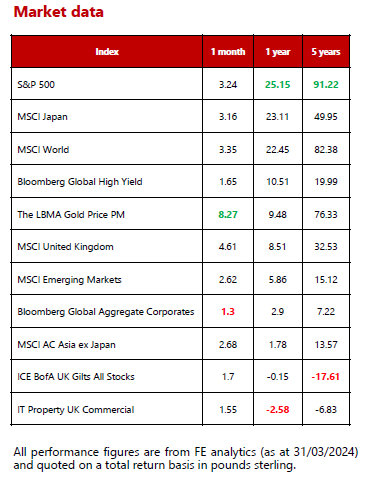

Global markets summary - April 2024

March rounded off what was generally a good quarter for equity investors with stock markets propelled by resilient data from major economies. The US continued to lead the way as its economy was confirmed to have grown by more than expected during the final quarter of 2023. Economic resilience has also been the story in most other developed economies. Europe has been helped by natural gas prices that are lower than before Russiaʼs invasion of Ukraine and the uptick in global manufacturing activity, as well as a recovery in bank lending growth. This, in combination with attractive valuations, should benefit cyclical and growth-oriented European equities. Japan is also beating expectations, both in terms of economic activity and corporate profits growth.

While equity investors extoled strong economic data, for fixed income investors it was a more challenging period. Stickier inflation prints combined with resilient economic activity have led investors to dial back expectations around the timing and scale of interest rate cuts this year. Other interest rate sensitive asset classes, such as commercial property, also suffered on the back of higher-for-longer interest rate expectations.

Overall, the first quarter of 2024 has been a rewarding one in many equity markets. That said, we are not complacent and are cognisant that there are a multitude of economic, environmental, political, and geopolitical risks lurking that could lead to volatility ahead. Given that investor sentiment and complacency levels are currently elevated, any negative headlines could be the catalyst for some profit taking and a market pullback. As such, our tone is that of cautious optimism moving into the second quarter of the year.

United Kingdom - April 2024

It was a strong month for UK equities, outperforming the broader global equity index. The inflation and interest rate narrative continues to dominate the directionality of the UK market, as is the case with most markets around the world. Towards the end of the month, the Bank of England (BoE) decided to hold rates steady at 5.25% for a fifth consecutive meeting. The breakdown of the votes signalled to the market that rate increases seem unlikely at this point and cuts could be coming soon.

The confidence of the central bank is helped by improved data, with inflation reportedly decelerating to 3.4%. This marks the lowest rate for two years. At this point in the cycle, slowing inflation can often be indicative of an economic slowdown. Pleasingly, data from the servicing and manufacturing sectors suggested that output has been expanding. Equally, the release of Januaryʼs GDP number showed 0.2% growth, which brings the UK out of the technical recession entered towards the end of 2023.

The combination of better-than-expected growth and falling inflation was helpful for the UK market, which continues to trade on a low valuation. Bridging the valuation gap to other markets is something that was on the agenda for the Chancellor, who delivered the Spring Budget earlier this month. The Budget was relatively uneventful and there was not a great deal that moved individual equities or sectors. At a headline level, the proposed introduction of a British ISA, which would provide an additional £5,000 ISA allowance to invest in British companies, is an interesting move. The logic behind it is sound, with UK equity ownership having been in decline for some time.

While the British ISA is not going to move the dial on day one, it could help towards improving sentiment and reminding investors there is a plethora of opportunities listed in the UK. We made no changes to our allocations this month.

North America - April 2024

US equities continued to perform well in March supported by some well-received corporate earnings as well as ongoing economic resilience. Last year, we wrote at length about the US equity marketʼs ‘bad breadthʼ as we saw only a handful of companies generating the lionʼs share of index gains. This year however, there is evidence of a broadening out in the market. Over March, the S&P 500 index delivered 3.32% with an equal-weighted version of the index delivering 4.54%. This is in marked contrast to 2023, where an equal-weighted version of the index lagged, delivering 6.79% for the calendar year, versus 18.58%.

The above figures show that a variety of sectors, including miners, energy, and industrials, all outperformed technology sectors over March, meaning investors are finally looking for opportunities outside of the much-lauded sector. Such a broad-based rally across most stocks in a particular index is generally viewed as a positive sign by investors as evidence that momentum is widespread across most business sectors and therefore sustainable.

