Global markets summary

May witnessed a resurgence in global equity markets, with investor confidence returning across most major indices. US equities posted their strongest monthly performance since the final quarter of 2023, as market participants were emboldened to increase risk exposure following President Donald Trump’s decision to moderate his stance on the most stringent proposed tariffs.

Market momentum accelerated in early May following the announcement of a bilateral trade agreement between the US and UK. A subsequent decision by Washington and Beijing to reduce tariffs for a minimum 90-day period provided additional impetus for Wall Street’s advance, even as US government bonds and the currency faced persistent headwinds.

UK equities benefited from growing confidence that trade frictions might abate more rapidly than previously anticipated. Continental European bourses similarly enjoyed positive returns, with the Euro STOXX index advancing 4.89% in sterling terms. European markets received additional support after President Trump indicated he would extend the timeline for negotiations with the EU before implementing proposed 50% tariffs. Decelerating inflation across several major eurozone economies further bolstered market expectations for European Central Bank (ECB) rate reductions.

The fixed income landscape presented a more nuanced picture. Higher yielding securities outpaced sovereign debt during the period, buoyed by equity market strength, constructive trade developments, and improving consumer sentiment. The asset class benefited from favourable technical dynamics, with healthy investor inflows and restrained new issuance. Investment grade corporate bonds similarly outperformed, with new offerings experiencing robust oversubscription.

Government bond yields in both the US and UK climbed throughout May, resulting in corresponding price declines. UK inflation accelerated beyond forecasts to reach 3.5%, marking its highest level in over a year. Treasury markets exhibited renewed nervousness amid progress on President Trump’s tax legislation through Washington’s legislative machinery. While concerns regarding the US fiscal position remain, the bill’s advancement has unsettled investors, pushing yields to multi-month highs. Should the legislation pass, it would reduce taxation without commensurate spending reductions, with analysts projecting an additional $3 trillion burden on the deficit over the coming decade.

As May ended, the US Court of International Trade delivered a ruling that President Trump lacked the legal authority to implement most of the global tariffs introduced since commencing his second administration. While equity markets maintained an optimistic interpretation of trade developments throughout the month, we will not be complacent amid these seemingly favourable conditions, positioning ourselves somewhat more cautiously than our peers by retaining elevated levels of cash.

May’s market performance reflected a notable shift in investor sentiment, with risk assets recovering strongly from April’s tariff-induced volatility. However, significant uncertainties remain, including the legal challenges to US trade policy, fiscal sustainability concerns, and the potential for renewed trade tensions. While markets have embraced a more optimistic outlook, investors should remain vigilant to the evolving policy landscape and its implications for asset prices.

United Kingdom

UK equities delivered another solid month of returns in May, with the MSCI United Kingdom All Cap returning +4.06%, though lagging the performance of broader global equities (MSCI ACWI +4.74%). Like most markets, domestic equities were supported by optimism that trade tensions may ease more quickly than initially feared.

The UK negotiated several significant trade agreements that helped bolster market sentiment during May. After years of negotiations, the UK secured a comprehensive trade deal with India towards the start of the month. The agreement reduces tariffs on UK imports of clothing, cars, food, and jewellery, while lowering barriers for UK exporters of alcohol, industrial goods, premium automobiles, and food products. While India represents a relatively modest portion of UK trade volumes, the deal signals positive momentum in the UK’s trade strategy.

Just two days later, a targeted trade agreement with the US delivered a fascinating insight into the transactional nature of President Trump’s regime. As a result, the UK automotive industry benefits from reduced tariffs, while the steel sector sees complete tariff elimination. In return, the UK removed its 20% tariff on US beef while maintaining domestic food standards. Though relatively narrow in scope, this agreement represents an important diplomatic victory for Keir Starmer.

The month concluded with another significant development on 19 May, when the UK and EU established a new post-Brexit framework spanning multiple sectors. The agreement grants EU fishing vessels continued access to UK waters through to 2038 in exchange for streamlined checks on UK food exports. The pact also includes enhanced defence and security cooperation with improved coordination and funding access.

