Global markets summary

Over the month of April, the stock market showed resilience, recovering a significant portion of its earlier losses. This recovery was largely driven by optimism around de-escalating trade tensions. US President Donald Trump introduced a 90-day suspension on the implementation of reciprocal tariffs for nations that had not yet imposed retaliatory measures, while tariffs on various electronic products were lifted. By the end of the month, developed market equities had risen by 0.9%, although US markets lagged their global counterparts. Growth stocks outperformed value stocks, with the energy sector’s underperformance notably impacting the value index.

In fixed income, the US bond market saw significant volatility in April, with Treasury yields spiking due to structural and cyclical factors. March inflation rates fell below expectations at 2.4% for headline and 2.8% for core, yet markets anticipate four rate cuts by year end despite potential inflation acceleration. UK Government bond yields were also volatile but ended April lower. A decline in March inflation and weaker activity data suggest a Bank of England rate cut in May. Within the corporate space, high-quality credit markets remain relatively resilient against recession risks, likely due to the substantial debt level improvements many companies have achieved in recent years.

April’s market rebound was striking, leaving some to wonder what the fuss was about. Despite this recovery, we remain cautious. The rally appears driven by optimism that the worst of the tariff impacts is over, though this is not yet reflected in the data. Confidence in US assets has been shaken, with the dollar and US Treasuries failing to act as safe havens temporarily. While they haven’t entirely lost this status, trust is dented, and global growth is likely to suffer.

As we face ongoing policy uncertainty and a potential macroeconomic storm, May will be pivotal for markets and could set the tone for the rest of the year.

United Kingdom

UK equities demonstrated resilience in April, closing with only a marginal decline (MSCI United Kingdom All Cap -0.22%). However, this seemingly calm monthly figure masks significant intra-month volatility. Following President Trump’s sweeping tariff announcement, the UK market experienced a sharp fall of 10%. What began as market shock, quickly transformed into measured adaptation, with equities recovering most losses by month end.

The UK has emerged in a relatively advantageous position within the new global tariff landscape, facing only the baseline 10% tariff rate. This positions the UK more favourably than several other developed economies, particularly Europe and Japan, which face steeper tariff barriers. The balanced trade relationship between the UK and US likely contributed to this more moderate approach, and ongoing diplomatic negotiations may yield further improvements.

The implementation of global tariffs is creating several unexpected disinflationary forces for the UK economy. The combination of anticipated slower global growth and OPEC’s production increase has driven energy prices lower, a significant positive for both consumers and businesses. Additionally, as Chinese exports originally destined for US markets get redirected to the UK and Europe, domestic consumers may benefit from increased supply and competitive pricing. While supply chain restructuring could prove inflationary over the medium term, near-term indicators suggest a more dovish interest rate environment than previously anticipated. This could substantially boost consumer spending power and support domestic equity valuations.

After years of investor neglect, the UK market appears to be of greater interest to global asset allocators. The changing global landscape (characterized by questions around ‘US exceptionalism’), the UK’s more moderate tariff exposure, restored political stability and attractive valuations create a compelling investment case. This view is supported by emerging performance trends, with UK equities outperforming the global benchmark every month so far in 2025.

We maintain our conviction in UK equities and our UK Dynamic Fund remains overweight to mid-cap companies. This segment offers several advantages in the current environment. Their strong domestic focus insulates these businesses from tariff impacts and limits exposure to US dollar weakness. This is combined with attractive valuations and greater potential to benefit from improving UK consumer sentiment and spending. As global markets navigate this period of adjustment, we believe the UK may offer a safe harbour among equity markets.

North America

In April 2025, President Trump’s tariff policy sparked US equity market turbulence, which reverberated across the globe. On 2 April, “Liberation Day” was declared, which involved new tariffs on imports. These tariffs were a two-tiered structure: a 10% baseline tariff on all imports and then additional, country-specific tariffs, some as high as 49%. The announcement plunged global financial markets into the steepest rout since the spread of the Covid pandemic five years ago. Investor consternation was assuaged mid-month as President Trump announced a 90-day pause on reciprocal tariffs for all countries except China, which faces a 145% tariff increase (however, short-term exemptions for electronics are in place).

