working hours per week to 52 (previously 68) in an attempt to improve living standards in the country. It even hopes to improve the birth rate via these measures – we’ll leave that for you to work out.

One of the key selling points of Asia from an equity investment perspective has always been the sheer diversity of the region, and this remains undiminished. We are minded to view material pullbacks in equities in the region as buying opportunities rather than signals to reduce holdings, and allocations remain unchanged.

Emerging Markets - August 2021

We invest in companies, not economies and we are constantly reminding ourselves of that. However, there are circumstances in which companies are unattractive on the basis of the economy in which they operate or the actions of those in charge. Brazil provides a case in point. The appointment of President Bolsonaro in 2019 was seen as an exciting change for Brazilian corporates, a pro-business leader who was unafraid to tackle some of the big issues that have dogged the country for so long.

Fast forward two-and-a-half years and President Bolsonaro finds himself in a desperate position. The death toll from Covid-19 is estimated to be in excess of half a million and Johns Hopkins University data suggests that the country ranks among the worst for deaths (per 100,000) in the world. The procurement of vaccines has come under intense scrutiny too, with claims that civil servants were under pressure to pay a premium price for the Covaxin jab, despite other vaccines being far more progressed in clinical trials and irregularities with the paperwork for the deal.

Elsewhere, Ricardo Salles, Brazil’s Environment Minister has resigned from his post, having presided over a significant rise in deforestation in the Amazon rainforest. Yet more corruption surrounds his resignation, with federal police investigating reports that he colluded with illegal loggers during his time in office.

The President himself is now under investigation over claims he made around election fraud, which prosecutors claim are baseless. The remarks could see the incumbent barred from standing in the 2022 election. The move would potentially pave the way for former leader Lula Da Silva, who has recently spent almost two years in prison following a corruption conviction, recently annulled by the Supreme court.

The country is suffering from its worst drought in almost 100 years, leading to water shortages and power outages and inflation is spiralling out of control. Commentators now expect the central bank to enact its biggest rate rise for two decades in August.

Work is a particularly contentious issue in Brazil. The labour reforms of 2017 caused great controversy. Restrictions on working hours were increased from a maximum of 8 hours to 12, and the way in which employees take their 30-day annual vacation was amended.

We have consciously avoided direct allocations to Brazil for a long time. The volatility induced by the political situation is far too great. True, there may be some great companies in Brazil, but we feel that allocations to broad emerging markets give us exposure to only the most exciting names.

Spotlight on: Private Equity - August 2021

Private equity firms have been busy in the UK of late. So far in 2021, 124 deals with a combined value of £42bn have been struck (according to Dealogic), the highest value since records began in 2005. Morrisons, the AA and Asda are a selection of household names that have been targeted by private equity firms recently and there could be more to come.

As a reminder, private equity managers raise pooled funds that typically seek to identify businesses that are fundamentally undervalued, either in terms of company assets or future growth potential, then buy them and conduct various initiatives that help to translate this potential and increase the firm’s value. This could be through restructuring, bolt-on acquisitions or using sector specialist expertise to improve.

Once they feel that the business is correctly positioned, they will then look to exit. This could be through initial public offerings (IPOs) where the company goes public, through trade sales to other private equity managers, or via sales to rival companies (strategic buyers).

One reason the UK has been a popular destination for private equity buyers is the attractive relative valuations on offer, with the UK trading on a discount to many developed market peers (as referenced earlier). While markets as a whole have done well, that doesn’t mean that there aren’t plenty of bargains to be had. Private equity buyers have a particular eye for asset-backed businesses and the likes of Asda, Greene King and John Laing all had real assets on their balance sheets that underpinned the market valuation.

We have been buyers of private equity vehicles for some time. We feel that their ability to take a long-term view on businesses and their relative attractiveness bears out in performance numbers. Many of the listed private equity vehicles themselves remain at discounts to their net asset value, and we remain buyers.

Fixed Income - August 2021

When considering fixed income, the two principal considerations are interest rate risk and credit risk. Interest rate sensitivity is measured through duration, which measures the move in the price of a bond, given a change in interest rates. The duration of a bond is determined by a range of factors, including time to maturity and whether or not there are options attached to the bond. The longer the duration, the more sensitive a bond is to changing rates (as there are more years of coupons until the principal is repaid).

