Global markets summary

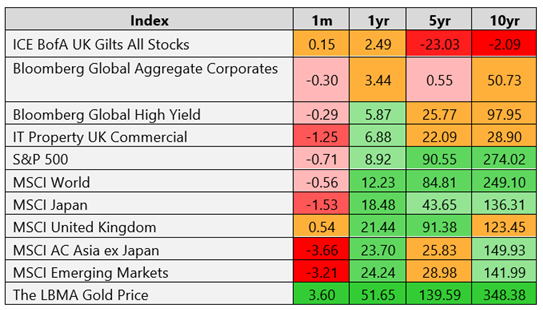

After six months of strong gains, global stock markets took a breather in November. The US S&P 500 returned -0.63% over the month in £ terms with mega cap technology stocks leading the decline. Only one of the ‘Magnificent Seven’ tech giants (Alphabet) stayed positive, with others dropping up to 13%. At the centre of this recalibration: the artificial intelligence narrative that has dominated 2025. Even stellar quarterly results from NVIDIA failed to calm nerves about stretched valuations.

UK markets stood out for their resilience. Large caps delivered 0.94% and small caps 0.28%, outperforming both the broadly flat EURO STOXX (up just 0.10%) and the technology-heavy MSCI Asia ex Japan, which tumbled 3.66%, all in sterling terms, as AI profit-taking accelerated. Meanwhile, cryptocurrency markets shed a staggering £1.2 trillion, more than Saudi Arabia’s entire annual GDP, serving as a stark reminder of the risks in speculative assets.

Policy uncertainty deepened the malaise. Markets had priced in further Federal Reserve rate cuts, but robust GDP data forced a sharp recalibration. The aftermath of America’s 43-day government shutdown left investors navigating without crucial economic indicators, thickening the fog of uncertainty. Emerging markets bore the brunt, with technology-heavy Korea and Taiwan (which have surfed the AI wave all year) suffering the steepest losses.

Fixed income provided a relative bright spot. UK gilt yields fell (pushing prices higher) after the Autumn Budget reassured markets, while sterling corporate debt also finished in positive territory.

Our core Multi-Asset Funds demonstrated resilience over the month, outperforming their respective benchmarks thanks largely to tactically-elevated cash positions and reduced ‘Magnificent Seven’ exposure. Although unsettling, this correction may prove more therapeutic than threatening. After such a vertiginous rally, the central case for many analysts is that November’s weakness was a necessary breather rather than the start of a bear market. As markets approach year end, the fundamental drivers remain intact even if the euphoria has dimmed. The lesson remains clear: what rises at breakneck speed must eventually pause to catch its breath.

United Kingdom

Headlines in the UK were dominated by Budget speculation and the subsequent fallout during November. In truth, the Budget has been the main talking point in the UK for close to three months, which highlights the arduous nature of the process and implications of consistent leaks to the media. Mercifully, the process is changing and the Office for Budget Responsibility (OBR) will check whether the Government is meeting its rules annually, as opposed to biannually moving forward. This will hopefully help to remove a period of speculation and uncertainty each year.

We will not cover the finer details of the Budget in this publication. Our focus is on market implications and, of course, your consultant is on hand to assist in relation to discuss its impact on your personal circumstances. So, what does the Budget mean for markets? In truth, not a lot. Given that the Budget was leaked over a period of weeks, with significant ‘kite flying’ of policies by ministers and the Treasury, it contained very few surprises.

This was a classic tax and spend Budget, bearing some similarities to last year. However, the main point of difference is that last year’s Budget contained several announcements that created significant inflationary pressures. While increases to welfare and the National Living Wage fail to help the situation, they don’t make it materially worse.

The most disappointing part of the Budget was what the Chancellor didn’t say. Concerningly, her speech was lacking in significant growth initiatives that could help to stimulate consumers and businesses, pulling us out of a prolonged period of low confidence.

While the Budget stole the headlines, it is unlikely to be the main driver for UK equity returns. We continue to believe that the key to economic activity and stronger equity market performance, particularly for domestic stocks, is lower inflation and interest rates. Data over November was relatively subdued, reflecting a cautious tone ahead of the Budget. This, combined with last month’s voting split, has led the market to price a December interest rate cut as a near certainty.