Although headlines boast a “recovery” in the US stock market, it is key to understand the impact of currency on returns. For sterling-based investors, the index delivered -4.05% over April due to US dollar weakness against the pound. The dollar remains almost 4% below its “Liberation Day” level.

Despite the market volatility, certain aspects remained consistent throughout the month, particularly with the release of Q1 earnings. Nearly 40% of the S&P 500’s market cap reported Q1 results, including four of the ‘Magnificent Seven’. Despite limited forward guidance visibility due to trade policy uncertainty, sentiment remained positive, for now, as investors bet on businesses weathering economic slowdowns and tariff disruptions. We maintain a more cautious forward-looking stance given that US data in April showed economic moderation. The flash composite PMI fell to 51.2, driven by a decline in the services sector (51.4), while the manufacturing index rose slightly to 50.7. Business expectations and the Michigan Consumer Sentiment Index fell to pandemic levels, with confidence shocks hindering investment and spending, increasing recession risks by year end.

The economic impact of tariffs is akin to a tax on consumers and businesses. The Tax Foundation notes this as the largest tax increase since the early 1990s, likely hindering growth by reducing consumer real incomes. The current ‘tax hike’ is estimated at 0.6% of GDP, consistent with slow growth but not a deep recession.

We maintain a degree of scepticism around the market’s speedy recovery; President Trump’s tariff policies could be stagflationary for the US. Efforts to reduce deficits and retreat from globalisation may undermine US asset outperformance foundations. Consequently, we reduced US growth exposure in portfolios, favouring actively managed value exposure. Although painful in April, we believe this approach is prudent as the market digests these policies and their data impacts.

Europe

Despite sharing in the broader international market turbulence during April, European equities demonstrated resilience, with the Euro STOXX 50 index delivering a 2.13% return in sterling terms by month end. As investors seek alternatives to unstable US markets, European shares have emerged as a preferred destination, buoyed by more attractive valuations.

The eurozone’s economic landscape presented mixed signals. The flash composite PMI edged down to 50.1 in April, primarily due to services sector weakness (49.7), while manufacturing held relatively steady at 48.7. This manufacturing stability proved remarkable given the US implementation of a 10% tariff regime (rising to 25% on automobiles) early in the month. Lower energy costs and anticipated fiscal stimulus measures helped counterbalance trade-related challenges. However, declining consumer confidence indicators reflect ongoing concerns about trade tensions and the unresolved Ukrainian conflict.

First-quarter economic performance exceeded expectations, with eurozone growth accelerating to 0.4%, doubling the previous quarter’s 0.2% and surpassing analyst projections. Spain and Italy outperformed forecasts with growth of 0.6% and 0.3% respectively, while Germany and France returned to positive territory with modest gains. Ireland registered a substantial 3.2% increase, though this figure is typically influenced by multinational corporate activity.

Inflation remains a concern, with headline eurozone inflation holding at 2.2% in April – higher than economist forecasts. Core inflation, excluding volatile food and energy components, increased to 2.7% from 2.4%. Forward-looking indicators suggest potential challenges, as the European Commission’s economic confidence measure fell to 93.6 in April, its lowest reading since December. The consumer sentiment indicator remained negative at -16.7, reflecting increasing pessimism about economic prospects and reduced appetite for major purchases.

Given this complex backdrop, we maintain a neutral position on European equities. Within our core portfolios, we access this market through actively-managed funds strategically positioned to navigate current volatility while capitalising on emerging opportunities.

Rest of the world

Japanese equities emerged as relative outperformers in April, recovering from earlier sharp declines despite delivering a -1.65% return in sterling terms. The Japanese economy showed signs of resilience, with the all-industry flash PMI climbing to 51.1, bolstered by partial recovery in the services sector. Manufacturing activity, however, remained below the expansion threshold, underscoring vulnerability to anticipated US tariff impacts on export-focused Japanese firms. We continue to hold a neutral position on Japanese markets.

Emerging markets demonstrated unexpected stability amid escalating US-China tensions. Notable resilience was evident in Latin American markets, with Mexico and Brazil outperforming peers, benefiting from comparatively moderate US tariff policies. China, by contrast, bore the brunt of trade pressures, with MSCI China declining 7.49% in sterling terms for April, while the broader MSCI Asia Pacific ex Japan index limited losses to 1.83%.

