Global markets summary

December brought a year of shifting fortunes to a fitting close. UK and European markets ended 2025 on a high note, while US equities stumbled as enthusiasm for technology shares cooled.

UK equities returned 2.24% for the month. The Bank of England cut rates by a quarter point before Christmas, welcome news for an economy seeking support. A divided vote among policymakers, however, signalled that inflation concerns have not entirely faded. European shares delivered 2.39% in sterling terms. A classic Santa rally lifted the region in the year’s final weeks as investors rotated away from expensive American technology names into more attractively valued sectors: banks, defence, energy, and mining. The S&P 500 disappointed sterling investors, falling 1.46% amid dollar weakness.

Japan’s equity market rose modestly in local currency terms, though yen weakness eroded these gains for sterling investors. China posted healthy returns for the year overall, but momentum faded in December as stimulus hopes ebbed and flowed. Asia Pacific equities excluding Japan fared better, returning 1.19%, buoyed by AI-driven semiconductor demand in Korea and Taiwan alongside inflows into domestic cyclical sectors across Southeast Asia.

Over the full year, the contrast in equity markets was stark. The S&P 500 returned just 9.34% in sterling terms versus 17.43% in dollars – a gap that reflected the US dollar’s near 10% fall as trade tensions cast doubt over its traditional safe-haven status. American equities enjoyed a robust 2025, but it was global markets that truly stole the show. The MSCI All Country World ex-USA index (a broad measure of international stocks) rose, in £ terms, an impressive 23.27%, comfortably eclipsing the S&P 500’s more modest 9.34% advance.

Two themes drove much of this outperformance. In Asia, the AI boom proved transformative, with technology firms and semiconductor manufacturers riding a wave of surging demand. In Europe, equities drew strength from ambitious defence spending commitments and a brightening growth outlook. For diversified investors, it was a year that rewarded looking beyond America’s shores.

Fixed income markets enjoyed a positive year, with December adding modest gains. UK gilts and US Treasuries benefited from falling inflation and rate cut expectations. Global investment-grade bonds delivered steady returns, while high-yield bonds performed very well as investors sought higher income and credit spreads tightened. Emerging market debt also had a strong year, helped by local rate cuts and stronger currencies.

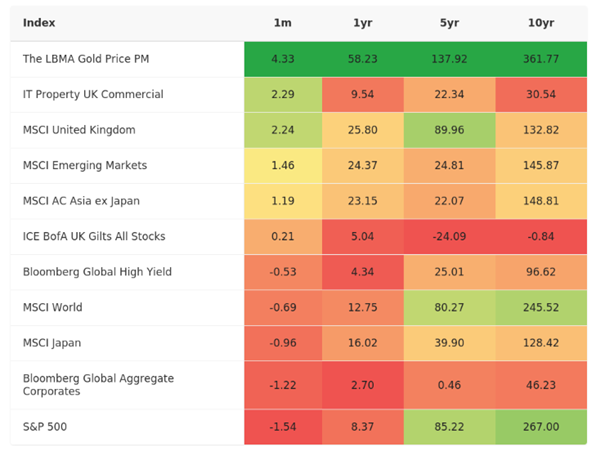

Gold was the standout performer, posting its best annual gain in decades. Record central bank purchases, global uncertainty, and falling interest rates combined to drive prices sharply higher.

At Mattioli Woods, we are relatively sanguine on the outlook for 2026. Supportive fiscal and monetary policy should sustain global growth, though elevated valuations in both equities and bonds leave little room for disappointment. AI remains a dominant theme, but investors will increasingly demand evidence that heavy capital spending is translating into genuine returns. A positive year remains our central expectation, yet market valuations are far from cheap, leaving limited room for error should the upbeat narrative begin to unwind.

United Kingdom

2025 provides a useful reminder that the economy and the stock market are two separate entities. If an investor read a broad range of newspapers every day for the past year and checked their portfolio at the end of December, they would undoubtedly be surprised to see such strong returns. While the economy failed to shake off the impact of the previous Budget and tariffs added another layer of complexity to markets, UK equities delivered a strong year.

The year began with heightened volatility following President Trump’s tariff announcements in April. The UK market initially fell 10%, though recovered swiftly as investors recognised the UK’s relatively favourable position and came to the conclusion that the effective tariff rate would be lower than initially announced.