Although expectations for interest rate cuts are continually pushed out (with the probability of a first rate cut in June now a 50/50 bet) the economic potential remains strong in the US, at least over the medium term. The Biden administration appears prepared to pull out all the stops to keep the economy running smoothly ahead of Novemberʼs presidential election. While getting policy through Congress looks improbable, the incumbent government can deliver tax cuts, forgive student loans, utilise liquidity from the Treasury, and even attempt to curtail rising petrol prices by using the Strategic Petroleum Reserve.

Within our core portfolios, we maintain a chunky allocation to US equities. Over March, we added a value-orientated US position looking to take advantage of the hidden value and upside potential in areas we believe are overlooked by the market given that we are finally seeing signs of the market leadership broaden and less fixation on the few technology stocks that drove markets over 2023.

Europe - April 2024

European markets also had a strong month with the Euro STOXX delivering 4.51% over March (in £ terms), leading the index to deliver 8.69% for the quarter. The information technology sector outperformed amid ongoing enthusiasm over demand for AI-related technologies. Improvements in the economic outlook boosted more economically sensitive stocks across a variety of sectors including financials, consumer discretionary and industrials, while banks were supported by some announcements of improvements to shareholder returns. In contrast, areas viewed as more defensive, namely utilities, consumer staples and real estate, were the main laggards.

The region has benefited from improving consumer confidence due to the mild winter and a rise in real wages due to falling inflation and a tight labour market. European consumers also have pent up savings thanks to the expectation of a severe energy crisis that did not materialise. Over the period, there were signs of improving business activity in the eurozone. The flash eurozone Purchasing Managersʼ Index (PMI) rose to 49.9 in March compared to 49.2 in February. This signals that business activity is almost at stable levels. Investors expect a rebound in manufacturing, which has now bottomed out and looks to be approaching recovery mode as we near a rate-cutting cycle in the developed world. We also see a pattern of consumers switching their spending back to goods from services, benefiting manufacturing-heavy regions like Germany and France.

We have recently closed our underweight to Europe given the potential tailwinds for the region. European equities still look attractively valued especially when compared with US peers. The price-to- earnings (P/E) ratio for the MSCI US index is, at time of writing, 21x earnings, whereas the MSCI Europe index is trading at 15x earnings, indicating a relative discount.

Rest of the world - April 2024

The momentum around Japanese equities also persisted over March, despite Japan beginning the normalisation of its monetary policy. The Bank of Japan (BoJ) ended eight years of negative interest rates by raising short-term rates for the first time in 17 years to a new target rate between the 0-0.1% range. The impact of this move on financial markets has been a weaker yen compared to other major currencies, supporting major large cap businesses that generate a significant proportion of their revenues outside of Japan. Although we took some profit from our position in Japanese equities over March given its stellar performance, we maintain a positive view of the region in light of its solid fundamental picture, which includes competitive earnings growth.

Although most markets ended the month in positive territory, Asia/emerging market (EM) equities underperformed developed markets (DM) over March. This is a continuation of the trend we have seen over the past 18 months as investors continue to question Chinaʼs growth prospects in the absence of any meaningful fiscal stimulus.

The MSCI China Index, nevertheless, rebounded from its January low on the back of better economic activity data during the Lunar New Year holiday and some easing measures from the Peopleʼs Bank of China. The stimulus measures so far have been piecemeal, but the Governmentʼs 5% GDP growth target for 2024 suggests more meaningful policy moves will be forthcoming. However, the property market problems are far from resolved and the consumer price index is in deflation; as such, we remain cautious on the region and believe that this recent rally may not be sustainable.

Indian stocks outperformed peers in March with investors hopeful that the political stability that has unpinned Indiaʼs recent stock market growth will continue if Narendra Modi wins a third electoral victory this year. India has also benefited from an improving physical and digital infrastructure, which has encouraged overseas investment in manufacturing as companies seek to diversify supply chains outside of China.

Broadly speaking, Asia and emerging market equities are expected to catch up to the rest of the world when DM countries begin their monetary easing cycle, which should result in a weaker US dollar. This in turn would lower the value of dollar-denominated liabilities and higher foreign direct investment. However, with the continued resilience of DM economies and sticky inflation prints pushing out interest rate cuts, as well as heightened geopolitical risk supporting the US dollar, we remain tactically tilted towards DM equities.

We maintain a measured exposure to emerging markets, given the long-term growth potential. From a fundamental viewpoint, valuations in broad Asia/EM remain compelling with earnings per share (EPS) growth expected to beat DM equities over the medium to long term given the overall lower base from which they are starting. We believe selectivity is essential as certain areas are poised to outperform, for instance, Korea and Taiwan are both benefiting from the recovery in the manufacturing cycle.

