Global markets summary

October proved excellent for investors, with both shares and government bonds delivering strong returns, a welcome combination that doesn’t happen often. The month started nervously with US-China trade tensions unsettling markets. However, a last-minute trade deal changed everything. The agreement paused American tariffs and secured Chinese cooperation on vital technology materials, sending tech shares soaring across Asia.

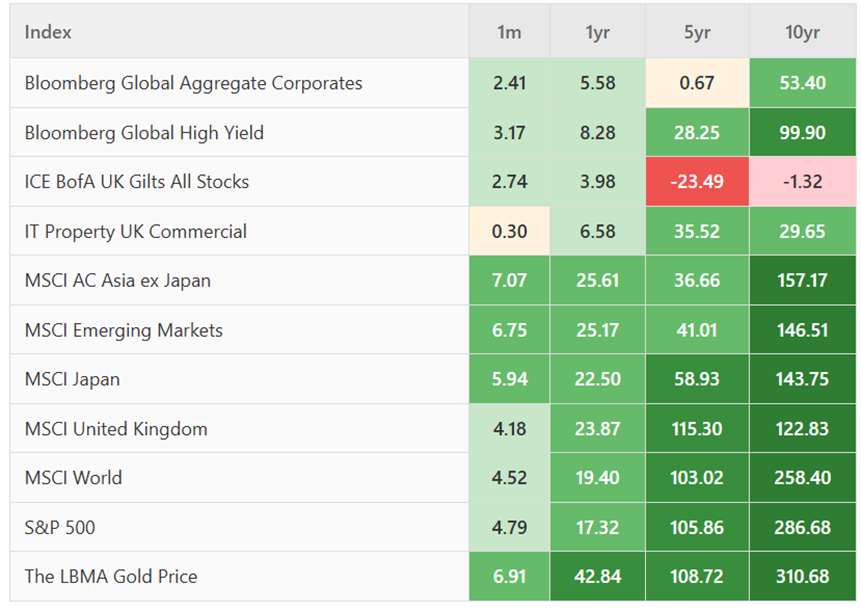

US shares led the way, with the S&P 500 gaining 4.84% for UK investors (helped by the dollar strengthening against the pound). The big American tech companies continued attracting money, while strong company earnings justified the optimism with over 80% of firms beating expectations. Asia Pacific (ex-Japan) markets performed even better at 6.30%, particularly Taiwan and South Korea, which benefited from the AI boom. Japan’s market surged after electing its first female prime minister, whose pro-growth policies weakened the yen and boosted exporters. UK large companies gained 4.49%, helped by commodity strength and overseas earnings. However, smaller UK firms managed just 1.03%, as investors worried about the upcoming Budget.

UK Government bonds were October’s surprise winner. After the Bank of England governor hinted at more rate cuts, bond prices jumped. Markets now expect lower interest rates through 2026. In America, while the Federal Reserve cut rates as expected, unclear signals about future cuts left investors adjusting their expectations.

Precious metals continued their remarkable run – gold up 52% and silver up 69% for the year. Industrial metals gained 4.8%, suggesting confidence in global growth, while oil prices remained steady despite supply concerns.

As October ended, markets found themselves perched at an intriguing crossroads. US equities hover near all-time highs, suggesting much good news is already in the price. Yet the month’s resilience, weathering geopolitical storms, digesting mixed central bank signals, and navigating earnings seasons, speaks to underlying market strength. In our view, diversification beyond America’s increasingly concentrated market leadership offers both protection and opportunity in equal measure.

United Kingdom

UK equities delivered yet more positive performance during October, though lagged global peers. As we have seen many times over the past twelve months, large-cap stocks outperformed mid-cap peers. October’s outperformance was particularly noteworthy, in terms of both the size of the outperformance and underlying market dynamics.

Though it garnered few column inches, UK gilts rallied strongly over the month on the back of softer inflation data and the sense that the Autumn Budget is likely to show some degree of fiscal restraint. The yield on 10-year UK gilts fell from 4.70% to almost 4.40% over the month, in what was a particularly sharp contraction. Given the implications for lower financing costs and signals around the increased chance of future interest rate cuts, one could be forgiven for expecting a stronger period for more domestically-focused stocks.

Part of the reason this failed to materialise was a strong set of Q3 updates from UK-listed banks, with HSBC, Barclays, NatWest and Standard Chartered all exceeding analyst expectations. Of course, the question for the banks and the wider market is, ‘How long are interest rates likely to remain at current levels?’, and much of this depends on economic data.

During October, a number of indicators fell short of expectations, increasing the odds of an interest rate cut before the end of the year. Firstly, monthly house price data from Halifax fell unexpectedly and the annual rate of growth was the weakest since April 2024. This was compounded by data from RICS, which showed home listings falling at the fastest pace for two years, suggesting Budget uncertainty has taken hold in the property market.