These diplomatic successes coincided with supportive monetary policy developments. The Bank of England delivered a 25 basis point rate cut to 4.25%, providing relief for borrowers and supporting market sentiment. Markets currently anticipate further cuts to approximately 3.50% by year end, while the BoE now projects inflation at 1.75% by 2027, below the 2% target.

However, the path forward remains uncertain. Lower energy prices support the inflation outlook, particularly as OPEC+ agreed to increase output for the second consecutive month. Yet recent challenges include inflation reaching 3.5% (above market expectations) and the potential for a divided Monetary Policy Committee, where two of nine members opposed the May rate cut. The June decision appears finely balanced, with the combination of elevated inflation and improved trade conditions potentially encouraging a more cautious approach.

The UK has demonstrated remarkable adaptability in navigating an increasingly fragmented global trade environment. While the recent trade agreements may not dramatically impact GDP growth or corporate earnings in the near term, they contribute positively to market sentiment and provide a foundation for future expansion.

We maintain our positive stance on UK equities, viewing current valuations as attractive given the improving data and supportive monetary policy backdrop.

North America

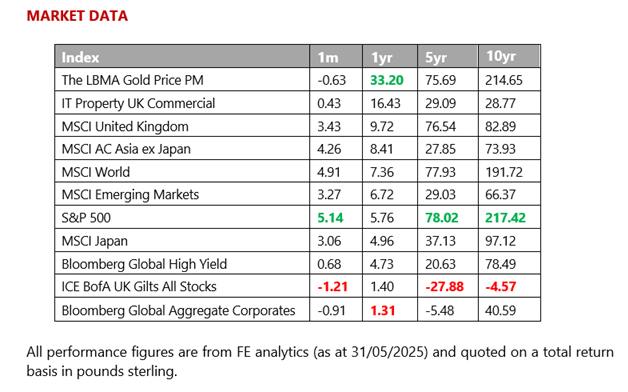

May marked a standout month for US equity markets, with the S&P 500 posting a robust 6.25% return in dollar terms (5.24% for sterling-based investors) – its strongest monthly performance since November 2023. This broad-based rally pushed the index into positive territory year-to-date in local currency terms. However, for UK investors, the S&P 500 remains down 6.30% in sterling terms, underscoring the significant impact of currency movements on international returns.

The rally was underpinned by solid corporate earnings. With 97% of S&P 500 companies having reported, blended year-on-year earnings growth reached 12.4%, marking a second consecutive quarter of double-digit expansion. Encouragingly, 77% of companies exceeded earnings expectations, while 63% beat revenue forecasts – highlighting the breadth of positive surprises.

Technology leaders within the ‘Magnificent Seven’ – notably Meta, Tesla, and NVIDIA – led the charge. NVIDIA’s 70% surge in quarterly revenue exemplified the sector’s strength. Meanwhile, financials and industrials approached record highs, buoyed by improved investor sentiment following the administration’s decision to pause its most aggressive tariff measures announced in early April.

Opinions remain divided on President Trump’s trade strategy – seen by some as calculated brinkmanship, by others as erratic policymaking. What is clear, however, is that tariff volatility has been a dominant force in shaping market performance this year. The 90-day pause on sweeping tariffs announced on 9 April marked a turning point, shifting sentiment from pessimism to cautious optimism. This cycle of threats, negotiations, and partial retreats has become a hallmark of the administration’s approach – so much so that market commentators have coined the acronym TACO (“Trump Always Chickens Out”) to describe the pattern.

Legal challenges have added further complexity. A US Court of International Trade ruling found that the President had “overreached his authority” by imposing tariffs without Congressional approval. Although the ruling was stayed pending appeal, it introduced a moment of constitutional tension. The administration’s swift appeal – and the higher court’s decision to allow tariffs to remain in place during the process – highlighted the enduring strength of executive power in trade matters.

