Global markets summary

July delivered a refreshing change of pace as global markets shrugged off their political jitters and got back to the business of making money. Both shares and bonds (to a certain extent) joined the party, with investors breathing a collective sigh of relief as Washington actually managed to get things done. Love him or loathe him, the Trump administration’s flurry of trade agreements and the rather grandly named ‘One Big Beautiful Bill Act’ brought something markets had been craving: clarity. It’s amazing what a bit of certainty can do for investor confidence – though the spectre of reciprocal tariffs still lurks in the shadows like an unwelcome party guest.

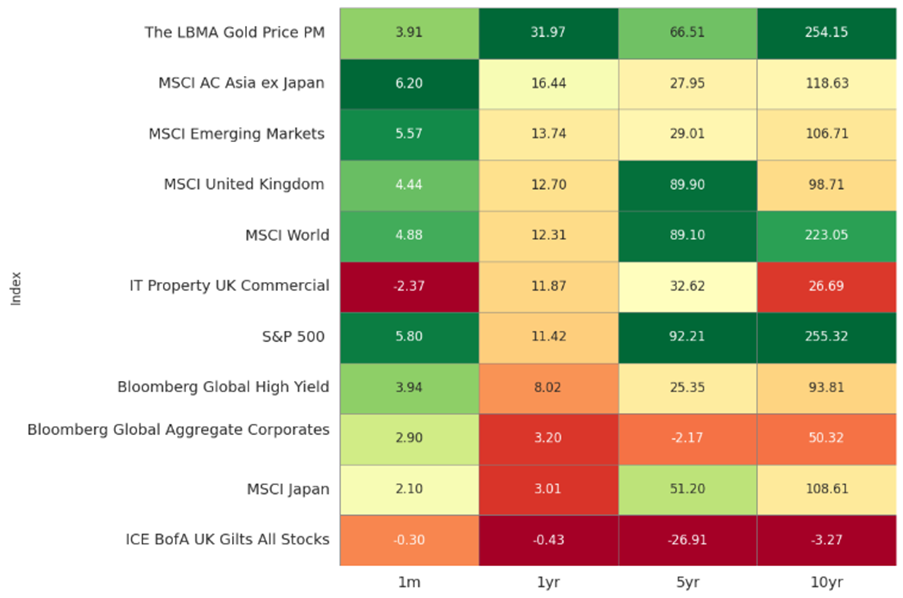

American markets led the charge, with the S&P 500 delivering a thumping 5.85% return for UK investors. The dollar’s muscle-flexing (up 3.73% against sterling) gave British holders of US assets an extra boost – sometimes it pays to look across the pond. Corporate America didn’t disappoint either. Nearly 80% of reporting companies beat expectations on both profits and revenues – a proper earnings season bonanza that left the long-term averages looking rather pedestrian. Closer to home, the UK market told a curious story. Blue-chip giants surged 5.06%, while their smaller siblings barely managed to keep their heads above water at 0.36%. It seems size mattered in July, with investors favouring the safety of the big battalions.

While equity investors were popping champagne, bond markets faced choppier waters. UK gilt holders got a nasty surprise when inflation jumped to 3.6% year-on-year. Transport, clothing, and leisure costs all conspired to push core inflation to 3.7%, sending 10-year gilt yields climbing to 4.6%. Bright spots appeared, with emerging market debt returning a healthy 3.14%. High-yield bonds also outperformed their investment-grade cousins, riding the wave of investor optimism.

Here’s where things get interesting (and slightly sobering). July’s exuberance has pushed global equity valuations to 20 times earnings – well above the long-term average of 16 times. In plain English? Markets are betting on a perfect scenario where everything goes right. At these prices, there’s precious little room for disappointment. As we start heading towards autumn – traditionally when markets get a bit temperamental – keeping a balanced portfolio across different assets and regions seems the sensible play.

July’s strong performance demonstrates the value of staying invested through uncertainty. With markets at elevated levels, we’re actively positioning portfolios to capture opportunities while protecting against potential volatility. By maintaining strategic diversification across assets and geographies, we’re ensuring your investments are well-placed to navigate whatever lies ahead – because proper portfolio management means being ready for all weather, not just the sunshine.

