United Kingdom - April 2023

This month we look at comebacks for our theme, and what better place to start than UK equities, and specifically the largest 100 by capitalisation. As you can see in the table later in this edition, over one year the UK is second only to gold and is in third place over three years. Of course, it matters when these periods start, and the three-year figure in particular is a bit of an odd one due to the mid-Covid-19 outbreak timing of the start date, but the principle (a fine comeback) sticks.

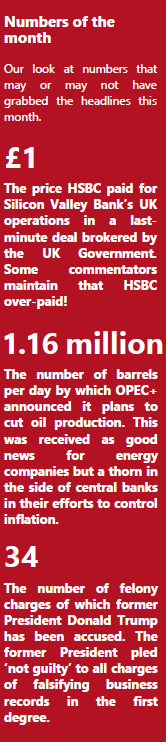

Three years on from the first lockdown, so much has changed, and yet also so little – Brexit continues to weigh heavily economically and on sterling, and yet there is progress (Irish borders, for example); politically, the Conservatives enjoy a large majority, though there have been numerous changes in the top jobs, and neither the PM nor Chancellor remains the same. In the United States, Donald Trump remains joint favourite to be the next President, while facing 34 charges relating to the 2016 Presidential campaign (which he won). So will the comebacks of sterling, Labour and Trump have any impact on risk assets?

In that order, the chances are yes, no and maybe. Were sterling to either weaken much further or start to strengthen, against the US dollar in particular, then different UK listed equities could face much more difficult, or much easier conditions. A Labour win would be unlikely to move markets unless sterling moved significantly as a result (or of short-term policies/perceived changes) and a second Trump Presidency, unlikely as it seems to us in the UK (more likely when you look at US voter reactions) would almost certainly change the geopolitical scenery if not the stage. China would remain under pressure, whereas Ukraine might find the US somewhat less of an ally.

All in all, the comeback we have seen from UK listed equities, specifically the larger companies (UK smaller companies remain in the doldrums) makes sense when you look at the players, and as you will read later, other issues such as decisions on oil production made by the Organisation of Petroleum Exporting Countries (OPEC) and Federal Reserve interest rate decisions will have more impact than more apparently local ones. However, the ‘setback’ of lower sterling, an economy under pressure and not-yet-under-control inflation could just be a ‘setup’ for a comeback of much bigger proportions. Against global equities, UK listed entities are at a significant discount; the very definition of a comeback is about doing something again after a break (growth) and/or becoming popular again.

Term or word(s) to watch: Liminal space – Liminal space refers to the place a person is in during a transitional period. It refers to that place between origin and destination and the transition it describes can be physical (think of a crossroad or the infinite hallways in The Shining) or emotional (such as the period between childhood and adulthood) in nature. The associated feelings with liminal space are of eeriness, apprehension, and nostalgia – which could also describe investors’ emotions during 2022! This period of high inflation and high interest rates could be described as a liminal space as we await some clarity from central banks on how high rates will be pushed and for how long.

North America - April 2023

The failures of several banks in the US have dominated newsflow this month. Though the failures have been somewhat idiosyncratic in nature they still reflect the problems caused by rapid interest rate increases and as such are a warning to investors in a broader sense. When one thinks that the problem assets in this case were US Treasuries, one really gets an understanding of how much strain there is in the system and how losses have been felt even in classically safe asset classes. In terms of wider consequence, we believe this makes a US recession much more likely. Bank lending criteria will become more restrictive and the flow of money to the real economy will become challenged. This might be enough to tip the balance decisively and a recession in the second half of the year is now more plausible than ever. Are markets ready? Well, equity market volatility remains remarkably low, and most indices are pretty stable considering the fact that so many investors are reported to be bearish in their outlook. This could of course be the calm before the storm and the possibility of an earnings recession induced by deteriorating economic conditions makes us extremely cautious. Indeed, it is possible that this will act as a trigger for the next stage of the bear market given that earnings adjustments often follow valuation multiples falls, the like of which we saw last year.