The market was most interested in private sector pay and jobs numbers. Both of which fell short on estimates and increased the odds of the Bank of England taking action. Those calling for cuts were emboldened towards the end of the month, with inflation figures coming in below expectations.

With the data remaining mixed and a relatively wide range of outcomes from the Budget later in the month, it feels that the last two months of 2025 are going to play an important role in charting the course for 2026. While our underweight position to large-cap names has been a headwind, we believe that the combination of a better-than-expected Budget and an unexpected interest rate cut could be important catalysts for mid- and small caps.

North America

While autumn leaves fell across Britain, US markets bloomed in spectacular fashion, defying the dreaded ‘Octoberphobia’ that haunts traders’ memories from the crashes of 1929 and 1987. For UK investors, Wall Street delivered a rather splendid treat this October 2025, with the S&P 500 serving up a 4.84% return (sweetened further by the dollar’s muscle against sterling).

The real fireworks came from Silicon Valley’s elite. The ‘Magnificent Seven’ tech giants continued their reign, with Amazon stealing the show on the final Friday, rocketing 9.6% after its cloud computing unit flexed impressive growth figures. CEO Andy Jassy’s proclamation of “strong demand in AI and core infrastructure” sent ripples through the market, lifting fellow tech darlings Palantir and Oracle in its wake. However, the month’s true headline-grabber was NVIDIA, which shattered records to become the world’s first $5 trillion company. CEO Jensen Huang painted a picture of AI’s “virtuous cycle”, where growing usage drives investment, which improves AI, which boosts usage, and round it goes. Big tech backed this vision with eye-watering capital expenditure commitments, most earmarked for AI infrastructure.

The earnings season proved equally impressive, with 82% of reporting companies exceeding expectations by an average of 6.4%. Add in the Federal Reserve’s surprise 25-basis-point rate cut, and you had the perfect cocktail for market optimism.

While the rally remained narrow, with growth stocks hogging the spotlight while value and mid-caps played supporting roles, the tech-heavy Nasdaq’s 4.7% climb suggested AI enthusiasm has evolved from sugar rush to something more substantial.

Yet with valuations at vertigo-inducing heights, a touch of British prudence seems sensible. We’re positioning portfolios to capture the lion’s share of any market ascent while maintaining a subtle defensive tilt. Rather than betting everything on the increasingly concentrated index – where the ‘Magnificent Seven’ command an almost imperial presence – we’re casting our net wider across corporate America, giving exposure to companies beyond the tech titans’ spotlight. To execute this, we’re blending actively managed funds, where seasoned stock-pickers navigate these frothy waters, with passive instruments that keep costs in check. It’s a measured approach for what could prove to be interesting times ahead. After all, while the Wall Street party shows no signs of ending, we’d rather be the guest who enjoys the festivities but keeps their car keys handy.

Europe

European markets delivered a perfectly decent, if unspectacular, October performance for UK investors. The EURO STOXX’s 3.04% return in sterling terms was rather like a reliable saloon car parked next to Wall Street’s flashy sports cars: solid, sensible, but hardly setting pulses racing.

The European Central Bank played statue, keeping its deposit rate frozen at 2% despite inflation easing to a comfortable 2.1%. This steady-as-she-goes approach seemed to suit markets just fine, though it did create an interesting contrast with the Fed’s surprise rate cut across the Atlantic.

The month’s most intriguing development came from an unexpected quarter: whispers of a US-China trade détente at the APEC summit, with Presidents Trump and Xi apparently making progress on rare-earths and agricultural trade. This diplomatic thaw sent a warming breeze through European markets, particularly benefiting the continent’s tech darlings, like ASML, riding the global AI enthusiasm wave.

Not all was rosy in the corporate earnings garden, however. Novartis stumbled on profit expectations (down 4%), while Philips took a 6% tumble after attracting unwanted FDA attention. The banking sector served up its usual mixed bag, with BNP Paribas delivering lukewarm results and HSBC setting aside a hefty $1.1 billion in provisions.

With European valuations at 15.5× forward earnings looking positively bargain-basement compared to America’s lofty 24.9×, there’s clear appeal for value-hunters. Yet after a stellar year-to-date performance (especially in euro terms), we’re witnessing what feels like a natural pause for breath – an ‘air pocket’ as markets digest recent gains.

Our verdict? We’re maintaining Swiss-like neutrality on European equities. The long-term structural story remains sound, but with the ECB seemingly done cutting rates while the Fed keeps trimming, near-term momentum may favour our American cousins. Sometimes, sitting on the fence is exactly the right place to be.

Rest of the world

While Wall Street grabbed headlines and Europe plodded along respectably, the Pacific Rim served up a decidedly mixed bag for UK investors in October. The MSCI Asia Pacific ex-Japan delivered a robust 6.30% return in sterling terms, though China proved the party pooper with a -1.44% decline, while Japan’s TOPIX added a respectable 4.32%.