Beyond that, Goldman Sachs is forecasting a further three cuts in 2026, taking interest rates to 3.0%, as inflation subsides. This would be well received by households and businesses alike. We believe that these interest rate cuts should help to unlock high levels of consumer savings. This could be an important driver for mid- and small-cap equities in 2026, which tend to be more domestically-orientated and this is an area to which we remain overweight.

North America

Over November, the S&P 500 slipped a modest 0.63% in sterling terms, but beneath this headline figure lurked a fascinating reversal of fortune. The vaunted ‘Magnificent Seven’ tech behemoths, those titans that have dominated market narratives, found themselves distinctly out of favour. Six of the seven stumbled, with declines reaching as steep as 13%, while only Alphabet managed to buck the trend. Most intriguingly, the equal-weight indices emerged victorious, suggesting the market’s rank and file staged something of a quiet rebellion against their overlords.

The month’s most theatrical moment belonged to NVIDIA, the semiconductor colossus that has become synonymous with artificial intelligence ambitions. Initial euphoria greeting its robust earnings evaporated within mere hours, as investors suddenly rediscovered their concerns about potential overvaluation in the AI sector. This swift about-face epitomised November’s mercurial temperament, a market grappling with whether the artificial intelligence revolution justifies current valuations or represents a bubble awaiting its pin.

Adding intrigue to an already complex narrative, Washington’s longest-ever federal closure created an information vacuum precisely when clarity was most needed. Critical economic indicators such as inflation metrics and employment statistics all went missing in action, leaving the Federal Reserve to navigate December’s rate decision with alternative instruments. The scant data that did emerge painted a nuanced picture: jobless claims touched their lowest point since spring, yet consumer sentiment plummeted to depths unseen since April, with Americans citing inflationary pressures, trade tensions, and political uncertainties as primary culprits.

As we pivot towards year end, sophisticated investors might consider this November less a catastrophe than a healthy recalibration. After a spectacular ascent that left valuations looking rather stretched, the market appears to be questioning whether concentration risk among tech giants warrants fresh examination. The outperformance of broader indices hints that opportunity may be shifting towards overlooked corners of corporate America, a rotation that astute portfolio managers would be wise to monitor as winter approaches.

Europe

European markets displayed admirable poise in November, with the EURO STOXX finishing essentially flat in sterling terms, a feat of stability while global peers wrestled with volatility. The continent’s resilience stemmed from a pleasing cocktail of factors: financial and technology sectors delivered robust earnings performances, offsetting disappointments from automotive manufacturers struggling with shifting consumer demands. Looking ahead, analysts project a hearty 12% earnings growth for 2026, while Europe’s more balanced sector composition – lacking America’s extreme tech concentration – provided welcome ballast during the month’s turbulence.

Perhaps the most remarkable subplot emerged from Madrid, where Spain’s budget deficit has dipped below Germany’s for the first time since the early 2000s. Remember Spain as part of the infamous PIIGS quintet during the 2010-2012 eurozone crisis? That beleaguered group (Portugal, Italy, Ireland, Greece, and Spain) once threatened to tear apart the single currency with their toxic brew of excessive debt and banking woes. Today’s reversal represents an extraordinary rehabilitation story, with the former crisis patient now boasting healthier finances than Europe’s traditional economic powerhouse.

The inflation picture across the continent offered central bankers reason for cautious optimism. French prices held steady at a modest 0.8% annual increase, while Spanish inflation cooled to 3.1% and Italy’s reading dropped to just 1.1%. These benign figures suggest eurozone-wide inflation should hover near the European Central Bank’s 2% target when December’s comprehensive data arrives. Yet not everything sparkled: German business sentiment unexpectedly soured, with corporate leaders growing increasingly pessimistic about future prospects. Paradoxically, German consumers showed tentative signs of renewed confidence, perhaps sensing bargains amid the gloom.

Our positioning remains deliberately neutral towards European equities, reflecting this complex mosaic of conflicting signals. While attractive valuations and improving fundamentals in peripheral nations argue for optimism, persistent German economic malaise and automotive sector headwinds counsel patience. The continent offers neither the explosive growth potential of emerging markets nor the defensive characteristics of fixed income, instead presenting a balanced risk-reward proposition that merits measured exposure rather than bold conviction. Until clearer trends emerge, we favour selective opportunities over broad market bets.