Fixed income - April 2024

While March was an ebullient month for equity investors, bond markets appear a little more circumspect. At the start of 2024, bond markets were pricing in six rate cuts in the US and eurozone, and seven rate cuts in the UK. At the end of the first quarter, expectations across the US, UK and eurozone shifted meaningfully to just three cuts, as markets have priced out anything other than the most featherlight of landings in the US and shallow recession in the eurozone and UK. While central bank officials have all but confirmed that interest rates have peaked, they maintain a cautious tone around the timing and scale of any interest rate cuts. Inflation remains a central concern for markets, and despite indications of dampening inflationary pressures, unexpected high inflation readings from the US tempered enthusiasm for imminent rate cuts. Currently, markets are not putting much weight on the possibility of adverse economic scenarios. Therefore, although it is not our base case, if developed market economies slow or slip into recession, we expect central banks to cut interest rates more aggressively than what is currently priced into forward curves.

Over March, corporate bonds outperformed government bonds thanks to easier financial conditions and global economic activity on the upswing. High yield was once again the strongest credit sub-sector thanks to its lower interest rate sensitivity. Economic resilience and a healthy underlying growth outlook should keep corporate defaults low, although we maintain that credit selection is vital as refinancing risk increases the longer interest rates stay high.

There were no changes to fixed income allocations within core portfolios over the period. We maintain a healthy allocation to the asset class, in line with risk appetite, via a broad spread of government debt, investment grade and high-yield credit and emerging market debt. Overall, we believe that fixed income markets are priced more fairly today than at the end of 2023 and appear well placed to act as a buffer within portfolios in the event of an adverse growth shock.

Ask us anything - April 2024

Q: Is the Japanese stock market now in ‘bubbleʼ territory?

A: Over the year so far, the Japanese stock market has delivered solid returns. The region made headlines in February, with the Nikkei 225 finally exceeding the bubble-era high last seen in December 1989. Naturally, this has investors feeling a little twitchy that history is about to repeat itself.

Firstly, it makes sense to look at the cause of stock market strength and analyse its sustainability. Money has flowed into Japanese stocks for a variety of reasons including improved governance standards and increasing demand from foreign investors (primarily thanks to an urge to pivot away from Chinaʼs markets). We have also seen an influx of investment by domestic households taking advantage of a new government-subsidised savings scheme.

Corporate governance reforms, led by the Tokyo Stock Exchange, have continued and should not be understated. As a result, Japanese companies are continuing to restructure in reaction to guidelines, resulting in a better use of balance sheets and a reduction of cross holdings, as well as triggering a raft of share buybacks, all of which are enhancing shareholder returns. As these changes are ongoing and in their infancy, our view is that corporate reforms will continue to drive Japanese stock market returns over the medium term.

The performance of domestically oriented companies has been notable, with many companies showing signs of regaining pricing power, which should not be underestimated following years of deflation. When coupled with improved consumer purchasing power through wage increases, this should generate healthy levels of corporate earnings growth. We can expect some of these higher profits to then be recycled back into Japanʼs economy through further wage increases, propelling a positive cycle of broader economic progress that has been largely absent from Japan for a generation.

That said, we believe some caution over the short term is warranted given the speed and nature of the recent rally. The rally of Japanese stocks has been centred on large caps (although not to the extent the US market has been concentrated on the ‘Magnificent Sevenʼ), leading to valuations of many of these companies, particularly those in the Nikkei 225 index, becoming somewhat stretched. We have taken some profit from this area and focus on remaining selective in terms of what we own within the region.

We remain positive on the region and retain a measured standalone allocation here given tailwinds such as improved corporate governance and world-beating niche manufacturing businesses, particularly in technology and robotics.

If there is a question you would like to pose to our team, please reply to this email or write to [email protected]

The Monthly Market Commentary (MMC) is written and researched by Scott Bradshaw, Lauren Hyslop and Jonathon Marchant for clients and professional connections of Mattioli Woods and is for information purposes only. It is not intended to be an invitation to buy, or to act upon the comments made, and all investment decisions should be taken with advice, given appropriate knowledge of the investorʼs circumstances. The value of investments and the income from them can fall as well as rise and investors may not get back the full amount invested. Past performance is not a guide to the future.

Mattioli Woods is authorised and regulated by the Financial Conduct Authority.

Sources: All other sources quoted if used directly; except fund managers who will be left anonymous; otherwise, this is the work of Mattioli Woods.