Global markets summary

March 2025 saw global investment markets experience notable volatility, primarily influenced by escalating trade tensions and economic uncertainties. The US stock market faced significant downturns due to apprehensions surrounding new tariffs announced by the Trump administration. European markets mirrored the US downturn, with significant declines across major indices as concerns over the potential impact of US tariffs on European exports led to increased market volatility. Asian markets were not immune to the global sell-off either, with Japan’s Nikkei index dropping by 4%, reflecting investor anxiety over trade tensions. Fixed interest markets too were mixed over the month, with only US Treasuries delivering a positive return to investors. Despite a flight to safe haven assets such as UK gilts and investment grade corporate bonds, rising yields led to a consequential fall in capital values and ultimately returns were below par, albeit nowhere near the falls seen in equity markets.

While this piece covers markets over March 2025, it would be remiss not to mention the market turbulence triggered by President Trump’s “Liberation Day” tariff announcements on 2 April. Although there had been plenty of hype ahead of the date, it was clear that most investors were expecting that the President’s bark would prove worse than his bite. Yet, what was delivered was a complex array of tariffs at various rates on a global basis, which, if maintained, are expected to significantly impact the global economy, potentially raising US inflation and reducing growth. With no last-minute reprieve from the Trump administration, the tariffs came into force at midnight in Washington on Wednesday 9 April. They include a 104% levy on China that will diminish trade between the world’s two largest economies. In response, equity markets around the world have sold off sharply.

We understand that such market events can be unsettling but would urge you to remain calm in the face of volatility and avoid making reactionary decisions. We know from many psychological studies that loss aversion is a powerful emotion, and the temptation when markets fall can often be to sell and avoid further losses. However, history tells us this is often the wrong course of action and that, with a long-term view, time in the market is more meaningful than timing the market. It is also important to note that the Mattioli Woods multi-asset solutions are designed to offer greater protection than equity markets via diversification, risk management and the flexibility to adjust the asset mix in response to changing market conditions.

We’ve written more about this in the ‘Ask us anything’ section and are here for you during this turbulent period to provide guidance.

United Kingdom

Despite a more challenging March, UK equities remain in positive territory for the year, both in absolute terms and relative to the broader global equity index. The significant uncertainty that has been caused by President Trump has led investors to appraise options elsewhere. In March, the Bank of America’s Global Fund Manager Survey highlighted the biggest rotation out of US equities on record. Beneficiaries from the rotation include UK equities, as investors seek more attractively-valued options around the world.

It remains to be seen whether the flows into the UK will be a passing shower or a monsoon. However, it is clear that the UK has endured a persistent drought, with domestic equity funds having registered net outflows in all but one of the past 45 months. The recent shift is a clear positive but at present, asset allocators appear to be parking their money in large-cap stocks, either through passive funds or derivatives. This helps to explain the material underperformance of small- and mid-cap stocks that we have witnessed since the turn of the year. With time, we hope to see this flow down the market cap spectrum.

While we wait for this to happen, we continue to see marginal positives in the data. Inflation, economic activity, consumer confidence and retail sales all came in better than expected during March, indicating that things may be improving.

The Spring Budget was expected to be the main market event during the month, though in stark contrast to the Autumn Budget, there was very little speculation around potential outcomes. Overall, the Spring Budget was a non-event for markets, with very little positive or negative news. Rachel Reeves restored her budget headroom through a number of spending cuts, predominantly to welfare, and managed to avoid tax increases. Alongside restoring headroom, the Government also increased defence spending to 2.5% of GDP, funded through cuts to foreign aid.

The Budget, together with recent data, gives the Bank of England little reason to hold interest rates in May’s meeting. However, the inflationary pressure that tariffs may bring will likely ensure a cautious stance is retained.

We commented last month and the month prior that large-cap stocks had dramatically outperformed mid-cap stocks. The trend continued in March and large-cap stocks are now more than 10% ahead of mid-caps year to date. Like most active managers, we have an overweight to the latter in our UK Dynamic Fund, seeing more attractive valuations and higher earnings growth prospects. While it has been a frustrating start to the year, we are optimistic around the prospects for these businesses.

North America

March rounded off a challenging quarter for US equity markets. The S&P 500 declined by 5.67% over the month in $US terms, although this was exacerbated for the sterling investor due to a weaker dollar, marking its worst quarterly performance since 2022. The Nasdaq Composite experienced an even steeper drop of 10.39% in £ terms as concerns over the valuations of technology stocks like Tesla and NVIDIA led to a sell-off here. Conversely, the energy sector in the US recorded a 9.3% increase, and financial stocks provided some support to the S&P 500’s performance.

