Global markets summary

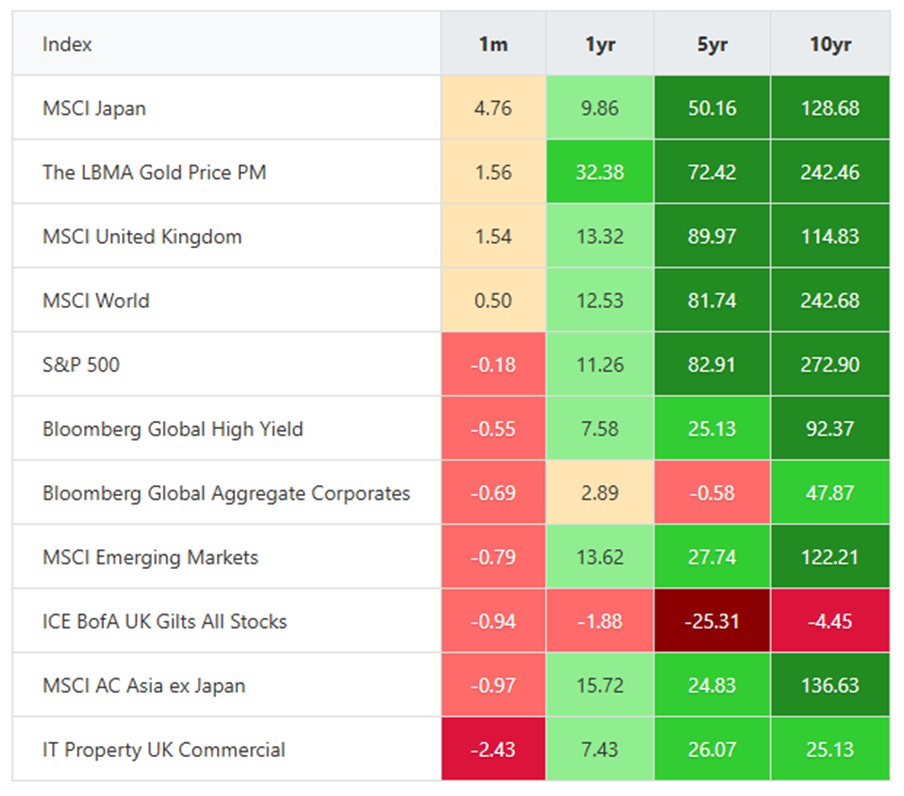

September proved a rewarding month for equity investors, with global markets delivering solid gains despite persistent geopolitical tensions and fiscal uncertainties. The standout performer was China, where the MSCI China Index surged 10.14%, fuelled by a potent cocktail of domestic liquidity and technological breakthroughs in artificial intelligence. Cash-rich Chinese households, faced with paltry interest rates and limited investment alternatives, have poured funds into equities since April, shrugging off concerns about slowing growth and deflation.

The US S&P 500 advanced 3.98% (in £ terms) for the month, with communication services, industrials and financials leading the charge. Yet beneath the headline strength, cracks emerged in healthcare and consumer discretionary stocks, where lofty valuations met cooling growth expectations. Meanwhile, UK equities trailed their global peers, with the MSCI UK Large Cap Index eking out a modest 1.58% gain as investors adopted a wait-and-see approach ahead of the Autumn Budget.

Fixed income markets painted a more nuanced picture. UK gilts suffered a particularly bruising September, as yields climbed to multi-decade highs while emerging market debt continued its outperformance, buoyed by a softer dollar and robust fundamentals. Global high-yield bonds delivered solid returns, supported by resilient corporate earnings and attractive yield levels.

The year-to-date picture tells a fascinating tale of shifting global dynamics. In a reversal of the past decade’s script, US markets have ceded leadership to Asia Pacific and European equities, hampered by trade tensions and a weakening dollar. Gold has emerged as 2025’s star performer, soaring over 40% to breach $3,700 per ounce – its best showing since 1979 – as central banks stockpiled the precious metal amid mounting geopolitical uncertainties.

Looking ahead, the investment landscape presents both opportunities and challenges. Equity valuations sit comfortably above long-term averages, particularly in the US, suggesting much good news is already priced in. As tariff-induced inflation risks linger and trade uncertainties persist, maintaining a well-diversified portfolio across regions and asset classes remains paramount for navigating the months ahead.