Rest of the world

Japanese stocks demonstrated why currency matters in November. A respectable 1.42% gain in Tokyo turned into -0.72% for £-based investors after the yen weakened against sterling. Yet this currency weakness tells a bigger story: Tokyo inflation stubbornly sits at 2.8%, well above target, while unemployment remains rock bottom and retail sales surprise positively. The Bank of Japan appears ready to finally abandon its ultra-loose monetary experiment, with government bond yields hitting 17-year highs as markets brace for rate rises. For sterling investors, Japan remains a currency gamble wrapped inside an equity investment, the fundamentals look promising, but the yen keeps moving the goalposts.

Across the broader Asia Pacific landscape, November delivered a reality check after a spectacular year. Technology giants in Korea and Taiwan, those darlings of the artificial intelligence boom, faced aggressive profit taking as investors questioned whether semiconductor valuations had run too far, too fast. India emerged as the region’s bright spot, powered by domestic consumers splashing cash and infrastructure projects humming along nicely, proof that sometimes boring fundamentals trump exciting narratives. The subcontinent shrugged off stretched valuations as its burgeoning middle class continued spending with enviable enthusiasm.

China offered mixed signals that kept investors guessing. Singles’ Day (their Black Friday equivalent) delivered surprisingly robust sales, suggesting Chinese consumers still have appetite for bargains despite broader economic worries. Yet scratch beneath the surface and concerns linger; industrial profits tumbled 5.5% in October, producer prices remain stuck in deflationary territory for three years running, and the property sector hangover continues to weigh on sentiment. Beijing desperately wants consumers to replace property speculation as the economy’s growth engine, but old habits die hard when millions of savers still nurse wounds from the real estate collapse.

Our stance across Asian and emerging markets remains deliberately neutral, reflecting this patchwork of opportunities and risks. Japanese corporate reforms and Indian demographics offer compelling long-term stories, while Chinese policy stimulus and Korean technology leadership cannot be ignored. Yet with currency volatility, geopolitical tensions, and valuation concerns swirling, we prefer gaining diversified exposure rather than making bold directional bets.

Fixed income

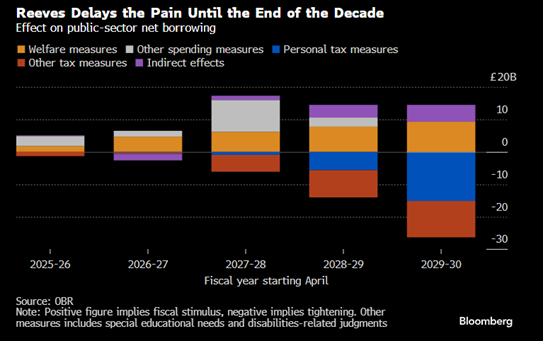

November proved eventful for bond investors, with Government debt markets swinging between anxiety and relief like a financial soap opera. British gilts initially wobbled as leaked forecasts suggested doom and gloom ahead of the Autumn Budget, sending yields climbing towards 4.56%. Yet when Chancellor Rachel Reeves finally unveiled her plans on 26 November, markets breathed a collective sigh of relief as the Government had conjured a surprisingly generous fiscal cushion, and gilt yields promptly retreated to 4.45%. With inflation cooling to 3.6% and the Bank of England looking increasingly likely to cut rates in December, gilt investors ended the month cautiously optimistic about prospects for capital gains.

Across the Atlantic, American Treasury bonds endured their own drama courtesy of Washington’s longest-ever government shutdown. The 43-day standstill left investors flying blind without crucial economic data, creating an information vacuum that pushed yields higher despite the Federal Reserve cutting rates in October. Once the shutdown ended mid-month and clearer signals emerged, the 10-year Treasury yield settled around 4.06%. Yet uncertainty lingers – markets cannot agree whether another rate cut arrives in December, with odds swinging wildly between 40% and 95% depending on the latest economic tea leaves.

Corporate bonds experienced a feeding frenzy in November, with companies rushing to borrow £134 billion globally while investors still had appetite. Technology giants and pharmaceutical firms led the charge, finding their bonds oversubscribed by three to six times despite offering relatively meagre returns. Investment-grade bonds (those from financially solid companies) look expensive by historical standards, needing only tiny price movements to underperform government debt. Meanwhile, riskier high-yield bonds delivered anaemic returns of just 0.2%, though defaults remain refreshingly rare and companies continue managing their debt loads sensibly.