The events of the first quarter have swiftly been overshadowed by President Trump’s “Liberation Day” tariffs and their sweeping impact on investment markets. Sentiment around government policy has undergone a violent shift, negatively impacting US equity market returns. The S&P 500 sold off sharply on Tuesday 8 April, as investor hopes faded for any imminent delays or concessions on tariffs ahead of a midnight deadline. The S&P 500 has endured its steepest four days of losses since the index was created in the 1950s, losing $5.83 trillion in market value.

Looking past the noise to the economic and market implications, the tension between slower economic growth and higher inflation is likely to grow over coming months. In recent meetings, the Federal Reserve (Fed) has signalled a lean towards growth implications over inflation, i.e. tariff policies likely increase the scope for US interest rate cuts this year. Reflecting this, the market’s expectations for the number of US rate cuts this year moved from 3 reductions of 25bps each to 3.3 reductions.

The global disinflation trend of the last two years has paused, with an increasing number of countries seeing upward revisions to inflation expectations. The US could experience a new inflation scare, driven by aggressive import tariffs. While a near-term inflationary spike is broadly expected in response should the tariffs remain in place, in our view, concerns of sustained stagflation (the term for persistent high inflation combined with high unemployment and stagnant demand) are likely overblown. Stagflation requires a sustained inflation-wage spiral, which last happened in the US when we saw an energy shock meeting a more unionised workforce. Our central case is that, over time, the envisioned supply shock will be managed as countries negotiate and/or supply chains migrate. Furthermore, as companies continue to integrate artificial intelligence into processes due to its ability to automate routine tasks and potentially replace workers in fields where these tasks are prevalent, workforce wage increases will likely remain constrained.

Over the latter half of 2024, we proactively moved our US equity exposure from passive to actively-managed funds given concerns around market concentration and frothy valuations. We believe this puts our portfolios in a better position to navigate current turmoil. While our US equity exposure is not immune to market conditions, the underlying fund management teams will proactively sift through market dislocations brought about by the current volatility to identify companies with attractive fundamentals that may have been mispriced in the market turbulence.

Europe

European equities ended their broad winning streak in March with the EURO STOXX returning -1.62% over the month. Underlying performance was mixed, as the technology sector showed resilience with several companies reporting strong earnings, while energy stocks were volatile, influenced by fluctuating oil prices and geopolitical tensions. Over the month, the announcement that Germany put forward a plan for a €500 billion special purpose vehicle for infrastructure investment over the next decade, an exemption from the debt brake for defence spending above 1% of GDP and an increase in borrowing limits for states from zero to 0.35% of GDP was seen as a shining light amid the global uncertainty.

Over April so far, the EURO STOXX index has lost 6.33% following the Trump administration’s tariff announcements. The automotive sector bore the brunt of the pain as tariffs on car exports led to substantial drops in stock prices for major manufacturers. Companies in the steel and aluminium industries have also endured pain as the tariffs on these materials could cause a substantial hit to earnings. In response, rather than fan the flames, the European Union has sought to cool tensions, with bloc chief Ursula von der Leyen warning against worsening the trade conflict in a call with Chinese premier Li Qiang. She stressed stability for the world’s economy, alongside “the need to avoid further escalation”, according to an EU readout.

We maintain a neutral stance towards European equities, preferring to access the region via actively-managed funds that are well placed to manage current market volatility and take advantage of opportunities.

Rest of the world

Over March, Asia Pacific and broad emerging markets reflected the sombre mood of investors with the MSCI Asia Pacific index returning -2.89%. The MSCI China was the ‘best’ performing market but still ended the month down, returning -0.52%. Japan’s equity market also faced selling pressure, driven by uncertainty surrounding US tariff policies. These fears were exacerbated by an announcement towards the end of March that the Trump administration would impose 25% tariffs on imported cars. As a result, exporters and technology-related stocks were among the most heavily affected.

The global market rout only deepened further as the Trump administration’s tariffs were revealed to be more severe than most investors anticipated. “Liberation Day” marks a seismic shift away from ‘globalisation’ and, unless there is massive back tracking, the policy will spark the reorganisation of global supply chains that have flourished since the 1970s. China has been hardest hit by the tariffs but has shown no signs of backing down, vowing to fight a trade war “to the end” and promising countermeasures to defend its interests. China’s retaliatory tariffs of 34% on US goods are due to come into force on Thursday 10 April.