United Kingdom

UK equities delivered positive performance during September, though lagged global peers. In terms of data, the UK continues to present a mixed picture, with growth proving resilient, but confidence among consumers and business is lacking. GDP expanded 0.3% quarter-on-quarter as expected, though the year-on-year rate of 1.4% exceeded consensus. This resilience prompted the OECD to upgrade Britain’s 2025 growth forecast to 1.4%, positioning it as the second-fastest growing G7 economy, albeit with expectations of a slowdown to 1% in 2026.

However, forward-looking indicators painted a less optimistic picture. The Lloyds Business Barometer plummeted from 54 to 42, while the Purchasing Manufacturers Index, a key measure of economic activity, disappointed across the board. The Composite PMI fell to 51 from 53.5, with services dropping to 51.9 and manufacturing remaining firmly in contraction territory at 46.2.

Consumer activity showed greater resilience. Retail sales rose 0.5% in August, while the British Retail Consortium’s high street sales tracker reported particularly strong like-for-like growth of 6.3% year on year to late September, helped by cooler weather boosting apparel and homeware sales. Housing market data remained mixed: mortgage approvals reached a six-month high in July, yet house price appreciation moderated to 2.1% annually by August.

The inflation picture proved stickier than hoped, with August’s 3.8% reading in line with expectations but forecast to peak at 4%. Wage growth edged up to 4.7%, while unemployment held at 4.7%. These persistent price pressures, combined with weakening business confidence and activity indicators, present a challenging backdrop for the Bank of England’s Monetary Policy Committee and limit prospects of a further rate cut this year.

Political uncertainty remains relatively high, with the Prime Minister facing pressure from both inside and outside of his party. With the Autumn Budget scheduled for next month and a seemingly broad range of options on the table, it is difficult to see activity picking up materially before the end of the year.

Despite the headwinds, UK equities have delivered strong returns this year, in a stark reminder that companies and economies are two fundamentally different things. This is particularly true of the UK market, where global revenues are far more dominant than domestic in the large-cap space. While we have seen the largest names in the index outperform, we continue to see the best value and most attractive prospective returns in the mid- and small-cap space. While there is a lot of fear around the Budget, we are optimistic that the Government knows that its strategy over the past year has not worked and it is time to reset the course for the years ahead, with less focus on taxation and a greater emphasis on growth.

North America

The S&P 500 rose by a solid 3.98% in sterling terms during September, though momentum waned towards month end as comments from the Federal Reserve (Fed) suggested interest rates might stay higher for longer than investors had expected.

The month’s standout performer was the energy sector, which surged alongside crude prices after President Trump urged European nations to cease Russian oil and gas purchases – a call that underscored ongoing geopolitical tensions affecting global energy markets.

Yet it was the Fed’s shifting rhetoric that dominated sentiment as September drew to a close. Chair Jerome Powell acknowledged the economy faces a “challenging situation”, caught between inflation risks and labour market concerns, while pointedly observing that “equity prices are fairly highly valued”. His colleagues echoed these cautious notes, with officials from St Louis and Atlanta openly questioning the need for further monetary easing.

Economic data largely validated this measured approach. Core inflation, the Fed’s preferred gauge, held steady at 2.9% year on year – stubbornly above target but not accelerating. More encouraging was the upward revision to second-quarter growth, now pegged at a robust 3.8% annual rate, driven by resilient consumer spending.

Forward-looking indicators painted a picture of an economy maintaining its stride, if not quite sprinting. Manufacturing and services PMI readings both exceeded 50, signalling continued expansion, with business optimism reaching four-month highs. As S&P Global’s chief economist noted, the data suggests third-quarter growth tracking at a healthy 2.2% pace.

The OECD’s upgraded global growth forecast added further context, with the organisation now expecting 3.2% expansion in 2025. Intriguingly, much of this strength reflects businesses front-loading activity ahead of anticipated tariff increases – a reminder that policy uncertainty continues to shape corporate behaviour.

For UK investors, the US market presents a familiar dilemma. The fundamentals remain solid – growth is robust, the AI revolution provides structural support, and merger activity is picking up. Yet valuations appear stretched, and markets have enjoyed an extended run without meaningful correction. A selective approach, looking beyond the mega-cap dominated indices, may prove prudent as we navigate the months ahead.

Europe

European shares delivered a solid 3.57% return in September, though beneath the headline figure lay a market increasingly divided by sector-specific fortunes and the shadow of transatlantic trade tensions.