The Federal Reserve will continue to try and separate its inflation and financial stability mandates, raising rates to tackle inflation where needed while protecting the system from the consequences through other measures that enhance liquidity – and that is sort of where we find ourselves. What it means is that temporary relief from lower rates is not on the cards given recent data, and this world of higher rate levels may persist for some time. Remember too that markets often do not bounce back in a sustained way when the central bank makes its first move to reduce rates and we are a long way away from even that point. Unless of course, a more systemic issue arises but in that environment the consolations of looser policy might not be enough to steer investors towards US equities. A lot of experienced investors are now starting to focus on the commercial real estate sector which has already experienced significant challenges and price falls, but the interrelationship between the troubled regional banks and the commercial property means there could be more pain ahead. If more dramatic intervention is needed from policy makers, is this going to get in the way of the inflation fight despite the belief that the mandates can be simultaneously fulfilled? In truth, we are at something of a crossroads for the US equity market.

For the King of all Comebacks, look no further than the attempt of Donald Trump to regain the US presidency in 2024. One might have thought recent legal developments would count against the bid, but his supporter base could be further galvanised by what they perceive as a witch hunt. He has drifted out to 3/1 to be the next President following the indictment, but it could be a drama which ‘entertains’ us for some time…

To reiterate, it is not the fear of another financial crisis à la 2008-09 that we are most focused on after the recent events which unfolded in the US financial system. More it is the ramifications for the US economy via slower growth. Earnings still look to be based more on hope than reality and a reckoning could be due soon. All exposure is strictly focused, mostly through our thematic preferences.

Europe - April 2023

Investor nervousness around the banking sector and protests on the streets, it almost feels like going back in time in Europe at the moment.

A dose of economic reality is currently being experienced in France. President Macron’s attempts to push through pension reforms have resulted in widespread protests and civil disorder. The aim is a pretty modest increase in the retirement age from 62 to 64 (and a corresponding requirement that people work 43 years instead of 41 to qualify for a full pension), but this has been enough to bring the country to a standstill. What has also angered many is the fact that a clause was used to pass the pensions draft law without a vote – a highly inflammatory move. It is unlikely that the impasse can be breached without some sort of deal between the President and the unions – although France has the lowest percentage of union members in the Organisation for Economic Co-operation and Development (OECD), the unions remain a potent force in the country. Astonishingly, over 98% of workers in France are covered by a collective bargaining agreement – compared to less than 30% in the UK. Though the civil unrest is expected to be a short-term development, it is a reminder of the painful adjustments that are going to have to be made by societies and economies. Demographics make current retirement plans and structures across most of the world totally unrealistic and there is a desperation to get people to remain in the workforce for longer. Clearly this is felt more acutely in developed markets such as Europe where life expectancy is that much greater and welfare provisions much more comprehensive, but it is the future across the globe.

We continue to hear hawkish comments from the European Central Bank (ECB) and the feeling is very much that the job has not been completed on inflation. There is form here on the possibility of overtightening too, with a previous ECB administration under Trichet moving aggressively on interest rates right up to the point of financial crisis in 2008, and it will be interesting to see if the current approach survives signs of an economic slowdown. It looks as if Europe, along with the UK, is facing a more stubborn inflation fight than some other regions with numbers still coming in around the 10% level in places.

The effects of falling energy prices help to some degree but there appears to be something of a ‘sticky core’ which could mean that rates stay higher for longer than originally thought. It is also a live question whether the central bank can continue to fulfil its inflation fighting mandate in an environment of instability within the financial space. The travails first of Credit Suisse (we hope Deutsche Bank is not next in line!) do not do wonders for investor confidence in the region. European banks had been major beneficiaries of the rally in the region’s stocks this year, but recent events have inevitably punctured some of the euphoria. We had never been convinced of the merits of the sector and the emergence of problems as we move from a world of zero interest rates to one where we are learning to live with levels nearer 5% was never going to be smooth.

You would have thought Silvio Berlusconi would have been finished after a string of controversies, but the ex-Prime Minister was elected to the Italian Senate in September last year, almost a decade after his ban for tax fraud.

We are optimistic that the financial system is more secure than the most negative commentators suggest but we see enough headwinds in Europe to restrict any enthusiasm here.

Rest of the world - April 2023

March saw President Xi of China visiting Russia with a statement of friendship between the two nations, despite Russia’s growing isolation given the ongoing war in Ukraine. Contrastingly, Japanese Prime Minister Fumio Kishida made a surprise visit to Ukraine a day after, with divisions in Asia showing. Aside from the photo opportunities, the Chinese visit to Russia did see some minor cooperation agreements but not on military – which had the potential for sanctions to be added to China. Russia’s key objective of getting funding for the ‘Power of Siberia 2’ pipeline to transmit gas via Mongolia to China was also not achieved.