United Kingdom

UK equity markets delivered another solid month of returns, with the MSCI United Kingdom All Cap gaining 3.83%. However, domestic political developments created notable volatility in government bond markets. A significant reversal on welfare cuts by the Labour government, combined with Chancellor Rachel Reeves’ visible distress during Prime Minister’s Questions, sparked investor concern. Gilt markets sold off sharply amid speculation that she might be replaced by a less fiscally disciplined successor. However, the Prime Minister’s subsequent backing of the Chancellor helped calm markets.

This upward pressure on yields was not unique to the UK, with most major sovereign bond markets experiencing similar movements. Uncertainty surrounding the upcoming Autumn Budget continues to weigh on domestic markets, as a lack of clarity around proposed measures risks creating investment inertia that could further dampen economic activity.

Economic indicators presented a mixed picture during the month. UK PMI figures declined from 52 to 51, falling short of the anticipated 51.8 reading. While this level still indicates economic expansion, the disappointment was echoed by a stark Institute of Directors survey, where over 80% of respondents expressed pessimism about the twelve-month outlook, exceeding negativity seen during both the Brexit referendum and Covid-19 pandemic. Notably, this business pessimism appears concentrated on companies’ own prospects rather than the broader economy, with approximately 30% expressing optimism about wider economic conditions.

Contrasting this negative sentiment, the Lloyds Business Barometer showed business confidence at its highest level since 2015 and business intentions at a ten-year high. Banking sector earnings further supported this positive narrative, indicating underlying loan growth momentum.

The conflicting data creates a complex investment environment, yet we believe UK equities offer compelling value. The combination of an attractive dividend yield approaching 4%, increasingly generous share buybacks, and historically low valuations provides downside protection. While the UK’s growth trajectory has repeatedly faced delays, we maintain our constructive view on medium-term prospects, particularly given potential benefits from planned fiscal spending and housing reforms. When growth does materialise, we expect small and mid-cap UK companies to be the primary beneficiaries, given their domestic focus and attractive valuations. Despite near-term headwinds, we remain optimistic about UK equity opportunities.

North America

The S&P 500 climbed 2.22% in dollar terms during July, but UK investors got an even sweeter deal thanks to the greenback’s strength – pocketing a hearty 5.8% return in sterling. This wasn’t just a case of a few tech titans doing the heavy lifting either; the rally spread its wings across the market, with large-cap growth stocks leading the charge in technology and consumer discretionary sectors.

In the battle of investment styles, growth trounced value once again, riding the coattails of resurgent tech and consumer discretionary strength. Large-caps left their smaller cousins in the dust, with the Russell 1000 outpacing the Russell 2000 – it seems investors still prefer the safety of size when optimism meets caution.

Corporate America came out swinging in the second quarter, with earnings surprising on the upside across multiple sectors. Tech giants flexed their muscles while industrials showed they’ve still got plenty of fight left in them. The message was clear: demand remains robust, and profit margins are expanding nicely.

Remember all that trade war doom and gloom? July saw the US ink deals with Japan, Indonesia, and the Philippines, taking some of the sting out of tariff concerns. Progress with EU negotiations helped dodge what could have been a nasty escalation. Meanwhile, businesses had been cleverly frontloading imports to sidestep earlier tariff threats, keeping supply chains humming along. A pause in reciprocal tariffs was the cherry on top, giving sentiment an extra boost.

While the Federal Reserve (Fed) kept rates steady, markets began sniffing out potential rate cuts later in the year as inflation showed signs of cooling its heels. This shift in expectations threw a lifeline to rate-sensitive sectors, with tech and property stocks particularly grateful for the reprieve.

As we roll into August, the outlook remains cautiously optimistic – emphasis on the ‘cautiously’. The Fed’s next moves on interest rates could provide further fuel for the rally, while continued earnings strength from tech and AI-related firms might keep market leadership intact. Trade relations and fiscal policy stability will be crucial for maintaining confidence, but investors should keep their wits about them. August has a reputation for throwing curveballs, and with markets riding high, staying alert to economic data and policy shifts isn’t just sensible – it’s essential for navigating whatever turbulence may lie ahead.

Europe

European equities continued their strong year-to-date run – up 20.58% in sterling terms – but July proved trickier as the region lagged global peers. While the EU and US finally reached a framework trade agreement, the 15% tariff on most European exports (though half the initially feared rate) left investors underwhelmed. Add in a punishing 50% levy on steel and aluminium, plus warnings from tech giants about trade policy threats to 2026 growth, and you can see why the mood soured. However, despite these headwinds, the Euro Stoxx still managed to post gains over the month (2%), keeping the broader comeback story intact.