The month witnessed dramatic developments in US-China trade relations, with American tariffs on Chinese imports surging to an unprecedented 145%, prompting reciprocal measures from Beijing. Market sentiment improved in the latter half of April as Washington signalled willingness to negotiate, coinciding with China’s robust first-quarter GDP growth of 5.4% year over year, which helped stabilise certain Chinese equities.

Economic indicators revealed the immediate impact of heightened trade barriers, with China’s manufacturing PMI contracting more severely than anticipated, falling to 49 from March’s 50.5 – representing the steepest decline since December 2023. The non-manufacturing index similarly disappointed, easing to 50.4 from the previous month’s three-month peak of 50.8.

China’s official growth target of approximately 5% for the current year appears increasingly challenging in the face of trade hostilities. While US trade friction threatens to disrupt Chinese exports and economic confidence, Beijing maintains substantial financial capacity to mitigate adverse effects through phased fiscal stimulus measures as it evaluates the economic implications of tariff policies.

Though temporarily spared from direct reciprocal tariffs, other Asian markets face indirect pressure due to their dependence on Chinese imports. This creates additional vulnerabilities for export-oriented economies like South Korea and Taiwan, which are already navigating fragile manufacturing conditions.

Our core portfolios maintain appropriately-sized exposure to broad emerging market equities, calibrated to risk tolerance levels. We preserve our neutral stance towards the region, recognising that while headwinds exist, geographical diversification across equity markets can help buffer against risks emanating from US policy decisions.

Fixed income

Fixed income performance presented a mixed picture in April amid persistent interest rate volatility as market participants evaluated potential inflation and growth implications of evolving foreign policy decisions.

UK Government bonds experienced significant yield fluctuations throughout April but ultimately closed lower, delivering robust returns with the IA (Investment Association) UK gilts sector advancing 1.58%. March’s encouraging inflation decline, combined with softening economic indicators, suggests favourable conditions for a Bank of England rate reduction in May. While UK gilt valuations appear attractive and the Government has maintained fiscal discipline thus far, global trade tensions create potential growth headwinds that could necessitate increased spending, with gilt yields remaining vulnerable to US Treasury movements.

Currency fluctuations significantly impacted sterling-based investors in US government securities. The hedged ICE BofA US Treasury Index posted a 0.54% gain, while its unhedged counterpart declined 2.83%, reflecting sterling’s appreciation against the dollar. Market expectations still include at least three Federal Reserve rate reductions this year, though probability of a fourth cut diminished to approximately 30% following stronger-than-anticipated employment data. Analysts note that while the current administration’s economic policies are pronounced, their initial effects remain modest and will require time to fully manifest, suggesting rate adjustments are more likely in the latter half of the year. Despite recent price corrections making US Treasuries more appealing from a valuation perspective, fiscal sustainability concerns and uncertainties surrounding global trade disruptions’ impact on Treasury demand, and inflation maintain our neutral stance.

Credit markets felt the broader volatility effects. High-yield bonds delivered flat April returns despite widening spreads, with energy sector weakness proving particularly detrimental. Investment-grade corporate debt outperformed higher-yielding alternatives as investors prioritized quality amid macroeconomic uncertainty.

We currently maintain a balanced position towards fixed income, with our core portfolios diversified across UK and US sovereign debt, emerging markets, and corporate credit. We emphasise active management within corporate credit sectors, believing that substantial market movements and opportunistic selling have created attractive entry opportunities, though selective security analysis remains crucial.

Ask us anything

Q: Do you have exposure to gold within portfolios? What is your view on it?

A: Yes, we maintain exposure to physical gold via an exchange traded fund across most of our portfolios, with approximately 5% allocation in our Balanced Fund.

