Global markets summary

Global markets delivered a broadly positive performance in February, with a notable shift in regional leadership. International equities outperformed the United States, extending a trend that has gathered momentum since the start of the year and represents a meaningful departure from the US dominance of the past decade.

Japan remained the standout major market, supported by moderate inflation, wage growth, corporate governance reform, and political stability. Closer to home, UK equities benefited from stabilising domestic inflation, improving corporate earnings, and renewed investor appetite for value-oriented markets, as investors globally rotated away from large-capitalisation growth stocks. Across Asia Pacific, performance was more varied: early gains in Korea and parts of emerging Asia, driven by renewed semiconductor demand, gave way to a more cautious mood as expectations for artificial intelligence growth were reassessed.

In the US, February was defined by heightened debate surrounding artificial intelligence. The emergence of capable new artificial intelligence (AI) products prompted investors to question the long-term position of established software businesses, and the resulting wave of selling extended well beyond directly affected companies, creating notable market volatility.

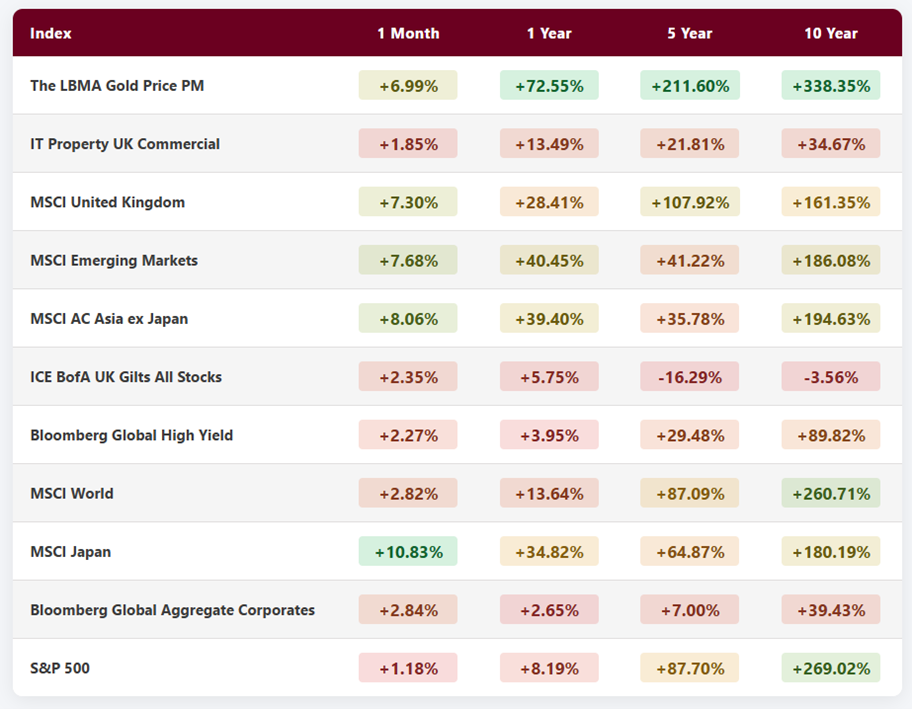

Fixed income markets were mixed. US Treasuries made modest gains on the back of Federal Reserve rate cut expectations, while UK gilts edged slightly lower. Investment grade credit was broadly stable, and physical gold continued its remarkable run, finishing the month up 21.2% year to date.

As the month drew to a close, events took a more serious turn. Over the weekend of 28 February, coordinated US and Israeli military strikes on Iran sent immediate shockwaves through financial markets. The Strait of Hormuz, a narrow waterway through which approximately one fifth of the world’s daily oil supply passes, moved sharply to the centre of investor concern. Geopolitical risk is now firmly in focus as we enter March. We address this development in detail in the “Ask us anything” section below.

United Kingdom

UK equities delivered strong outperformance relative to global peers during February, supported by an encouraging set of economic data, though the picture was not without nuance. Perhaps the most striking release was January’s public finances, which showed a budget surplus of £30.4 billion: the largest monthly surplus since records began in 1993, and more than double the figure recorded in the same month a year earlier. Cumulative borrowing across the first ten months of the fiscal year also came in well below official forecasts, providing the Chancellor with some welcome breathing room ahead of the Spring Statement.