Interest rates emerged as a dominant theme. The Bank of England began cutting rates in February, though progress stalled as inflation proved stickier than anticipated, reaching 3.8% by August, well above the 2% target. Services inflation remained particularly elevated at 5.0%, complicating the path to further monetary easing.

Political developments added another layer of uncertainty. The Labour Government’s Autumn Budget created prolonged speculation about tax rises and spending measures, dampening business confidence and delaying investment decisions. Despite campaigning on growth, concrete policy initiatives remained limited.

Market performance was characterised by stark divergence between market segments. Large-cap stocks dramatically outperformed their small- and mid-cap counterparts, benefiting from lower levels of exposure to the domestic economy. By virtue of being a bigger part of the index, large-cap names also benefited from improved investment flows, as US investors – faced with high valuations and tariff uncertainty – considered other investment destinations.

Economic data presented a mixed picture. GDP growth proved more resilient than expected, with the UK positioned as the second-fastest growing G7 economy at 1.4%. Consumer spending showed encouraging signs, with retail sales rising and mortgage approvals reaching multi-month highs. However, forward-looking business confidence indicators remained subdued, reflecting ongoing uncertainty about fiscal policy.

Looking ahead, we remain optimistic about prospects for UK equities. The political situation remains uncertain and local elections in Q2 are likely to be a pivotal moment for the Starmer Government. The lack of growth initiatives and generally weak sentiment should support more interest rate cuts in 2026, which could provide important catalysts for the domestically-focused mid- and small-cap segments, where we continue to see attractive long-term opportunities.

North America

US equities delivered robust gains in 2025, but for UK investors the picture was more subdued once currency movements were factored in. In dollar terms, the S&P 500 advanced about 16%, lifted by strong corporate earnings, excitement around artificial intelligence, and a late-year shift towards easier monetary policy. Yet sterling strengthened by roughly 7-9% against the dollar over the year. This meant that UK investors who did not hedge their currency exposure saw returns shrink to just over 8% when converted back to pounds.

December illustrated this dynamic clearly. While US indices were broadly flat or marginally lower in local currency, the rising pound deepened losses for UK investors. Technology and communication services led performance, powered by AI-related investment, while consumer staples and energy lagged.

The broader economic backdrop remains complex. The US economy grew at an annualised rate of 4.3% in the third quarter, a healthy pace, even as unemployment edged up to 4.6%. In response, the Federal Reserve cut interest rates again in December. Inflation has eased towards 2.5%, and government spending offers modest support into early 2026. Consumer spending remains resilient but uneven. Higher-income households are driving growth, while those on lower incomes face mounting pressures. Labour markets are softening without collapsing, and further rate cuts cannot be ruled out.

Artificial intelligence continues to dominate headlines, though its real economic impact remains unclear. Investment is flowing into data centres and supporting infrastructure, but meaningful productivity gains have yet to materialise.

We maintain a slightly underweight stance on US equities, favouring opportunities elsewhere. Our exposure is diversified beyond the main index, with an emphasis on value-oriented and small- to mid-cap strategies – areas we believe offer better prospects at current valuations.

Europe

European equities finished December on a positive note, supported by inflation sitting close to the European Central Bank’s 2% target and a stable jobs market. Headline inflation hovered at about 2.2%, while unemployment held steady at 6.4% in the eurozone and 6.0% across the wider EU. These conditions helped sentiment even as manufacturing remained soft. The ECB left interest rates unchanged at its December meeting, signalling confidence that inflation will ease further in 2026.

December’s data revealed a clear split between services and industry. Manufacturing slipped back into contraction, with order books and employment under pressure – particularly in Germany. Services activity, by contrast, edged higher and helped markets look through the near-term industrial weakness. Consumer confidence dipped, but resilient employment and rising real incomes limited the impact. Equities ended the year firmer across much of the continent.

The economic picture is modestly encouraging. The ECB expects growth of about 1.2% in 2026, with inflation easing towards 1.9%. This suggests steady policy rather than fresh tightening, and most forecasters expect rates to remain broadly unchanged as inflation continues to fall.

Fiscal policy – government spending and taxation – is expected to be broadly neutral overall. However, targeted public investment should provide a modest boost. Germany’s multi-year infrastructure programme and increased defence spending across member states are likely to support demand and gradually improve competitiveness.

This backdrop typically favours quality cyclical and value-oriented sectors (i.e. financials, industrials, and select materials) over the more export-sensitive parts of manufacturing, which face external headwinds and lingering cost pressures. European equities look attractively valued compared with global peers, and earnings prospects are improving. Small- and mid-cap companies stand out as potential beneficiaries as domestic demand supports revenue growth.