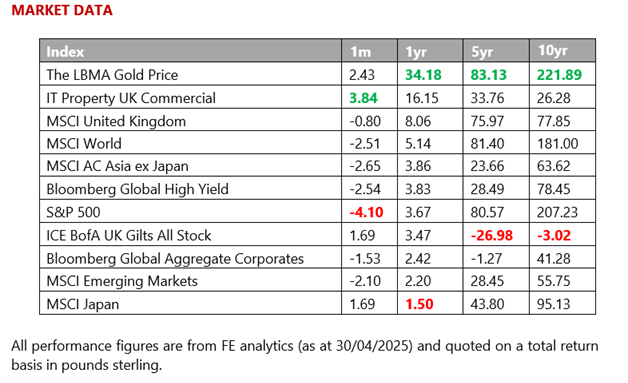

We have held a favourable view towards gold for some time as a geopolitical volatility hedge – a market characteristic we expect to persist over the near to intermediate horizon. We tactically increased our gold position in early 2025, anticipating policy shifts following the presidential transition. This thesis has materialised effectively, with gold emerging as a standout performer during the administration’s initial months. Gold prices have reached unprecedented levels (approaching $3,080 per ounce), delivering nearly 20% returns to sterling-based investors through April.

The current administration’s approach to trade policy – imposing substantial tariffs based on deficit metrics rather than actual trade barriers – signals a preference for balanced rather than free trade. This stance represents not only a decisive shift away from globalisation but also potentially a departure from the dollar-centric monetary framework that has prevailed since Bretton Woods ended in 1971. Throughout this period, the dollar has functioned as the world’s primary reserve currency, commanding a disproportionate share of official reserves and international transactions relative to America’s global economic footprint. This system has underpinned the rules-based trading order, reinforced by stable geopolitical alliances.

A key consequence of this dollar hegemony has been the channelling of international dollar revenues into US assets, particularly Treasury securities, widely regarded as foundational ‘safe’ investments within the global financial architecture. Foreign holdings extend significantly into US equities and private credit markets. These cumulative flows have resulted in America’s negative $26 trillion net international investment position, as referenced in the 2 April presidential address.

It requires little economic expertise to recognise that the current tariff-oriented challenge to global trading norms could trigger substantial repatriation flows, accompanied by reassessment of dollar assets’ ‘safety’ and America’s relative economic prospects. Given the scarcity of credible alternatives, gold’s position as a primary beneficiary of such repatriation appears logical. Central banks and investors have increasingly turned to gold this year for reserve diversification and macroeconomic uncertainty protection.

While this might suggest an obvious investment case, it’s worth noting our longstanding position in this asset, making current valuations potentially less optimal for new entry. Any exposure should be calibrated according to individual risk tolerance, particularly considering potential heightened volatility following recent sharp price appreciation.

Gold stands alone among major commodities in exceeding its inflation-adjusted historic peak, reflecting its status as a monetary rather than commodity asset. The broader commodity complex – including diesel, steel, and fossil fuel derivatives – significantly influences gold producers’ cost structures. With cost inflation from these inputs and labour substantially moderated compared to 2021-22, record gold prices translate to unprecedented profit margins for producers. Longer-term, elevated prices typically stimulate increased production, which could exert downward price pressure in coming years.

While our outlook remains positive over the short-to-medium term, we view gold as requiring active management rather than a passive buy and hold approach.

Key takeaways

Investing in equities involves taking risk that a client needs to be comfortable with.

• We have tactical exposure to physical gold across our multi-asset funds that we have held for the past few years.

• We increased exposure at the start of 2025 as a hedge against geopolitical volatility.

• Gold has been one of the best performing assets year to date.

• The sharp rise in price does, however, make now a less attractive entry point for investors.

If there is a question you’d like to pose to our team, please reply to this email or write to [email protected].

The Monthly Market Commentary (MMC) is written and researched by Scott Bradshaw, Lauren Hyslop and Jonathon Marchant for clients and professional connections of Mattioli Woods and is for information purposes only. It is not intended to be an invitation to buy, or to act upon the comments made, and all investment decisions should be taken with advice, given appropriate knowledge of the investorʼs circumstances. The value of investments and the income from them can fall as well as rise and investors may not get back the full amount invested. Past performance is not a guide to the future.

Mattioli Woods Limited is authorised and regulated by the Financial Conduct Authority.

Sources: All other sources quoted if used directly, except fund managers who will be left anonymous; otherwise, this is the work of Mattioli Woods.