Inflation continued to ease, with the Consumer Prices Index falling to 3.0% in January, down from 3.4% the month before and in line with expectations. While still above the Bank of England’s 2% target, the direction of travel is encouraging. The latest labour market data reinforced this picture: wage growth softened to 4.2%, below both the previous reading and market expectations, while private sector pay growth moderated to 3.4%. Unemployment edged up slightly to 5.2%. Taken together, the data was broadly supportive of a further interest rate cut at the Bank of England’s March meeting, and gilt yields fell in response.

Business activity remained resilient. The UK Composite Purchasing Managers’ Index for February came in at 53.9, comfortably above the 50 level that separates expansion from contraction, with both services and manufacturing contributing positively. Retail sales also surprised on the upside, rising 2.0% excluding fuel against a market expectation of just 0.3%, and British Retail Consortium data confirmed that non-food retail sales turned positive for the first time in several months, with clothing returning to growth.

The housing market showed signs of stability. Both Nationwide and Halifax reported modest monthly price gains in January, with the average UK house price surpassing £300,000 for the first time, supported by transaction volumes running slightly above pre-pandemic levels.

A more cautious note came from confidence surveys. The GfK Consumer Confidence reading fell to minus 19, weaker than expected, suggesting households remain watchful despite the improving economic backdrop. GDP growth for the final quarter of 2025 also came in slightly below expectations at 0.1%, though monthly data pointed to a pickup towards the year end following the Autumn Budget.

Overall, the data paints a picture of an economy gradually finding its footing, with conditions increasingly supportive of monetary easing in the months ahead. The extent to which easing occurs is now somewhat dependent on events in the Middle East. Persistently higher energy prices are likely to lead to higher inflation, and this is likely to take March’s anticipated interest rate cut off the table. The UK remains particularly vulnerable to higher prices and imports, given the Government’s lack of willingness to tap domestic reserves and the focus on net zero. Energy costs in the UK remain among the highest in the world and this is a persistent headwind for consumers and businesses.

North America

US equity markets delivered mixed results in February 2026, with the headline figures concealing considerable movement beneath the surface. In local currency terms, the S&P 500 ended the month marginally lower, while the more technology-focused Nasdaq 100 recorded its weakest monthly performance since early 2025, dragged down by large technology companies and artificial intelligence-linked businesses. For sterling-based investors, the picture was somewhat more encouraging, as a 1.5% decline in the pound against the dollar softened the impact of those losses when translated back into sterling. Even so, US equities continued to trail many other international markets.

The defining theme of the month was a meaningful shift in market leadership. Investors rotated away from the high-growth technology stocks that had dominated 2025 and towards companies offering steadier income streams and more tangible assets. Utilities and energy were standout performers, supported by rising oil prices and a preference for resilience in an uncertain environment, while software and artificial intelligence-related shares declined sharply as questions mounted over the long-term sustainability of AI investment. Value-oriented strategies, mid-sized companies and equally-weighted approaches to the S&P 500 all outperformed, with the equal-weight index delivering one of its strongest monthly results in almost a year. A market generating returns across a wider range of businesses, rather than a handful of technology giants, is generally considered a healthier and more durable structure.

Geopolitical tensions escalated sharply in the final days of February following coordinated US and Israeli strikes on Iran. Oil prices rose, gold strengthened, and equity markets came under pressure, though investors showed pockets of resilience as they weighed the likelihood of a short-lived disruption against a more structural shift. Looking ahead, the three factors most likely to shape returns are the broadening of market leadership, the path of inflation and interest rates, and the evolution of geopolitical risk. For sterling-based investors, the US dollar will remain an important variable: it tends to strengthen in periods of uncertainty, which can enhance translated returns but also raises hedging costs.

Within this context, Mattioli Woods portfolios are deliberately positioned with less exposure to US equities than the global benchmark, reflecting our view that valuations in parts of the market have moved ahead of underlying fundamentals. Within our US allocation, we have moved away from passive index exposure in favour of a broader approach, including dedicated positions in value-oriented strategies and smaller companies. This positioning has contributed positively to relative performance, and we believe it leaves portfolios well placed should the broadening of market leadership continue.