Mongolia’s holy animal is the takhi, a small, stocky wild horse. Sadly, the population began to dwindle at the turn of the 20th century caused in part by attempts to catch and transport foals. The last group of wild takhi was spotted around 1969 then, as far as anyone could tell, the creature ceased to exist in the wild. However, thanks to the dedicated efforts of conservationists and just 12 captured horses, the takhi came back from the brink of extinction and were reintroduced to the wild in the 1990s. Though still endangered, these precious animals can now be found in over 30 countries across the world.

While not particularly noteworthy in itself, the changing global relationships behind this trip could have economic implications going forward. Russia has been increasingly drawn into China’s influence. Trade between the two nations increased to a record $190 billion in 2022, up from $147 billion the year before, and Chinese goods delivered to Russia in the first two months of 2023 were up 25%. China has also become Russia’s main export market for oil and gas, with sanctions seeing other markets close.

Russia is now using more Renminbi in its central reserves, transactions and many Russian banks offer savings accounts in this currency directly to retail customers. This has led to many headlines about China trying to compete with and replace the US Dollar’s role as the global reserve currency. From a US perspective, should this ever happen, it will have negative implications. As the global reserve currency, this brings a high demand for this currency meaning the US can borrow more cheaply as well as control elements of the global financial ecosystem – as we saw when it banned Russia from the Swift payment system last year.

The banking crisis we saw last month, alongside the potential upcoming noise around the debt ceiling, may raise concerns about the dollar’s hegemony however, the chances of the US Dollar losing its status overnight are virtually nil. We have seen similar headlines on agreements to use the Renminbi in the past, including in 2009 and 2013 between China and Russia, which has had little impact. The bulk of global trade in all regions (other than Europe) has the US Dollar as by far the most used currency and this will not change quickly. At present, ignoring China to Hong Kong trade, the Mexican Peso is used more widely in global trade.

Somewhat paradoxically, China could also hurt its own economy by becoming a reserve currency too quickly. To become a reserve currency, it would need to be traded without restriction, which goes against the Chinese Central Banks desire to tightly control the economy. Reserve currencies also carry a premium making them more expensive. This would hurt China’s current export led economy, so a restructuring would be needed before then.

The ending of the dominance of the US Dollar in global markets is not expected in the short term, even as China’s currency becomes more widely used. Longer term, China will want a stronger currency and as geopolitics see China and the US compete, alternatives to the dollar could grow in popularity. We see this as something to watch, rather than something to invest in or make decisions based on at present.

Fixed income - April 2023

Bond investors received a punishing lesson this month in the orthodoxy of lending, and how one’s position within a company’s capital structure can be upended to suit the needs of the moment. This lesson came courtesy of the near collapse of what had been the second largest bank in Switzerland, Credit Suisse. In recent years Credit Suisse faced several scandals leading to clients heading for the exit – with $119 billion of funds pulled in the fourth quarter alone the bank was clearly in trouble. Credit Suisse had looked to shore up capital with a plan to borrow $54 billion but when its largest backer, Saudi National Bank, refused to lend further, continued capital outflows and concerns around the strength of the global banking system, following the failure of the US regional bank’s Silicon Valley Bank and Signature Bank, led to an emergency takeover by UBS.

During a match against Belgium in the 2018 UEFA Nations League, Switzerland staged a memorable comeback. Haris Seferovic scored a hat-trick allowing Switzerland to recover from conceding two early goals and eventually shock fans by beating World Cup semi-finalists Belgium 5-2. Credit Suisse in contrast, have scored a number of ‘own goals’.

The takeover (or merger as Credit Suisse termed it) was led by Swiss regulators and the deal forced through without the usual approval from shareholders. Further came the unprecedented news certain bondholders, specifically holders of the $17.5 billion of Credit Suisse AT1 bonds, would be wiped out while Credit Suisse equity holders would receive around $3 billion (1 UBS share for 22.48 Credit Suisse shares). In a typical company capital structure, equity holders rank last and would expect to be last in line for any pay-out (and thus first to soak-up any losses) when a company collapses. This deal optically turned perceived wisdom on its head.