The Land of the Rising Sun witnessed genuine history in October as Sanae Takaichi shattered the ultimate glass ceiling, becoming Japan’s first female Prime Minister. A devoted disciple of ‘Abenomics’, Takaichi’s victory sparked what traders are dubbing the ‘Takaichi Trade’, a bet that Japan’s love affair with expansionary fiscal and monetary policy will continue unabated.

The market’s response was nothing short of spectacular. The Nikkei 225 posted its best monthly performance since January 1994, while the TOPIX scaled record heights. Japanese chipmakers and AI-linked firms rode the global tech wave magnificently, with exporters getting an extra boost from the weaker yen padding their overseas profits.

While Japan celebrated, China provided the sobering counterpoint. The Middle Kingdom’s manufacturing PMI slumped to a six-month low of 49.0 (firmly in contraction territory), dampening spirits despite whispers of targeted stimulus measures. It seems even Beijing’s usually reliable policy toolkit is struggling against structural headwinds.

Yet the broader Asian story remained surprisingly resilient. The IMF’s projection of 4.5% regional growth for 2025 tells of an economy still powering ahead, with Asia contributing a whopping 60% of global growth. The secret sauce? A potent mix of AI supply chain dominance and firms frantically front-loading shipments ahead of threatened US tariff increases.

Korea and Taiwan emerged as October’s regional stars, surging 23% and 10% respectively, their semiconductor sectors basking in the global AI gold rush. These tech-heavy tigers, deeply embedded in the world’s electronics manufacturing web, proved that geography still matters in the age of artificial intelligence.

And then there’s Argentina, the wild card that nobody saw coming. President Javier Milei’s party’s overwhelming midterm election victory sent the MSCI Argentina Index rocketing an eye-watering 64% in a single month. It’s the sort of return that makes even the most seasoned emerging market investor do a double take.

The Pacific markets present a fascinating study in contrasts. Japan’s policy-driven momentum looks set to continue, particularly for exporters and tech plays. The broader Asia-Pacific region offers structural growth at reasonable valuations, though China’s slowdown casts a shadow that bears watching.

Our approach? Selective enthusiasm with a side of caution. We’re favouring Japanese exporters riding the Takaichi wave and Asian tech champions feeding the AI beast, while keeping a weather eye on Chinese headwinds and US trade tensions. In emerging markets, we’re hunting for domestic growth stories and green investment themes that can weather the geopolitical storms. After all, in a region where one market can surge 64% while another contracts, picking your spots carefully isn’t just prudent, it’s essential.

Fixed income

After years of playing second fiddle to equities, the fixed income universe delivered a rather satisfying October for those wise enough to pay attention. While equity markets grabbed headlines with their tech-fuelled theatrics, bonds quietly went about their business of actually generating returns.

UK Government bonds put on quite the show in October, with 10-year gilt yields tumbling 31 basis points from 4.70% to 4.39%. It’s the sort of move that had bond managers reaching for the champagne (or at least a decent cup of tea). The catalyst? Growing conviction that the Bank of England will deliver a December rate cut, like an early Christmas present to the bond market. Yet all is not entirely rosy in Westminster. Whispers of a £50 billion fiscal shortfall ahead of the November Budget kept long-end yields elevated, rather like having a splendid party while knowing the caterer’s bill is still to come. The yield curve steepened accordingly, as markets priced in both monetary easing and fiscal anxiety.

US Treasuries played a more subdued tune, with the 10-year yield hovering around 4.10% and the 2-year at 3.60%. Despite September’s 25 basis point Fed cut, Chairman Powell’s careful commentary tempered expectations for December fireworks. The yield curve remained stubbornly inverted, that uncomfortable warning signal that refuses to go away, like an unwelcome house guest who’s overstayed their welcome.

Looking across sectors, emerging market (EM) debt delivered strong performance in October, benefiting from the dual tailwinds of attractive real yields and dollar weakness. Having started their tightening cycles ahead of developed markets, many EM central banks established substantial rate differentials that continue to appeal to investors as inflationary pressures ease. In credit markets, global high yield outperformed investment grade, as higher starting yields were sufficient to offset modest spread widening in both markets.

Our positioning reflects these dynamics. We remain negative on US Treasuries, where limited rate cut potential and persistent inversion offer poor risk-reward. UK gilts warrant a neutral stance, while near-term rate cuts provide support, fiscal concerns cap the upside. Investment grade credit looks unappealing, with spreads at multi-decade lows offering minimal compensation for duration risk. High yield merits neutrality, as decent carry is balanced against late-cycle concerns. Our conviction lies in emerging market debt, where attractive real yields, early-cycle positioning, and ongoing rate differentials create the most compelling opportunities in fixed income.