Much of the recent movement in prices in sovereign debt markets has revolved around expectations on potentially higher inflation and global growth. Higher inflation would expect to be accompanied by higher interest rates, either to control inflation or to ensure the real (after-inflation) appeal of new bonds. It is these expectations that have seen movements in the prices of sovereign bonds, particularly those with shorter duration.

From this we can infer that market expectations are that higher inflation expectations are transitory rather than permanent, as we would have expected more pronounced movements otherwise for longer dated bonds.

The second risk type is credit risk, which is related to default rates. For bonds from risky lenders, such as companies with higher levels of debt or weaker businesses, lenders demand to be paid a higher rate. Sovereign debt is generally considered the safest debt, particularly that of US Treasury bonds, given the low likelihood of the US government not repaying their debt.

The amount on top of this (nearly) risk-free rate, to accept the higher risk, is known as the spread. Spreads can get wider or narrower depending on market conditions, as the likelihood of higher defaults increases in more difficult market conditions. This would see investors selling bonds so prices would fall, and yields would go up (as these have an inverse relationship).

Spreads on corporate bonds have been relatively low, which partially reflects the intervention in markets by central banks buying issuance, but the absolute yield figures and income available is quite low, often giving a meagre return once inflation is considered. Higher yielding credit from riskier companies looks more attractive but does carry more sensitivity to the risks of global growth being further disrupted.

Generally, sovereign bonds are not currently attractive investments given the low yields available throughout the market, particularly with the threat of rising inflation making these worth even less in real terms. However, they do play an important diversification role in portfolios. There are real returns available from high yield (and emerging market debt), but these are not risk free. Fixed income is a fascinating but far from straightforward area right now.

Commodities - August 2021

Everyone seems to have written off oil investment and we have certainly preferred to invest down the alternative energy route, but we have to acknowledge the very long-term timeframes over which change plays out. One analyst has recently noted that even if all cars went electric and all oil-fired power stations were decommissioned as of today, two-thirds of the global oil demand would still be intact given the consumption from the shipping, aviation industries and others. This may miss the point, namely that those very industries are themselves at risk as the global consumer demands change.

Western oil companies are certainly under pressure and are seemingly repositioning their businesses in the face of an existential threat; realistically, things are going to take time and writing off oil completely is unwise (and somewhat impractical).

We have also written before about how green technologies and a cleaner economy are going to involve significant commodity extraction demands (copper, lithium, aluminium, etc.), which will create tensions in investor thinking and principles. How this plays out will be interesting and is far from clear.

For obvious reasons, adverse developments in the global economy caused by the Delta variant (and any new ones we are treated to) are going to arrest the upwards march of the commodities space (and we have seen that a bit recently), but they ultimately look like a decent place to be. The bond markets are sending conflicting messages about whether we should be concerned about inflation or growth prospects. On the balance of probabilities, a decent global recovery looks achievable and the possibility of this inducing an inflationary surprise means commodities are well placed.

Gold has been through some difficult spells, though the recent falls in US real yields to record lows should in theory be very helpful to the cause. You can still articulate an excellent case for gold particularly if the global economy makes measured headway, but supply constraints create inflationary pressure. Gold (and silver) miners may find themselves in an enviable position should this outlook materialise, and we maintain strong exposure in this area.

Property - August 2021

UK commercial property continues to benefit from the reopening of the economy and the associated greater certainty on future earnings. Of the investments trusts that have reported, the second quarter has seen positive net asset value growth, with industrials leading the way.

Industrials continue to be an in-demand area, with the trend of ecommerce having been accelerated by the pandemic. Out of town retail parks have also been increasingly of interest, with the click and collect model also increasing in popularity and offering sufficient space to show off more bulky goods that customers may want to see in person rather than online. Office investment remains a changing space, with the disruption of increased home working still in place. Predictions of the death of the office seem overdone, but now that working from home flexibility has been proven, offices may need to be adapted to incorporate lower use rates.

This too has an impact on retail and leisure, with city and town centres potentially hit by less footfall. The lunchtime rush for food may be much slower than historically. It also remains to be seen how permanently disrupted other leisure venues will be, in particular the trend for streaming services getting new films rather than first being exclusively in cinemas initially. Some film fans may prefer to watch from home even post pandemic; this and other changed behaviour may not go away once the pandemic is over.

Much commercial property continues to see values recover as confidence improves in the UK economy and the visibility of earnings comforts. Property is not a homogenous asset class, and all buildings have distinct challenges across sectors. We continue to tilt allocations to smaller lot sizes and industrial assets.