Despite these tailwinds, we are acutely aware that risks remain. Weak external demand, high energy costs for industry, and cautious households keeping savings rates elevated could all slow any cyclical recovery if confidence fails to rebuild.

The eurozone ended 2025 with an improving market tone, underpinned by contained inflation, stable employment, and supportive, if measured, policy. In 2026, we expect steady growth, easing inflation, and neutral fiscal conditions to provide a constructive backdrop for European equities. We see opportunities in value, quality cyclicals, and small- to mid-cap names as earnings normalise and investment programmes take hold.

Rest of the world

It was a standout year for Asian and emerging market equities, though beneath the headline gains, regional fortunes diverged. Emerging markets delivered one of the strongest annual returns globally, rising about 24% in sterling terms, helped by a late-year rally in December. Asia excluding Japan posted similar strength, up nearly 23% for the year. China rebounded sharply with gains of about 22%, despite lingering concerns over its property sector. Japan’s TOPIX index also advanced roughly 25% in local currency though UK investors saw more muted returns as the pound strengthened significantly against the yen late in the year.

The drivers were clear: optimism around falling global inflation, a softer US dollar, and strong demand for technology hardware lifted sentiment across Asia. Korea and Taiwan led the way thanks to their pivotal role in supplying chips for artificial intelligence applications. Chinese equities had a mixed but slightly positive month as investors weighed policy support against weak consumer confidence. Japan’s market hovered near record highs, supported by corporate governance reforms and robust capital investment, though currency translation once again eroded returns for UK investors.

Currency dynamics played a significant role in 2025. While emerging markets and Asia excluding Japan saw little drag from foreign exchange movements, helped by a weaker US dollar, Japan told a different story. Sterling surged to about ¥211 per pound by year end, cutting returns on Japanese equities from roughly 25% in local terms to nearer 15% for UK investors.

This highlights why currency hedging (protecting against exchange rate swings) can be so important when investing internationally. In markets where policy shifts and interest rate differences drive sharp currency moves, unhedged exposure can meaningfully erode returns.

The outlook remains encouraging, though with important nuances by region. Emerging markets and Asia excluding Japan should benefit from attractive valuations, recovering earnings, and structural themes such as AI and semiconductor demand. China’s prospects hinge on credible policy execution and stabilisation in property and consumer spending. Japan offers solid fundamentals but faces ongoing currency risk; sterling strength could continue to dampen returns unless the yen stabilises as the Bank of Japan gradually tightens policy.

In our view, Asia and emerging markets enter 2026 with improving fundamentals and supportive conditions. However, wide dispersion across regions and currencies means that active positioning and hedging strategies will matter more than ever. We remain constructive on the asset class, but believe careful selection is essential.

Fixed income

Global bond markets ended 2025 in reassuring fashion, delivering steady gains across most segments. UK Government bonds delivered a modest gain of about 5% for the year, with December adding a small uplift as yields eased from their autumn highs. The 10-year gilt finished near 4.3%, reflecting persistent inflation and heavy Government borrowing that capped price gains. Expectations of Bank of England rate cuts supported sentiment, but fiscal concerns kept yields elevated.

Across the Atlantic, US Treasuries were among the strongest performers in local currency terms, returning roughly 5.8% for the year. December saw yields settle near 4.18% as the Federal Reserve cut rates by 0.75% and inflation cooled. For UK investors, however, a stronger pound trimmed returns slightly – a useful reminder that currency can be just as influential as the bonds themselves when investing globally.

Emerging market debt stood out as the clear winner of 2025. Hard-currency sovereign bonds – government debt issued in US dollars – gained over 11%, and sterling-based returns were broadly similar thanks to a weaker dollar late in the year. December added modest gains as emerging market currencies strengthened, and local central banks cut rates. For UK investors, this segment offered both attractive income and favourable currency tailwinds, a rare combination in a year of global uncertainty.

High-yield bonds (issued by companies with lower credit ratings but offering higher income) also delivered solid results, returning 8–10% globally. The gap between these bonds and safer government debt remained near historic lows, defaults were minimal, and the income these bonds generate drove performance throughout the year. Sterling strength shaved a little off returns, but the asset class still provided strong income and resilience.

Investment-grade bonds followed suit, posting 7–8% gains supported by falling Treasury yields and robust company finances. Currency movements meant UK investors saw slightly lower returns than the headline figures, but the segment continued to offer diversification and stability.