Ask us anything

Q: Should we be worried about an ‘AI bubble’ and potential market crash? How would this impact your funds?

A: The question of whether we’re witnessing an AI bubble is one we take extremely seriously and for good reason. With chipmaker NVIDIA trading at over $4 trillion, and AI startups commanding eye-watering valuations reminiscent of the late-1990’s dot-com era, it’s natural to feel a sense of déjà vu. Even industry titans like Sam Altman and Jeff Bezos have sounded notes of caution about investor exuberance outpacing actual returns.

Why this time feels different (yet familiar)

Here’s what keeps us up at night: AI companies are trading at extraordinary multiples, some beyond 90 times revenue. The ‘Magnificent Seven’ tech giants now comprise nearly 40% of the S&P 500. MIT research suggests 95% of generative AI projects are failing to deliver material returns. These are legitimate red flags that demand attention.

Yet beneath the froth lies something more substantial than the dot-com era’s ‘build it and they will come’ optimism. Today’s AI leaders (Microsoft, Alphabet, Meta) are sitting on mountains of cash and generating real revenue. They’re spending nearly $80 billion per quarter on tangible infrastructure: data centres, chips, and computing power that form the backbone of a new economic layer. This isn’t venture capital chasing website traffic; it’s industrial-scale capital formation.

Our verdict: both/and, not either/or

After extensive analysis, we’ve concluded that AI represents both a genuine structural transformation and carries significant valuation risks. Think of it as the difference between recognising electricity would change the world in 1890 (correct) while also acknowledging that not every electric company stock was a wise investment (also correct).

The AI revolution is real; it’s reshaping everything from medicine to manufacturing. However, in their enthusiasm, markets have likely got ahead of themselves in pricing this transformation.

How we’re positioning your investments

Rather than making an all-or-nothing bet, we’ve crafted a strategy we call ‘intelligent exposure’, capturing meaningful upside while protecting against potential downturns.

Strategic selection over index following

While we maintain some passive exposure to keep costs low, we’ve shifted primarily to active management in US markets. Our carefully selected managers can identify genuine winners while sidestepping the most overvalued segments. Yes, this means we might lag during momentum-driven rallies when AI stocks surge indiscriminately, but it provides far better risk-adjusted returns over time.

Focus on foundations, not fantasies

We’re investing in proven AI enablers – established chipmakers, cloud providers, and software firms with solid fundamentals. The unprofitable startups trading at astronomical valuations? We’re giving those a wide berth.

Diversification inside and outside AI

We’re counterbalancing mega-cap concentration by adding exposure to emerging technologies like robotics and international markets that offer AI opportunities at more reasonable valuations.

What this means for your portfolio

Should markets correct, and history suggests they will at some point, our approach means your funds won’t bear the full brunt of an AI selloff. We’re participating in the revolution without betting the farm on it. Think of it as having a ticket to the show without camping overnight in the queue.

The bottom line: we believe AI will fundamentally reshape our economy over the coming decades. But we also believe that disciplined, thoughtful investing – not FOMO-driven (fear of missing out!) speculation – is how we’ll help you benefit from this transformation while sleeping soundly at night.

Markets may experience boom-bust cycles within AI segments, but by maintaining our balanced approach, we’re positioned to weather the storms while capturing the long-term structural growth this technology promises.

If there is a question you’d like to pose to our team, please reply to this email or write to [email protected].

Four key takeaways from October:

- Stocks and bonds both won: October saw rare simultaneous gains in equities and bonds.

- US tech concentration hit extremes: NVIDIA became the first $5 trillion company, but US valuations at 24.9x earnings far exceed Europe’s 15.5x.

- Asia outperformed, UK lagged: Asia-Pacific gained 6.30% on AI boom while UK mid-caps managed just 1.03% on Budget fears.

- US-China trade deal changed everything: a last-minute agreement pausing US tariffs and securing Chinese cooperation on technology materials sent tech shares soaring across Asia.

MARKET DATA

All performance figures are from FE analytics (as at 31/10/2025) and quoted on a total return basis in pounds sterling.

The Monthly Market Commentary (MMC) is written and researched by Scott Bradshaw, Lauren Hyslop and Jonathon Marchant for clients and professional connections of Mattioli Woods and is for information purposes only. It is not intended to be an invitation to buy, or to act upon the comments made, and all investment decisions should be taken with advice, given appropriate knowledge of the investorʼs circumstances. The value of investments and the income from them can fall as well as rise and investors may not get back the full amount invested. Past performance is not a guide to the future.

Mattioli Woods Limited is authorised and regulated by the Financial Conduct Authority.

Sources: All other sources quoted, if used directly, except fund managers who will be left anonymous; otherwise, this is the work of Mattioli Woods.