Here’s the curious thing: while markets fretted about trade, the eurozone economy quietly got on with business. GDP expanded 0.1% in the second quarter – not exactly champagne-popping territory, but better than the flat-lining analysts expected. Year-on-year growth of 1.4% beat forecasts too, even if it couldn’t match the export-fuelled surge of early 2025. Inflation behaved itself admirably, holding steady at 2.0% – bang on the European Central Bank’s (ECB) target. Core inflation stuck at 2.3%, suggesting price pressures remain contained. Employment stayed rock-solid with joblessness at a record low 6.2%, though Germany’s 6.3% rate remains stubbornly high by its standards. Economic sentiment actually improved in July, with businesses and consumers feeling more chipper about the future. This resilient data took pressure off the ECB to rush into rate cuts – good news for savers, less thrilling for borrowers hoping for relief.

We maintain a neutral outlook on European equities, as the region’s solid economic fundamentals, attractive valuations, and emerging credit cycle are balanced against lingering trade uncertainties, disappointing tariff agreements with the US, and sector-specific headwinds from China – suggesting investors should stay selective rather than betting the farm on a continental comeback.

Rest of the world

North-east Asian markets joined the global rally party, with the MSCI Asia ex Japan climbing 5.82% in sterling terms. China stole the spotlight with an 8.53% surge, while emerging markets broadly posted respectable gains of 5.57%. Even Japan’s typically subdued Topix managed a 2.54% rise.

China’s economy put on a brave face in July, with first-half GDP growth hitting 5.3% year-on-year – comfortably above Beijing’s 5% target. Industrial production jumped 6.8% in June, beating expectations, while the Caixin manufacturing PMI finally crawled above the magic 50-point mark that separates expansion from contraction. So far, so good.

But here’s where it gets interesting: dig beneath the surface and the picture becomes murkier. Chinese exporters have been frantically front-loading shipments ahead of expected US tariff hikes, while pivoting to non-US markets wherever possible. Domestic demand remains anaemic, and new export orders are actually falling. It’s rather like watching someone sprint the first half of a marathon – impressive, but can they keep it up? The consensus view suggests China’s momentum will fade as these artificial tailwinds die down. We’re maintaining a neutral stance on Chinese equities – the short-term numbers look decent, but tariff headwinds and structural challenges warrant caution.

The Bank of Japan continued its glacial approach to policy normalisation, keeping rates pinned at 0.50% as expected. What did change was their inflation outlook – core CPI is now projected at 2.7% for fiscal 2025, up from April’s 2.2% forecast. Persistent food price increases are doing what decades of monetary stimulus couldn’t: actually creating inflation.

Governor Ueda dropped hints about potential rate hikes before year-end, especially after positive trade negotiations with the US bore fruit. Meanwhile, the real economy showed encouraging signs – industrial production jumped 1.7% month-on-month in June, defying expectations of a decline, while retail sales maintained their steady 2% annual growth pace.

Yet despite these green shoots, we remain neutral on Japan.

While everyone obsessed over China, emerging markets broadly delivered solid returns. The MSCI Emerging Markets index gained 5.57%, with non-Asian emerging markets posting a respectable 3.41%. These aren’t headline-grabbing numbers, but in a world of elevated valuations and geopolitical uncertainties, steady returns from diversified emerging market exposure look increasingly attractive.

July’s performance across Asian and emerging markets tells a nuanced story. China’s near-term strength masks medium-term vulnerabilities, Japan continues its cautious rehabilitation, and emerging markets offer pockets of value for those willing to look beyond the obvious plays. With both China and Japan presenting balanced risk-reward profiles, a neutral stance allows participation in any upside while protecting against the considerable downside risks that remain. Sometimes the smartest move is acknowledging what you don’t know – and positioning accordingly.

Fixed income

July proved tricky for bond investors, with inflation concerns and political meddling keeping markets on edge. US inflation came in better than feared, with consumer prices rising 2.7% year-on-year. Trump’s tariffs haven’t bitten as hard as expected – yet. Clever companies have been stockpiling goods and rerouting supply chains to dodge the worst impacts. But here’s the rub: the Federal Reserve faces mounting pressure from the White House to cut interest rates, even as government spending balloons. This political arm-twisting pushed US Treasury yields higher, making bonds less attractive.