Europe

During February, European equities delivered a notably stronger performance than their US counterparts, supported by encouraging economic data and a shift in investor preference towards sectors less exposed to the turbulence in global technology shares. While US indices ended the month broadly lower, European markets rose by approximately 3%, reflecting growing investor confidence and resilient company earnings.

This advance extended a trend that took hold in late 2025, as the drivers of market performance broadened beyond the world’s largest technology companies and into more traditional, economically-sensitive industries such as manufacturing, banking, and healthcare. In the United States, by contrast, software companies, large-scale cloud providers, and businesses closely tied to artificial intelligence weighed heavily on overall returns.

European markets were well positioned for this shift. Unlike the United States, where technology dominates, European stock markets have far greater exposure to financials (22%), industrials (21.6%), healthcare (13%), and technology (10%). These are sectors with physical assets, predictable revenues, and less reliance on the kind of ambitious growth assumptions that propelled technology valuations higher in recent years. As confidence in those assumptions began to waver, investors moved capital accordingly, and Europe was a natural beneficiary.

The region faces a meaningful test as tensions in the Middle East escalate. Effective disruption to shipping through the Strait of Hormuz, one of the world’s most critical routes for oil, has sent tanker traffic down by more than 80% and pushed the Brent crude oil price up by between 7% and 9%, to approximately $78 to $80 per barrel. For a region that relies heavily on energy imports, the risks are twofold: higher energy costs bear directly on industrial profit margins, particularly in the manufacturing-heavy sectors that drove European outperformance in February, and any sustained rise in prices risks reigniting inflation at a moment when central banks have only recently begun to ease. Markets are currently behaving as though the disruption will prove short-lived, though history offers little reassurance on that point.

Geopolitical crises are, by their nature, unpredictable. Investors in European equities would be wise to treat the current relative calm not as a signal that risks have passed, but as an opportunity to consider carefully how much uncertainty their portfolios can comfortably absorb.

Rest of the world

February was an encouraging month for global stock markets beyond the United States, with Japan, Asia Pacific, and emerging markets all outperforming. Investors moved capital away from the dominant American technology companies that had led markets for much of the past two years, broadening returns for those with international exposure. For UK investors, a 1.5% fall in sterling against the US dollar provided an additional tailwind when returns were translated back into pounds.

Japanese equities were among the strongest performers globally, with a number of leading strategies returning between 15% and 20% over the month. Confidence grew in the government’s plans to stimulate economic growth, and companies linked to semiconductors and artificial intelligence performed particularly well. Strategies focused on value and smaller companies also did especially well, as investors judged Japanese shares to be more attractively priced than their American counterparts.

Across the wider Asia Pacific region, South Korea and Taiwan led the way. Both countries are home to some of the world’s most important semiconductor and memory chip manufacturers, and demand for these components continued to rise sharply as businesses globally invested heavily in artificial intelligence infrastructure. Emerging markets built on recent gains through the same theme, with improving corporate earnings forecasts and a growing number of investors looking beyond the United States for opportunities.

Towards the end of the month, an escalation in tensions between the United States, Israel and Iran introduced a degree of nervousness. The closure of the Strait of Hormuz pushed the price of Brent crude oil up by between 7% and 9%, to approximately $78 to $80 per barrel. The impact on Asian and emerging markets was relatively contained, though energy-importing economies such as Japan, South Korea and Taiwan experienced some short-lived volatility. Markets appeared to treat the disruption as a temporary event rather than the beginning of a prolonged crisis.

Looking ahead, the investment case for all three regions remains encouraging. Corporate earnings are improving, valuations are more attractive relative to the United States, and a softening US dollar provides a helpful backdrop. Short-term volatility may persist if oil prices remain elevated or tensions intensify, but the broader outlook remains positive as global growth becomes more evenly spread.

Fixed income

February was a broadly positive month for higher-quality bonds. Government bond yields fell across major developed markets, meaning bond prices rose, and assets such as US Treasuries, UK gilts, and global investment-grade corporate bonds all delivered positive returns. A calmer inflation backdrop and periodic bouts of market anxiety around trade policy and geopolitics encouraged investors to seek the relative safety of high-quality fixed income. For UK investors, a 1.5% fall in sterling against the US dollar provided a modest additional boost to overseas bond returns when translated back into pounds.