It is key to note that this is a manufactured situation and remains fluid, with the future actions of the Trump administration remaining largely unknown. On Tuesday 8 April, President Trump stated that his government is working on “tailored deals” with trading partners, with the White House saying it would prioritise allies like Japan and South Korea. His top trade official Jamieson Greer also told the Senate that Argentina, Vietnam, and Israel were among those who had offered to reduce their tariffs.

Japan’s equity market has not gone unscathed, and although net exports represent 10% of GDP only, the stock market exposure to larger non-Yen sales represents 45% of the overall market’s sales. Unsurprisingly, defensive sectors have performed relatively well while bank share prices have fallen on fears of no interest rate hikes. While Japan’s stock market will not be immune to a global growth shock, it is in a comparatively strong position given that the Japanese economy is not hugely reliant on net exports (exports are only 10% of GDP while consumption accounts for 55% of GDP) and total tariffs relating to Japanese US exports are Y7 trillion or 1.2% of GDP. We also think it is likely that Japan could see its tariffs reduced, given the desire in Washington to maintain a close relationship with Tokyo, and considering Japan’s strategic importance to the US, as it faces up to China.

We maintain a neutral stance to broad Asia Pacific and emerging market equities, accessing these markets via actively-managed funds within our core portfolios. In addition, we retain a targeted positioning in Japanese equities, believing that there are quality companies located in the region that are well placed to weather the current storm.

Fixed income

Despite a flight to safe haven assets over March, only US Treasuries delivered a positive return to investors. Rising yields led to a consequential fall in capital values and ultimately below par returns, albeit nowhere near the falls seen in equity markets. The yield on 10-year gilts fluctuated, starting the month at around 4.48% and rising to approximately 4.65% by the end of March. This increase was driven by investor concerns over fiscal policies and inflation.

Global bond markets have experienced significant movements since the announcement of new tariffs. Bond yields have generally spiked, with the yield on the 10-year US Treasury hitting its highest level since late February, reaching 4.51%. As the tariffs have introduced considerable volatility into the bond markets, investors are seeking safe havens, leading to increased demand for government debt, which in turn pushes up bond yields.

Spreads in corporate debt widened in sympathy with other risk assets, though price action was more muted relative to equities. As you may know, a wider credit spread indicates that investors require a higher risk premium to compensate for the increased perceived risk of the corporate bond. As such, credit spreads tend to widen during periods of economic uncertainty or market volatility, as investors become more risk averse. Now, the main question for credit investors is whether a growth slowdown could morph into a recession and, in this case, a default cycle. In our view, investment grade credit looks relatively well placed with balance sheets remaining robust while we feel less confident about the more leveraged and lower quality part of the credit market.

Over the past few months, we have increased the credit quality within the bond sleeve of core portfolios as part of a broader move towards defensive positioning. Our preference for short duration (i.e. bonds less sensitive to interest rate movements) has also been well rewarded as yields have pushed upwards.

Ask us anything

Over the past week, we have had an influx of concerns relating to the impact of President Trump’s tariffs. Below, we have sought to answer the majority of these questions, which largely relate to our views on the impact, whether now is a good time to buy or sell, and concerns around market falls.

We understand that these developments have sparked significant uncertainty for investors and would like to remind you that we are here to help during this period. Please do not hesitate to get in touch with your consultant or a member of the Investments team if you need any further guidance.

Keep calm and carry on

Trump’s “Liberation Day” has been a horrific surprise. While some tariffs were expected, the magnitude and sweeping nature has seen markets pull back rapidly. Expectations have swung, and now the chance of a recession has increased dramatically. Certainly, we can class what we are currently experiencing as an economic shock.

Economic shocks happen and are undoubtedly unpleasant, but volatility is a risk of equity investing. We know from many psychological studies that loss aversion is a powerful emotion, and the temptation when markets fall can often be to sell and avoid further losses. Our investment experience tells us that is often the wrong course of action and time in the market is more meaningful than timing the market. For medium- to long-term investment horizons, staying invested is important.