The surprise winner emerged from developing nations, where emerging market bonds delivered their best monthly performance in some time. Latin American debt led the charge, boosted by stronger currencies and credible central bank policies, while African bonds also sparkled. For British investors seeking yield in a low-return world, these markets offered a rare bright spot. Our portfolios reflect this opportunity; we favour emerging market debt while steering clear of expensive investment-grade bonds and low-yielding government debt. In a world where traditional bonds offer slim pickings, sometimes the best returns require looking beyond familiar shores.

Ask us anything

Q: What are your views on the Budget and how will it impact markets?

A: The Autumn Budget delivered a ‘spend now, pay later’ approach with few genuine surprises, following weeks of political speculation and leaks. While the Chancellor highlighted upgraded growth forecasts for this year (from 1% to 1.5%), the quieter story was the downward revision to growth expectations in later years. The Government has clearly signalled its priorities: expanding the public sector and supporting specific industries aligned with Labour’s manifesto promises, while the broader private sector received limited attention.

Market reaction: from relief to reality

Markets initially breathed a sigh of relief, but the morning after brought a more sobering assessment. The key concern centres on whether the Government will actually raise the revenues it needs, particularly as the major tax measures are scheduled perilously close to the next general election, raising questions about their implementation.

Source: Bloomberg

The real market driver: interest rates, not politics

Despite the political theatre, the Budget is unlikely to be the main story for UK markets. The real catalyst for equities will be the trajectory of interest rates. With a December rate cut looking virtually certain and potentially three more cuts by mid-2026, we could see rates approaching the ‘neutral’ level of 3% – neither stimulating nor constraining the economy. This matters because lower borrowing costs typically unlock pent-up consumer savings and boost spending, creating a far more powerful economic force than any Budget measure.

Where the opportunities lie

Sector winners: The Government’s intentions are clear, creating distinct opportunities in:

- housebuilding and building materials

- construction and infrastructure

- defence contractors

- banking sector

- support services

The overlooked opportunity: UK mid- and small-cap equities remain exceptionally undervalued. While many investors shelter in large-cap stocks, these smaller companies stand to benefit most from falling interest rates and recovering consumer confidence.

Looking ahead: reasons for optimism

After what feels like a lost decade for consumer sectors, several forces could drive a rebound:

- The savings unwind: lower rates will encourage spending of accumulated savings.

- Rising incomes: higher wages and increased welfare spending will boost consumption.

- The ‘enjoy it’ effect: with minimal Capital Gains Tax (CGT) allowances and rising dividend taxes, there is increasingly little incentive to save rather than spend.

With twelve months until the next Budget, there is finally breathing room for confidence to build and economic momentum to gather pace.

The bottom line

While political uncertainty persists and consensus remains overwhelmingly negative on the UK domestic situation, this pessimism may paradoxically create the ideal conditions for UK equity outperformance. The Budget, for all its fanfare, is ultimately a sideshow. The main event – falling interest rates and recovering consumer confidence – is what will truly drive markets forward.

If there is a question you’d like to pose to our team, please reply to this email or write to [email protected].

Four key takeaways from November:

• The UK Budget on 26 November caused relief rather than panic, pushing gilt yields down.

• Six of the ‘Magnificent Seven’ tech stocks declined, ending their six-month winning streak, with only Alphabet staying positive.

• Crypto markets lost £1.2 trillion in value while emerging market bonds delivered the month’s best returns.

• In £ terms, Asia Pacific (ex Japan) markets suffered some of the worst losses at -3.66%, as AI profit-taking accelerated, while Europe stayed flat at 0.10% in sterling terms.

MARKET DATA

All performance figures are from FE analytics (as at 30/11/2025) and quoted on a total return basis in pounds sterling.

The Monthly Market Commentary (MMC) is written and researched by Scott Bradshaw, Lauren Hyslop and Jonathon Marchant for clients and professional connections of Mattioli Woods and is for information purposes only. It is not intended to be an invitation to buy, or to act upon the comments made, and all investment decisions should be taken with advice, given appropriate knowledge of the investorʼs circumstances. The value of investments and the income from them can fall as well as rise and investors may not get back the full amount invested. Past performance is not a guide to the future.

Mattioli Woods Limited is authorised and regulated by the Financial Conduct Authority.

Sources: All other sources quoted, if used directly, except fund managers who will be left anonymous; otherwise, this is the work of Mattioli Woods.