Within credit markets, investment-grade bonds benefited from both lower government yields and a preference among investors for financially stronger companies during a more uncertain period for equities. High-yield bonds lagged, however, as markets demanded greater compensation for taking on additional risk. Emerging market debt had a mixed month: falling global yields provided some support, but a stronger US dollar and rising geopolitical tensions acted as headwinds.

The mood shifted sharply at the end of February and into early March, when a significant escalation in the Middle East unsettled financial markets. The initial response was a flight to the safety of government bonds, which pushed yields lower. That rally proved short-lived. As investors began to consider the potential consequences of a prolonged conflict and the possibility of sustained higher oil prices, inflation concerns resurfaced and bond yields reversed course. Sovereign bonds across the United States, the United Kingdom, Japan, and elsewhere fell in price as a result, and markets began to question whether central banks would be able to proceed with the interest rate cuts many had anticipated for later in the year. High-yield and emerging market bonds felt the pressure most acutely.

Looking ahead, much depends on how events in the Middle East develop. A swift resolution could allow oil prices to settle and inflation expectations to moderate, restoring the more supportive environment that characterised much of February. A prolonged conflict, however, could keep oil prices elevated and delay the interest rate reductions that bond markets have been anticipating. The three factors most worth watching are the oil price, the guidance from major central banks as they weigh inflation risks against softer economic data, and the direction of the US dollar, which has a particularly significant bearing on emerging market debt. February served as a useful reminder of the stabilising role that high-quality bonds can play within a portfolio, while early March demonstrated how swiftly geopolitical events can reshape the investment outlook.

Ask us anything

Q: What are your views on the recent escalation of conflict in the Middle East? How are portfolios likely to cope with it?

A: We have received many variations of this question over the past few days, which is entirely understandable. Below, we set out what has happened, what it means for your investments, and how we are responding.

At the centre of this situation is the Strait of Hormuz, a narrow waterway in the Persian Gulf through which approximately one fifth of the world’s daily oil supply passes. In the wake of the strikes, a number of shipping companies have paused or rerouted their vessels, and insurers have substantially increased the cost of cover for ships travelling through the region, with some declining to offer cover for certain vessels at all. Even without the strait being formally closed, this has created a meaningful bottleneck. When oil becomes harder to move, it becomes more expensive, and that cost is ultimately passed through the supply chain to businesses and consumers.

How markets have responded

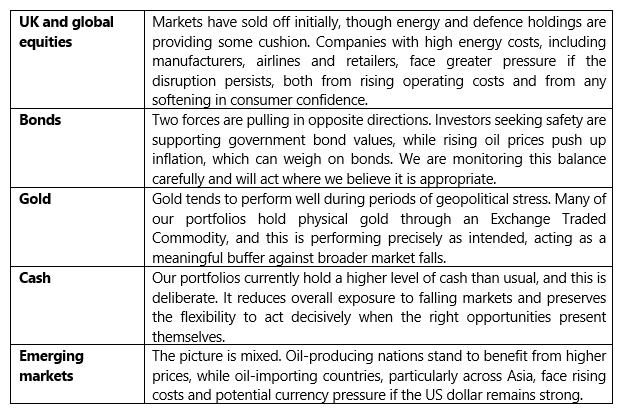

As at time of writing, market reactions so far have been broadly consistent with previous episodes of geopolitical tension. Oil and energy prices have risen sharply as investors price in the risk of reduced supply. Gold has risen as investors seek assets that tend to hold their value in periods of uncertainty. The US dollar has strengthened for similar reasons, and equity markets have fallen broadly, with energy and defence companies notable exceptions. The cost of borrowing for companies, particularly those with weaker balance sheets, has also increased as investors exercise greater caution.

Moves of this kind, while unsettling, are not unusual when significant geopolitical events occur. Markets have navigated many such episodes in the past, and we are monitoring the situation closely.

What this means for your investments

The scenarios we are considering

At this stage, three broad paths lie ahead. Our portfolios are positioned to navigate each scenario.

Scenario One

A quick de-escalation

Shipping and insurance through the Strait of Hormuz resume, the oil price spike fades, and markets recover much of the initial fall. This remains a realistic and credible possibility.