AT1 bonds are part of the capital cushion regulators require banks to hold and which either convert to equity or can be written off if a bank’s capital strength falls below a specified level. By holding this capital there is the possibility a failed bank can avoid the necessity for a taxpayer funded bail-out. As a result AT1 bonds typically offer a higher coupon to compensate for the higher risk, than a bond higher up the capital structure, such as a senior secured bond which will be securitised against assets of the borrower (AT1s are known as subordinated, or unsecured).

So, Credit Suisse equity holders should have been left with nothing? Or, taken the initial losses? Well, it was not quite that simple due to wording in the prospectuses (recommended reading for the insomniac) for these particular Credit Suisse AT1 issues – which allowed the bonds to be written down in a ‘viability event’ and the regulator to disregard the usual order of priority, particularly in a case where government support was needed (as it was in this case).

However, this is not the end of the matter. The AT1 holders were never going to roll-over and accept their losses so expect matters to rumble on via legal means for some time. As for the large body of other AT1s in existence, regulators throughout Europe were swift in reinforcing the usual hierarchy of bonds over equity. They will remain an important element of capital requirements for banks. Whether investors will feel quite so comfortable lending via this means remains to be seen.

We have looked at AT1 bonds on several occasions, most recently in Q3 2022, but had concerns around the impact of recession on European banks and felt the coupons on offer were not sufficient to fully compensate for the heightened risk versus broader investment grade bonds. Of course, at the time we could not have anticipated the ruptures that have now emanated in the space. The situation has been an important lesson in never taking anything for granted in the bond space. Our preference for high quality issuers, through exposure to US Government debt and investment grade bonds, remains.

Infrastructure - April 2023

The change in regime from a decade of low interest rates to rapidly rising rates across developed markets has no doubt been a headwind for the infrastructure sector. A number of yield-starved investors held infrastructure assets as alternative sources of income but sold out of these assets in favour of fixed income assets, which are perceived as lower risk (such as government bonds), when they began to offer a more attractive yield. We have not made a wholesale switch from infrastructure assets to fixed income; we believe these assets continue to play an important role in portfolios, nor do we believe fixed income is inherently low risk (just look at the performance of gilts over the past year).

In our view, the perception of infrastructure assets as mere ‘bond proxies’ lacks an understanding of the true breadth of the asset class and diversified drivers of returns. Our investment in infrastructure includes a blend of operational essential infrastructure assets (such as hospitals, health centres and schools) with exposure to assets with demand-based revenue (for example, rail, toll roads and airports). In addition, there is exposure to assets involved in energy production such as a portfolio of operational wind farms as well as those that facilitate the operation of digital infrastructure like data centres and satellites.

Infrastructure can be seen as an asset class for all weathers. Historically, essential infrastructure assets have a track record of being more defensive than global equities during periods of slowing growth, while assets more exposed to demand offer potentially resilient returns through periods of higher inflation. Power prices have been another important source of returns for a number of our infrastructure assets. Despite regulatory interference from the UK and European governments, our positions with power price connection have been buoyant over the past year as the majority of companies took a prudent approach to power price assumptions, viewing 2022 prices as too good to last. There is also a growth element to the space with the increased demand for new and upgraded infrastructure across the globe as well as its role in the energy transition.

We continue to maintain a healthy exposure to infrastructure across the portfolios via a blend of global listed infrastructure and UK listed investment trusts.

Despite enduring two major conflicts in the last 50 years, the city of Beirut in Lebanon has made a comeback. Hamra, once a hotbed of militia fighting, now has an impressive array of shops and clubs to rival London and Paris. Once left in ruins by war, Beirut’s National Museum has been renovated and since regained its status as a world-famous cultural centre over the past few years.

Financials - April 2023

High profile failures across the banking sector grabbed headlines over March and conjured ghosts of financial crisis past but the situation is very different from 2008.

The contagion began with the failure of US bank Silicon Valley Bank (SVB) then Signature Bank which caused panic across the banking sector. However, on closer inspection, the issues facing both US banks were quite idiosyncratic. SVB had two specific vulnerabilities; its highly concentrated base of depositors, and a large portfolio of long dated government bonds which left the bank sitting on large unrealised losses due to the dramatic rise in yields since 2021. There was a lot of finger pointing about who or what caused SVB’s failure – was it a group of venture capitalists who spooked depositors using social media and started the bank run? Is the Federal Reserve (Fed) to blame for raising rates too aggressively? Perhaps the fault lies with SVB for putting money into long dated bonds when rates were at record lows? Surely regulators should shoulder some responsibility for allowing banks to invest in a long-dated portfolio of bonds? And what about the Trump administration for loosening regulations on smaller banks? In reality, there was no one cause, all of these factors played a part in what became the perfect storm.