Financial stocks emerged as the month’s clear winners, propelled by robust earnings and successful cost-cutting programmes. Deutsche Bank’s return to the EURO STOXX 50 Index symbolised the sector’s rehabilitation. By contrast, consumer discretionary names struggled under the weight of disappointing guidance – ASOS being a notable casualty – while automotive shares found themselves in the crosshairs of tariff concerns. Materials stocks also retreated as US levies on timber products began to bite.

The economic backdrop offered modest encouragement. The Eurozone Composite PMI edged up to 51.2, its highest reading in 16 months, keeping the region firmly in expansion territory. Services led the charge, recording its strongest performance of the year, while manufacturing maintained a more pedestrian pace. This divergence was reflected in business confidence, which slipped to a four-month low as industrial pessimism offset services sector optimism.

Germany, Europe’s economic engine, sent characteristically mixed signals. The Ifo Institute reported an unexpectedly sharp drop in business sentiment as companies fretted about the outlook. Yet consumer confidence, as measured by GfK, showed signs of improvement, with households feeling more sanguine about their income prospects.

The European Central Bank’s decision to hold rates steady at 2% provided a tailwind for cyclical sectors, while the euro’s weakness offered exporters a competitive edge. More significantly, Germany’s ambitious €500 billion infrastructure programme continues to underpin longer-term optimism about the region’s growth potential.

For UK investors, European equities present a nuanced picture. Valuations remain attractive relative to other developed markets, and fiscal stimulus provides structural support. However, trade uncertainties and uneven economic momentum counsel against unbridled enthusiasm. A neutral stance appears warranted – acknowledging both the opportunities in financials and infrastructure plays, while remaining mindful of the headwinds facing consumer and industrial names.

Rest of the world

Asia-Pacific equities delivered stellar returns in September, with the MSCI Asia Pacific Index climbing 6.16% for sterling investors, as semiconductor powerhouses South Korea and Taiwan scaled record highs on artificial intelligence euphoria.

The region’s chipmakers led the charge, buoyed by insatiable demand for AI infrastructure and expectations that US rate cuts would sustain the technology boom. This optimism proved particularly infectious in North Asia, where hardware manufacturers stand to benefit most directly from the AI revolution.

Japan’s TOPIX index posted a more modest 2.60% gain in sterling terms, as mixed signals clouded the monetary policy outlook. Tokyo’s inflation reading of 2.5% year on year fell short of the anticipated 2.8%, temporarily cooling speculation about imminent Bank of Japan rate rises. Yet the dissent of two Bank of Japan board members at September’s meeting – both favouring tighter policy – suggests a hike remains possible before year end. Japanese pharmaceuticals proved a notable drag, caught in the crossfire of fresh US tariff announcements targeting the sector.

The yen’s slide to 149.5 against the dollar reflected both domestic political uncertainty ahead of the Liberal Democratic Party leadership race and broad dollar strength, as robust US data dampened expectations for aggressive Federal Reserve easing.

China’s technology giants staged a remarkable rally, with Alibaba surging 31% and Baidu jumping 48% in September alone. The sector’s renaissance – bringing year-to-date gains to 96% for Alibaba and 59% for Baidu – was underpinned by genuine technological progress. Home-grown AI models like Alibaba’s Qwen and Baidu’s Ernie garnered strong industry rankings, while President Xi’s earlier rapprochement with tech leaders signalled Beijing’s renewed embrace of the sector as crucial to national competitiveness.

Yet this tech exuberance masked persistent weakness in China’s old economy. Manufacturing contracted for a sixth consecutive month (the longest slump since 2019) as tariff pressures and trade tensions continued to weigh on industrial activity.

For UK investors, the region presents a study in contrasts. The structural AI story remains compelling, particularly for semiconductor and software plays. However, geopolitical frictions and China’s uneven recovery warrant caution. Our neutral stance across Japanese, Asia-Pacific and emerging market equities reflects this delicate balance – acknowledging the opportunities while respecting the risks in an increasingly fractured global landscape.

Fixed income

September’s bond markets offered a masterclass in divergence, as traditional safe havens stumbled while riskier segments flourished. UK gilts endured a particularly torrid month, with 30-year yields climbing to eye-watering levels around 5.7% – heights not seen in decades. The combination of stubbornly elevated inflation and mounting fiscal anxieties left UK Government bonds nursing painful losses, leaving many investors questioning whether the gilt market’s traditional role as portfolio ballast has been permanently compromised.

Across the Atlantic, US Treasuries fared somewhat better, though yields still drifted higher. The 10-year yield nudged up to approximately 4.20%, while the 30-year reached 4.77%, as robust economic data forced traders to recalibrate their expectations for Federal Reserve largesse. The resilient American economy, it seems, requires less monetary medicine than markets had anticipated.