Scenario Two: Most Likely

Prolonged disruption

Shipping and insurance remain restricted for several weeks, keeping energy prices elevated and markets under pressure. Energy and defence holdings continue to provide some offset. This is the scenario we consider most likely over the coming week.

Scenario Three

A wider escalation

A broader regional conflict develops, pushing oil prices significantly higher and triggering a more sustained market sell-off. In this scenario, our gold holdings and elevated cash position become especially important as stabilising forces within portfolios.

What we are doing

We have acted swiftly and decisively. On Monday, we reduced overall equity exposure by 2% across our funds, reallocating the proceeds into cash, where we were already overweight. This is a tactical asset allocation decision, meaning it reflects our view on the broader market environment rather than any change in our conviction about the underlying investments held within portfolios.

The reduction was funded equally from US equities and European equities. Within Europe, we have shifted our emphasis away from mid-sized companies, which are structurally more sensitive to energy price shocks, and towards larger businesses: those with exposure to energy production that benefits from higher oil and gas prices, and large defensive companies with stable, predictable cash flows.

Over the past 12 months, we have deliberately avoided making reactive changes in response to geopolitical events, taking the view that short-term uncertainty rarely justifies disrupting a well-constructed portfolio. We believe this situation is different in both character and scale and warrants a measured response. The key considerations driving our thinking are as follows.

Oil prices and inflation are directly linked. Any prolonged disruption to energy flows through the Strait of Hormuz could push oil prices significantly higher, and leading economists estimate that this could add materially to global inflation. Higher inflation reduces the likelihood of the interest rate cuts that markets have been anticipating, which would affect both bond markets and broader economic confidence. At the same time, sustained rises in energy costs historically weigh on economic growth, and the situation is further complicated by China’s significant economic ties to Iran, the consequences of which extend well beyond the immediate region.

These pressures come at a moment when equity valuations were already elevated and markets were beginning to reassess some of the more optimistic assumptions around artificial intelligence and productivity growth. We consider it prudent to reduce risk at the margin.

As noted above, our portfolios were already defensively positioned before these changes, with an overweight to cash and meaningful exposure to gold. The additional equity reduction reinforces that positioning and provides further resilience should market conditions deteriorate.

We are monitoring whether shipping and insurance activity through the Strait of Hormuz begins to normalise and watching the oil price for signals as to whether this represents a short-term shock or something more persistent. If tensions ease and markets stabilise, we would look to unwind these tactical positions. Our central view, however, is that this situation is unlikely to be resolved quickly, and we believe the current positioning reflects an appropriate and proportionate response to that uncertainty.

We will continue to keep you informed as the situation develops. In the meantime, please do not hesitate to contact us if you have any questions or would like to discuss your portfolio in more detail.

If there is a question you’d like to pose to our team, please reply to this email or write to [email protected].

Four key takeaways from February 2026:

- International equity markets outperformed the United States in February, with Japan, Europe, and Asia Pacific leading the way as investors moved away from large-capitalisation technology stocks and towards value-oriented and economically-sensitive sectors.

- UK economic data was broadly encouraging, with a record monthly budget surplus, easing inflation, and resilient business activity all pointing towards further interest rate reductions in the months ahead.

- Physical gold finished February up 21.2% year to date and continued to perform precisely as intended within portfolios, providing a meaningful cushion against broader market volatility and geopolitical uncertainty.

- Coordinated US and Israeli military strikes on Iran at the end of February escalated geopolitical risk sharply, with potential implications for oil prices, inflation expectations, and the path of interest rates across major economies.

MARKET DATA

All performance figures are from FE analytics (as at 28/02/2026) and quoted on a total return basis in pounds sterling.

The Monthly Market Commentary (MMC) is written and researched by Scott Bradshaw, Lauren Hyslop and Jonathon Marchant for clients and professional connections of Mattioli Woods and is for information purposes only. It is not intended to be an invitation to buy, or to act upon the comments made, and all investment decisions should be taken with advice, given appropriate knowledge of the investorʼs circumstances. The value of investments and the income from them can fall as well as rise and investors may not get back the full amount invested. Past performance is not a guide to the future.

Mattioli Woods Limited is authorised and regulated by the Financial Conduct Authority.

Sources: All other sources quoted, if used directly, except fund managers who will be left anonymous; otherwise, this is the work of Mattioli Woods.