Signature bank’s issues surrounded their relationship with Cryptocurrency firms, a niche banking area which most large institutions avoid. Credit Suisse’s issues were quite different and well known within the industry. While Credit Suisse’s balance sheet and capitalisation levels were sturdy, there has long been wider worries about the bank’s profitability. Given these concerns, the hit to Credit Suisse was no surprise as in a panic-induced bloodbath, the weakest usually endure the worst injuries.

Legendary English ska band Madness reformed in 1992, six years after splitting up, and announced a comeback show in London dubbed ‘Madstock’. The gig was nearly cancelled hours before the band was due onstage after a robber stole the group’s £600,000 advance. Did he smuggle the cash out in his ‘baggy trousers’? (Sorry.)

We have minimal exposure to the banking sector within the portfolios, but the position held across core portfolios in Global Insurance has suffered on sentiment rather than a change in fundamentals. We do not foresee any systematic risk to the banking sector. In fact, the main implication for markets is around the future of interest rates. The failure of several US banks has thrown into question bets that the Fed will continue to raise rates aggressively.

Environment - April 2023

In a move that seeks to address how nations are held responsible under international law for their climate obligations, the United Nations General Assembly has adopted a resolution which will ask the International Court of Justice (ICJ) for an advisory opinion. While this advisory opinion is not domestically binding, it does carry international weight and would clarify a country’s climate obligations. Further, it could lead to financial consequences through litigation in the case of failure to meet those obligations.

The push for the UN to adopt such a measure was led by the South Pacific island nation of Vanuatu, largely as a result of a campaign by law students at Vanuatu’s University of the South Pacific. As an island that has in the past month alone suffered two powerful cyclones which led to widespread damage and left many residents in evacuation centres, the injustice between nations suffering the greatest impact of climate change and those who can hasten the move to a more sustainable future is being addressed. There now exists a means for vulnerable nations to hold other nations financially accountable.

It is likely that the potential for repercussions because of a failure to meet commitments, such as that of the Paris Agreement 2015, will see more decisive action being taken with an increased focus on the behaviour of corporate bodies – many of whom are at the forefront of climate related activity in the transition away from fossil fuels.

One of the major issues when understanding corporate behaviour is so-called ‘greenwashing’- essentially the propensity of companies to issue unsubstantiated environmental claims; selling goods labelled as green that are in fact not. The European Commission (EC) this month published a proposal, the Green Claims Directive (GCD), which aims to tackle this behaviour and reassure consumers. For specific green claims, companies across the bloc will now need to have independent verification and clear scientific evidence. The drive to intensify environmental responsibilities continues to gather pace.

The UN backed Scientific Assessment Panel has reported that the ozone layer is expected to recover to 1980s levels (prior to the formation of the ozone hole) within the next four decades following the phase out of almost 99% of ozone-depleting substances.

Increased investment will be necessary to support the transition to clean energy sources and for nations to avoid climate legislation as they progress along the net-zero path. Across portfolios, we maintain exposure to renewable energy and companies facilitating decarbonisation. The outlook for these underlying themes remains as strong as ever.

The Monthly Market Commentary (MMC) is written and researched by Simon Gibson, Richard Smith, Scott Bradshaw, Mark Moore and Lauren Wilson for clients and professional connections of Mattioli Woods and is for information purposes only. It is not intended to be an invitation to buy, or to act upon the comments made, and all investment decisions should be taken with advice, given appropriate knowledge of the investor’s circumstances. The value of investments and the income from them can fall as well as rise and investors may not get back the full amount invested. Past performance is not a guide to the future. Mattioli Woods is authorised and regulated by the Financial Conduct Authority.

The MMC will always be sent to you by the seventh working day of each month, usually sooner, is normally delivered via email, and is free of charge as the MMC is generally made available to clients who have assets under our management in excess of £200,000, and to all clients under our Discretionary Portfolio Management Service (DPM). Normally, the MMC costs £397 + VAT per annum. Professional advisers and their clients should contact us if they are interested in receiving a monthly copy.

Sources: All other sources quoted if used directly; except fund managers who will be left anonymous; otherwise, this is the work of Mattioli Woods.