Three themes dominated fixed income in 2025. First, central banks began easing policy. The Federal Reserve cut rates, and expectations of Bank of England action lifted bond prices globally. Second, falling inflation supported government debt, particularly in the US and Europe. Third, strong corporate credit quality kept the premium investors demand for riskier bonds at historically low levels, underpinning returns across high-yield and investment-grade markets.

Looking ahead to 2026, returns are likely to be more modest. Gilts and Treasuries may see smaller gains as rate cuts slow, and government borrowing remains heavy. Emerging market debt still looks attractive, offering appealing income and improving fundamentals – though currency volatility could re-emerge. High-yield bonds are expected to deliver lower returns, as the premium for holding them has little room to fall further. Investment-grade bonds should continue to offer mid-single-digit returns, supported by steady income and strong credit quality.

Ask us anything

Q: Please share your outlook for 2026, what can we expect from markets next year?

As we look ahead to 2026, the global economy appears set to maintain its momentum. Our base case is that this could be a year of ‘extending the cycle’, where both government spending and interest rate policy work together to keep growth steady.

Several major economies are opening their wallets. Japan is preparing stimulus measures, while Germany has already announced its plans. Across the Atlantic, the US Congress has passed the “One Big Beautiful Bill”, which will begin boosting the American economy throughout the year. Meanwhile, China is expected to introduce gradual measures to support its economic targets.

Central banks will likely be taking different paths in 2026. Both the US and UK are likely to continue cutting interest rates, with the US potentially accelerating these cuts under a more dovish Federal Reserve chair appointed by President Trump. The eurozone looks set to keep rates steady unless something unexpected occurs. Japan stands apart, with rates edging upwards as the Bank of Japan grows confident that inflation is settling around its 2% target.

Growth forecasts remain solid across the board. Europe, particularly Germany, should see improved performance thanks to fiscal stimulus. China aims to maintain around 5% growth, while US expansion is expected to match this year’s pace. The UK’s outlook remains modest; similar to 2025 with some risk of minor deterioration.

Key themes and risks

• Tariffs remain in play, though their exact legal status awaits a US Supreme Court decision. Regardless of the outcome, we believe they will continue shaping trade in 2026, with global supply chains adapting accordingly.

• Valuations present a challenge. Both equity and bond markets look expensive, leaving little room for disappointment. The artificial intelligence theme dominates investor sentiment, but 2026 could test whether AI companies can deliver on sky-high expectations. We expect the focus to shift from AI hype towards actual monetisation and returns on the massive capital investments made in the technology.

• Politics officially looks quiet, but history suggests otherwise. November’s US midterm elections will determine how much President Trump can achieve in his final two years. In the UK, local elections could significantly impact Prime Minister Keir Starmer and Chancellor Rachel Reeves’s political futures.

We are heading into 2026 with cautious optimism. The fundamentals suggest a positive year for global growth, but investors should remember that markets have already priced in considerable good news. Success will depend on whether reality can meet these elevated expectations.

If there is a question you’d like to pose to our team, please reply to this email or write to [email protected].

Four key takeaways from December:

- UK and European equities rose, supported by a Bank of England rate cut and a Santa rally driven by rotation into value sectors like banks and energy.

- US equities fell for sterling investors, as technology enthusiasm cooled and dollar weakness amplified losses.

- Asia ex-Japan gained modestly, lifted by semiconductor demand and cyclical sector inflows, while yen weakness eroded Japan’s returns for UK investors.

- Fixed income added small gains, with gilts and Treasuries benefiting from falling inflation and rate cut expectations.

MARKET DATA

All performance figures are from FE analytics (as at 31/12/2025) and quoted on a total return basis in pounds sterling.

The Monthly Market Commentary (MMC) is written and researched by Scott Bradshaw, Lauren Hyslop and Jonathon Marchant for clients and professional connections of Mattioli Woods and is for information purposes only. It is not intended to be an invitation to buy, or to act upon the comments made, and all investment decisions should be taken with advice, given appropriate knowledge of the investorʼs circumstances. The value of investments and the income from them can fall as well as rise and investors may not get back the full amount invested. Past performance is not a guide to the future.

Mattioli Woods Limited is authorised and regulated by the Financial Conduct Authority.

Sources: All other sources quoted, if used directly, except fund managers who will be left anonymous; otherwise, this is the work of Mattioli Woods.