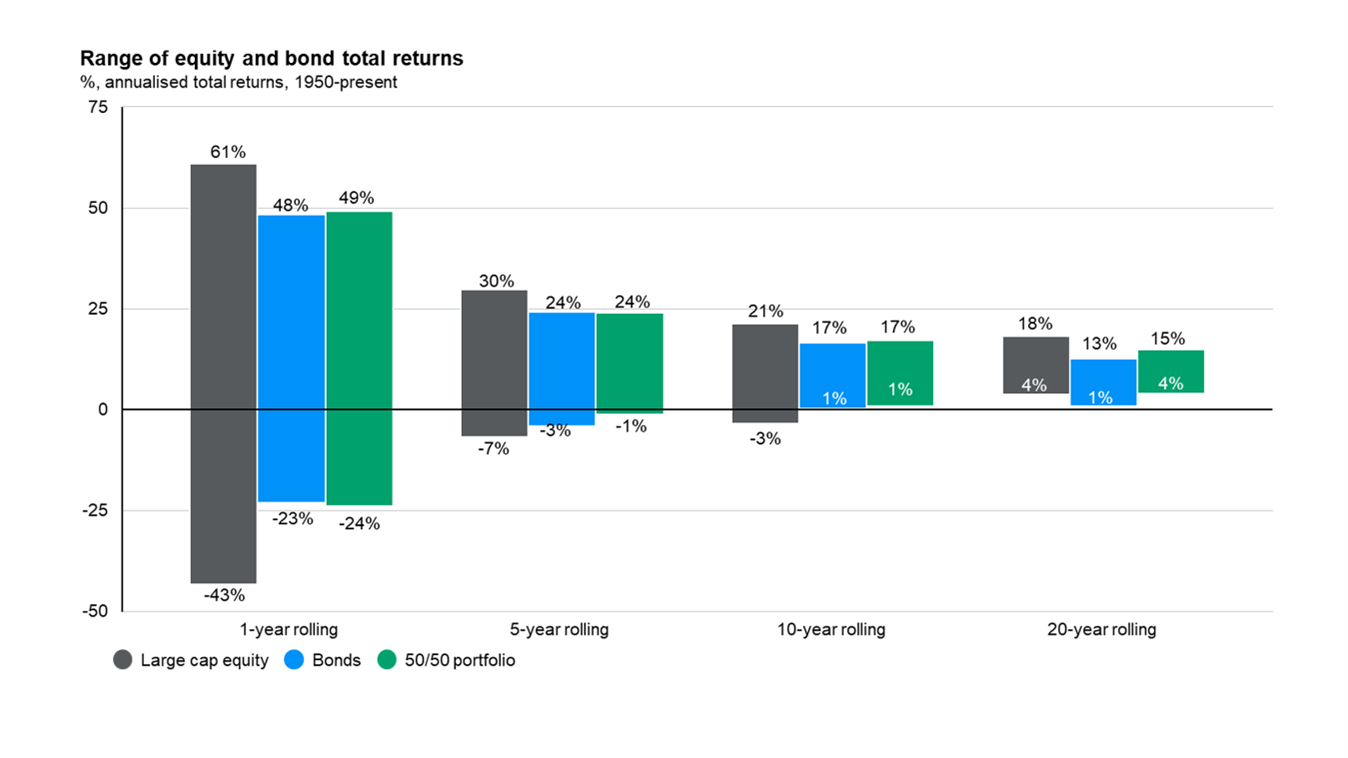

Chart 1

Long-term US asset class returns by holding period

Going back to 1950, the range of investment returns over a one-year period has been fairly wide. Equities (as by the S&P 500) and bonds have both had exceptionally strong and exceptionally poor years. Looking further to the right, over longer periods this smooths out, and over five-year periods, equities have tended to deliver positive returns. The chart also shows the benefit of diversification, with adding bonds to the portfolios reducing drawdowns over time.

Source: JPM Guide to the Markets (UK) as at 31/03/2025

Even longer term, data from First Trust (1937-2024), suggests for a S&P 500 investor, there is a 53.3% chance of positive returns over one day, 63.0% over one month and 77.3% over a year. This gets even more positive over a longer investment horizon, increasing to 87.9% over five years and 97.4% over ten years.