Responsible Assets - August 2021

One of index provider MSCI’s latest offerings is the MSCI Net-Zero Tracker, which covers more than 9,000 companies and identifies some of the best (and worst) performers in terms of carbon emissions. Among the worst contributors are state-owned enterprises, somewhat ironic given the rhetoric peddled by most governments in recent years.

What the list also does is highlight climate leaders from a range of sectors, and investors will continue to debate whether these firms warrant a premium rating above peers, on the basis of their lower environmental risks.

Disclosure remains a significant impediment to truly understanding the impact of corporations on the environment. Even with improved disclosure, information can be extremely difficult to verify or even compare between companies. Indirect emissions (known as Scope 3) present the most difficulty, as they attempt to estimate the emissions created by the use of a product sold.

For example, a car manufacturer might have market leading emissions levels from production activities, but this might be materially outweighed if the cars sold are heavy polluters.

Responsibility in the workplace is about accountability and having a good work ethic. The workplace may have changed (we know ours has); the need to be responsible seems more important than ever.

One significant finding from the work relates to the Paris Agreement. MSCI has measured the level of emissions each company would need to stay within to ensure that the 1.5° C global warming target would be met. Their research suggests that this budget could be spent within the next six years.

As regular readers will know, we are sceptical about highly ambitious targets that stretch decades into the future. While they are generally a step in the right direction, the work by MSCI shows that this is an issue that requires more urgent action.

Currency - August 2021

If we use the US dollar (USD) as our measure, the Kuwaiti Dinar is the strongest currency in the world in 2021. One Kuwaiti Dinar (KWD) equals 3.33 USD. Conversely, the Venezuelan Sovereign Bolívar (VES) is the lowest valued, weakest and cheapest currency in the world today, though the Iranian Rial would run it close. There are around 4,000,000 VES to one USD. Does that matter at all? Well, not probably to most (all) of our readers, but if you are in Kuwait or Venezuela, it really might.

A stronger currency usually delivers cheaper imports – good for those manufacturers and indeed many consumers who either rely on or prefer items from outside their own country/economy. It causes a few issues too – the main one is really the flip side of the former – more expensive exports (it costs those outside the country more to buy their goods (and services).

A weaker currency therefore sees cheaper exports and weakening the currency artificially (perhaps via interest rate reductions, for example) may even be policy. A weaker currency is tough on any country that has large imports, and an example would be where it doesn’t produce oil and has to import while its own currency is weak, which is exacerbated if the oil price is inflated.

UK Interest Rates - August 2021

No news. No change.

Is that good or bad?

For those who are sat on cash and need to be, then inflation, as mentioned last month, is creating a little pain and interest rates cannot help. For those borrowing, this means that current rates, and in the UK fixed rates as far as five or even ten years out, look extremely attractive. This has helped to fuel property prices more or less throughout the UK.

The Monthly Market Commentary (MMC) is written and researched by Simon Gibson, Richard Smith, Scott Bradshaw, Jonathon Marchant and Lauren Wilson for clients and professional connections of Mattioli Woods, and is for information purposes only. It is not intended to be an invitation to buy, or to act upon the comments made, and all investment decisions should be taken with advice, given appropriate knowledge of the investor’s circumstances. The value of investments and the income from them can fall as well as rise and investors may not get back the full amount invested. Past performance is not a guide to the future. Mattioli Woods is authorised and regulated by the Financial Conduct Authority.

The MMC will always be sent to you by the seventh working day of each month, usually sooner, is normally delivered via email, and is free of charge as the MMC is generally made available to clients who have assets under our management in excess of £200,000, and to all clients under our Discretionary Portfolio Management Service (DPM). Normally, the MMC costs £397 + VAT per annum. Professional advisers and their clients should contact us if they are interested in receiving a monthly copy.

Sources:

www.bbc.co.uk,

www.bloomberg.com,

Financial Express,

www.thedragonsblade.com,

www.express.co.uk,

www.pitstoppin.co.uk,

www.vr-12.com,

www.smalltalkbigresults.wordpress.com,

www.mmn.com,

www.avantida.com,

www.plazmedia.com,

www.sibcyclinenews.com,

www.viewzone.com,

www.anonw.wordpress.com.

All other sources quoted if used directly; except fund managers who will be left anonymous; otherwise, this is the work of Mattioli Woods.