What emerges is a more nuanced outlook. While the immediate risk of severe trade disruption has eased, a new baseline of elevated tariffs (likely stabilising around 12–14% of goods imports) appears increasingly entrenched. This suggests a structural shift in US trade policy, rather than a temporary negotiating tactic, and markets are gradually adjusting their expectations accordingly.

Nonetheless, uncertainties persist. The legal basis for many tariffs remains under scrutiny, and Section 899 of the proposed budget bill has raised concerns among market participants. If enacted, it could impose additional taxes on foreign investments in US assets, potentially dampening overseas demand for American securities.

We continue to recommend a balanced approach in American equities, combining growth and value shares, anticipating broader market participation beyond the concentrated AI-related names.

Europe

European markets demonstrated solid performance in May, with the MSCI Europe ex-UK Index advancing 4.9%. Progress in transatlantic trade negotiations helped allay recession concerns, while expectations of fiscal support and positive earnings revisions continued to bolster regional sentiment.

The rally was broad-based across the continent, with investors responding positively to the de-escalation of trade tensions. European indices recovered swiftly from earlier weakness, with Germany’s DAX achieving record closing highs during the month. The reduced threat of severe US tariffs – particularly the withdrawal of the proposed 50% levy on EU imports – contributed significantly to improved market confidence.

Looking ahead, European policymakers remain committed to enhancing defence capabilities and strengthening supply chains, themes that should benefit equity investors. However, the inflation outlook remains uncertain, with potential retaliatory tariffs on US imports balanced against deflationary pressures from increased Chinese exports seeking alternative markets.

We maintain a neutral stance. Reasonable valuations and the ECB’s comparatively accommodating monetary policy provide underlying support.

Rest of the world

Japanese equities participated in May’s global risk rally, with the TOPIX delivering 2.90% in £ terms. The market operated against a backdrop of heightened volatility in the domestic bond market, where long-dated government securities came under sustained pressure. A lack of domestic demand for longer-duration bonds, combined with investor concerns over the Ministry of Finance’s issuance strategy, contributed to challenging conditions.

Some relief came following the authorities’ announcement to scale back long-dated bond issuance, which helped stabilise financial conditions. Our position on Japanese equities remains neutral. The economy is sluggish, and alongside global concerns, faces American trade protection risks. Government uncertainty leaves investors without clear policy direction.

The MSCI Asia Pacific (ex Japan) index returned 4.10% over May. The region, however, continues to face a mix of opportunities and headwinds as global trade flows adjusted to the evolving tariff landscape. India emerged as a notable potential beneficiary. Apple’s announcement to relocate iPhone production for the US market to Indian facilities by the end of 2026 reflects broader supply chain realignments. However, India also faces ongoing trade negotiations with the US, aiming to avert a proposed 26% tariff on its exports – highlighting the delicate balance between opportunity and risk in the current environment.

Emerging market equities contended with a complex backdrop in May, shaped by shifting trade dynamics and currency pressures. The potential redirection of Chinese exports to alternative markets, as US tariffs constrained traditional trade routes, introduced both risks and opportunities across the emerging market landscape.

Fixed income

Bond markets experienced heightened volatility in May, navigating between competing concerns over persistent inflation, growth uncertainties, and mounting fiscal challenges. A pivotal moment came with the downgrade of US sovereign credit, which triggered a sell-off in longer-dated Treasuries and prompted reassessment of government borrowing sustainability.

Sovereign yields rose across developed markets, though performance diverged significantly based on fiscal positions. Countries with weaker fiscal profiles (including the US, UK, and Japan) underperformed, while peripheral European markets such as Spain and Italy proved more defensive, benefiting from their improved fiscal standings.