British bondholders got a shock when June inflation jumped to 3.6% – nobody saw that coming. Transport, clothing, and leisure costs all surged, pushing 10-year gilt yields up to 4.6%. In simple terms: your existing bonds became less valuable as new ones offered higher returns.

Not all bonds struggled. Corporate bonds outperformed government debt as company earnings remained strong. Emerging market bonds were July’s star performers, returning 3.14% in sterling terms. High-yield bonds also delivered positive returns at 1.13%.

The Bottom Line: Government bonds faced headwinds from inflation surprises and political pressures, but corporate and emerging market bonds offered brighter spots. With bond prices already reflecting cautious optimism, we’re selective about where we see value – particularly favouring emerging markets where returns still look attractive.

Ask us anything

Q: Can you explain in simple terms what’s going on with tariffs now and how should investors respond?

A: Remember when international trade was boring? Those days are long gone. President Trump’s ‘America First’ trade agenda has turned global commerce into a high-stakes chess match, with tariffs as the primary weapon of choice.

Since January, a baseline 10% tariff has become the entry fee for most countries wanting to sell to America. But that’s just the start. Steel and aluminium face a punishing 50% levy, while cars from most nations hit a 25% wall. Come August, copper imports will join the 50% club – and pharmaceuticals, computer chips, even iPhones could be next in the firing line. The drama peaked on 2 April – dubbed ‘Liberation Day’ by the administration – when Trump announced eye-watering reciprocal tariffs that sent markets into a tailspin. A hasty pause on 9 April gave everyone breathing room to negotiate, leading to a flurry of dealmaking.

The results? Mixed, to put it mildly. Japan and the EU managed to negotiate their way down to 15% tariffs on most goods (though steel and aluminium remain at 50%). The UK secured a modest victory, getting car tariffs reduced from 25% to 10% for a limited number of vehicles. China, despite negotiations, still faces tariffs north of 30%. Meanwhile, Vietnam, the Philippines, and Indonesia struck framework deals keeping their rates around 20% – higher than the baseline but avoiding worse outcomes. The price? Promises to buy billions in American goods and open their markets wider.

Here’s what matters for your portfolio: these aren’t just numbers on a spreadsheet. Trade barriers haven’t been this high since your grandparents’ generation, and uncertainty is forcing businesses into wait-and-see mode. Companies are delaying investments, postponing hiring, and some are already passing costs onto consumers.

The silver lining? Markets have shown they can rally sharply on positive trade news – the S&P 500 jumped nearly 10% when reciprocal tariffs were paused in April. Plus, governments worldwide are preparing counter-measures: fiscal stimulus, regulatory easing, and support packages that could offset some damage.

So how should savvy investors respond? First, don’t panic-sell on every headline. Second, ensure your portfolio is built for resilience:

• diversify geographically – don’t put all your eggs in the American basket

• hold quality bonds as a hedge against equity volatility

• consider inflation protection through real assets or commodities

• stay active – passive strategies are overexposed to US risk

• watch your currency exposure – the dollar’s traditional safe-haven status is wobbling

The UK market, with its defensive tilt and commodity exposure, actually looks relatively attractive in this environment. Sometimes being boring pays off.

Key takeaways

• US tariffs are at their highest since the 1940s.

• Most countries face 10%+ levies, with product-specific rates even higher.

• Trade uncertainty is dampening business investment and hiring.

• Governments are preparing stimulus measures to offset the impact.

• Diversified, actively-managed portfolios offer the best protection.

If there’s a question you’d like to pose to our team, please reply to this email or write to [email protected].

MARKET DATA

All performance figures are from FE analytics (as at 31/07/2025) and quoted on a total return basis in pounds sterling.

The Monthly Market Commentary (MMC) is written and researched by Scott Bradshaw, Lauren Hyslop and Jonathon Marchant for clients and professional connections of Mattioli Woods and is for information purposes only. It is not intended to be an invitation to buy, or to act upon the comments made, and all investment decisions should be taken with advice, given appropriate knowledge of the investorʼs circumstances. The value of investments and the income from them can fall as well as rise and investors may not get back the full amount invested. Past performance is not a guide to the future.

Mattioli Woods Limited is authorised and regulated by the Financial Conduct Authority.

Sources: All other sources quoted if used directly, except fund managers who will be left anonymous; otherwise, this is the work of Mattioli Woods.