Yet while developed market government bonds struggled, emerging market debt continued its remarkable renaissance. Local currency emerging market debt has surged 13.8% year to date, with hard currency bonds not far behind at 8.7%. This stellar performance owes much to the dollar’s retreat and surprisingly resilient emerging market fundamentals, a sharp contrast to the doom-laden predictions that dominated headlines just eighteen months ago.

Corporate credit markets offered shelter from the government bond storm. Global investment grade bonds posted modest gains between 0.5% and 1.3%, depending on region, as investors sought quality amid macro uncertainty. Credit spreads tightened further, rewarding those who maintained faith in corporate balance sheets. High-yield bonds delivered an even more impressive 1.1% monthly return, with yields hovering around 7%, a compelling proposition for income-seekers willing to venture down the credit spectrum.

The stark performance gap between government and corporate bonds underscores a crucial shift in fixed income dynamics. With traditional sovereign debt no longer offering reliable diversification benefits, investors are increasingly turning to credit markets and emerging economies for both returns and portfolio protection, a trend that shows little sign of abating as we navigate the final quarter of 2025.

Ask us anything

Q: What does ‘US government shutdown’ mean and specifically what does it mean for markets? Should we be worried about this?

A: Imagine the UK Parliament failing to agree on a budget, forcing Whitehall to temporarily close its doors. That’s essentially what’s happening across the Atlantic. As of 1 October 2025, the US federal government has partially shut down because Congress couldn’t agree on spending plans.

Unlike the UK’s parliamentary system, the US Congress must regularly approve funding bills to keep government departments running. When Democrats and Republicans can’t reach agreement – as has just occurred – non-essential government services grind to halt. Federal employees are sent home without pay (though they’re typically compensated later), national parks close, and economic data releases are delayed.

This is the first shutdown since 2018, when the impasse lasted over a month. Crucially, unlike the 2013 shutdown, this isn’t tangled up with America’s debt ceiling – the legal limit on government borrowing. That’s significant, because debt ceiling crises can genuinely rattle global markets by raising the spectre of a US default.

However, there’s a new wrinkle: threats to permanently eliminate some government positions, adding uncertainty for affected workers.

History suggests minimal lasting damage to markets. Based on previous shutdowns, US economic growth might slow by roughly 0.1-0.2% per week – noticeable but not catastrophic. Once resolved, the economy typically rebounds as delayed government spending resumes and workers receive back pay.

For UK investors, the immediate effects are likely to be:

• delayed US economic data, making markets slightly more uncertain

• possible short-term volatility in US equities

• minimal impact on UK markets, unless the shutdown drags on for months

Think of government shutdowns like temporary roadworks on a motorway – they cause delays and frustration but don’t change your ultimate destination. Historical evidence shows these political theatrics rarely derail long-term investment returns.

The prudent approach? Stay focused on your financial goals, whether that’s retirement planning or building wealth. Resist the temptation to make knee-jerk portfolio changes based on Washington’s political drama. Well-diversified portfolios are designed to weather such storms.

If there’s a question you’d like to pose to our team, please reply to this email or write to [email protected].

Four key takeaways from September:

- Global equities rallied in September, led by China’s AI-driven surge and strong US and European market gains, despite geopolitical and fiscal headwinds.

- US markets showed resilience, but stretched valuations and cautious Federal Reserve commentary suggest selective positioning is prudent.

- European equities offered value, with financials outperforming, though trade tensions and uneven economic signals warrant a balanced stance.

Asia-Pacific outperformed, driven by AI optimism and tech demand, while Japan’s policy uncertainty and yen weakness added complexity.

MARKET DATA

All performance figures are from FE analytics (as at 30/09/2025) and quoted on a total return basis in pounds sterling.

The Monthly Market Commentary (MMC) is written and researched by Scott Bradshaw, Lauren Hyslop and Jonathon Marchant for clients and professional connections of Mattioli Woods and is for information purposes only. It is not intended to be an invitation to buy, or to act upon the comments made, and all investment decisions should be taken with advice, given appropriate knowledge of the investorʼs circumstances. The value of investments and the income from them can fall as well as rise and investors may not get back the full amount invested. Past performance is not a guide to the future.

Mattioli Woods Limited is authorised and regulated by the Financial Conduct Authority.

Sources: All other sources quoted if used directly, except fund managers who will be left anonymous; otherwise, this is the work of Mattioli Woods.