We maintain a cautious stance on US government debt. Market concerns persist regarding Treasury yields potentially rising, particularly absent any concrete fiscal planning. The 2017 tax reductions will probably continue, while meaningful budget reductions appear unlikely, creating yield pressures. Looking forward, the combination of persistent inflation around 3.0-3.5% in the US, coupled with substantial fiscal deficits projected at 7% of GDP, suggests limited scope for monetary easing in the near term. Long-dated yields may face continued upward pressure as governments grapple with financing growing debt burdens amid potentially reduced foreign demand.

Credit markets painted a more optimistic picture over May, with high-yield bonds outperforming both investment grade and sovereign debt. US high-yield spreads compressed by 130 basis points from April’s wides, reflecting renewed risk appetite and confidence that worst-case growth scenarios would be avoided.

Ask us anything

Q: Can you explain the downgrade to US debt? Is there any impact on portfolios?

A: Moody’s recent downgrade of US sovereign debt from Aaa to Aa1 marks a symbolic watershed moment, leaving America without a top-tier rating from any major agency. The timing could hardly be more challenging, coinciding with congressional approval of President Trump’s “One Big Beautiful Bill” – a tax package that could add over $3 trillion to the national debt over the next decade. With the US already running a 6.8% budget deficit (a level typically associated with recessions) and annual interest payments approaching $1 trillion, the downgrade serves as a stark reminder that America’s “exorbitant privilege” in global debt markets should not be taken for granted.

The immediate market reaction has been telling. Thirty-year Treasury yields surged to 5.04%, their highest level since November 2023, while the dollar weakened against major currencies. These movements reflect growing bondholder concerns about debt sustainability, particularly as the new tax cuts lack offsetting spending reductions. The spectre of the UK’s 2022 gilt crisis looms large, raising questions about whether bond markets will continue to tolerate America’s fiscal trajectory or deliver a sharp rebuke through persistently higher yields.

For portfolios, the practical impact remains measured despite the headlines. Global banking regulations do not differentiate between bonds within the “Grade A” category, meaning banks face no forced selling pressure. Central bank reserve managers, who prioritise deep and liquid markets, are unlikely to alter their Treasury holdings significantly. That said, the downgrade has already prompted Moody’s to reduce counterparty risk ratings for major US banks, including JPMorgan Chase, Bank of America, and Wells Fargo.

Looking ahead, we maintain minimal exposure to US government debt within portfolios, and where positions exist, we’ve intentionally kept duration short to limit sensitivity to interest rate movements. While Treasuries retain their role as the world’s deepest and most liquid asset class, the combination of expanding deficits, persistent inflation concerns, and erratic policymaking from Washington suggests that US Treasury yields will likely remain elevated. The era of ultra-low borrowing costs appears firmly behind us, and investors would be wise to position accordingly.

Key takeaways

- Moody’s lowered US debt from Aaa to Aa1, leaving America without a top-tier rating from any major agency for the first time, coinciding with Trump’s tax package that could add $3 trillion to national debt.

- 30-year Treasury yields surged to 5.04% (highest since November 2023) and the dollar weakened, reflecting concerns about debt sustainability with the US running a 6.8% deficit and approaching $1 trillion in annual interest payments.

- We maintain minimal exposure to US government debt with intentionally short duration where held, expecting yields to remain elevated given fiscal challenges and inflation concerns.

If there is a question you’d like to pose to our team, please reply to this email or write to [email protected].

The Monthly Market Commentary (MMC) is written and researched by Scott Bradshaw, Lauren Hyslop and Jonathon Marchant for clients and professional connections of Mattioli Woods and is for information purposes only. It is not intended to be an invitation to buy, or to act upon the comments made, and all investment decisions should be taken with advice, given appropriate knowledge of the investorʼs circumstances. The value of investments and the income from them can fall as well as rise and investors may not get back the full amount invested. Past performance is not a guide to the future.

Mattioli Woods Limited is authorised and regulated by the Financial Conduct Authority.

Sources: All other sources quoted if used directly, except fund managers who will be left anonymous; otherwise, this is the work of Mattioli Woods.