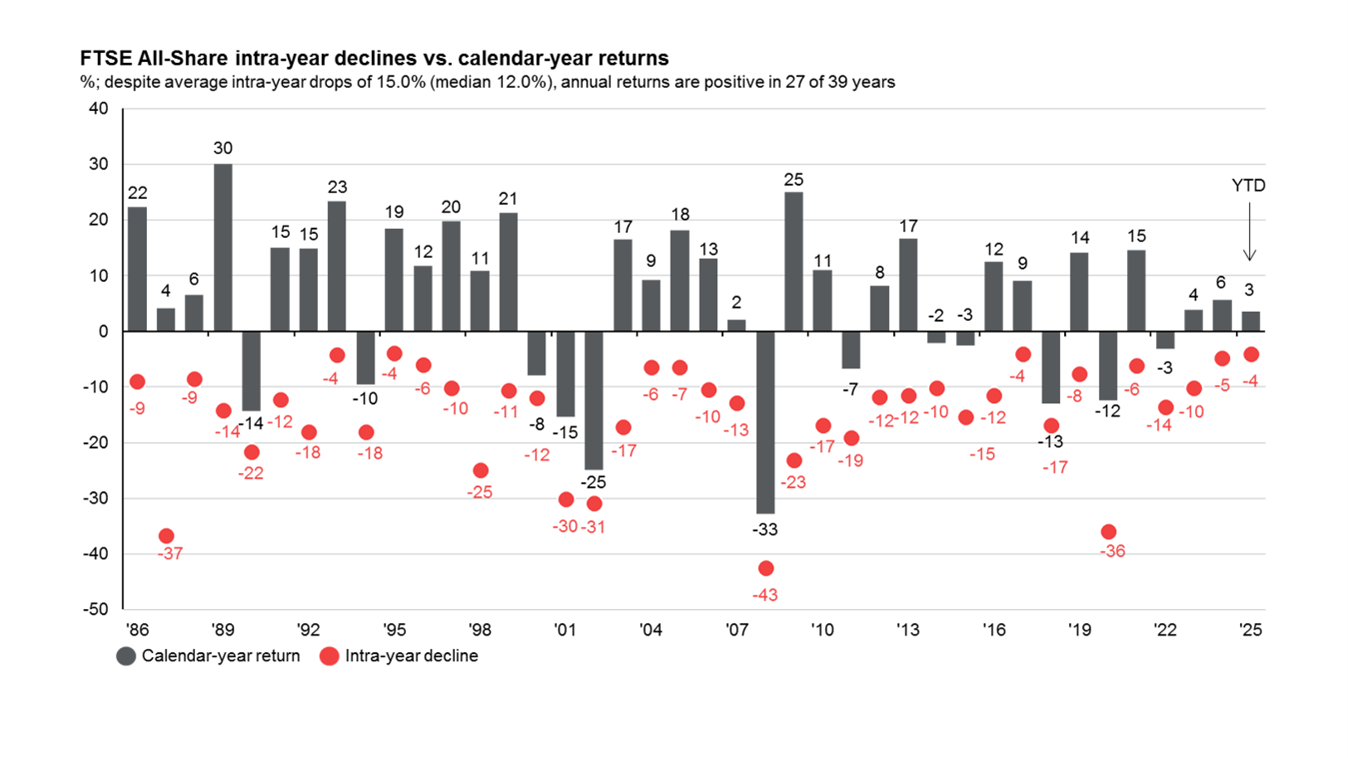

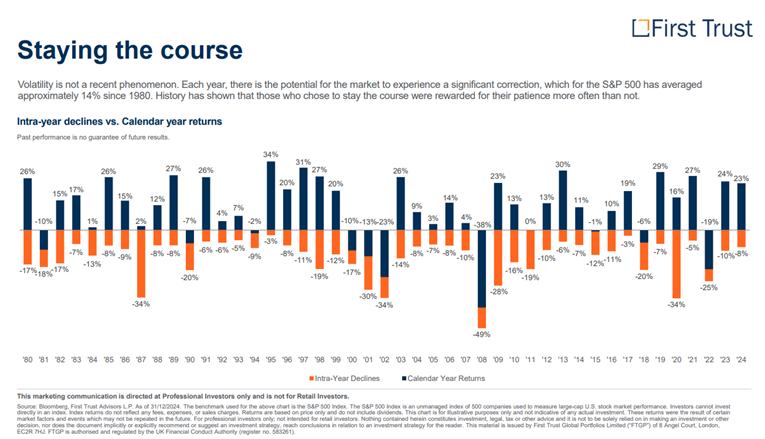

Chart(s) 2

Intra-year drawdowns are the norm

It is also not unusual to see drawdowns in markets in a year and still result in a positive year. The below charts show the drawdowns in both the main UK stock market, where there have been average 15% drops, and the main US stock market, where the average decline has been 14%, but staying invested has led to positive returns overtime.

Source: JPM Guide to the Markets (UK) as at 31/03/2025

Source: JPM Guide to the Markets (UK) as at 31/03/2025

Source: First Trust Client Resources Kit – Markets in perspective – as at 31/12/2024

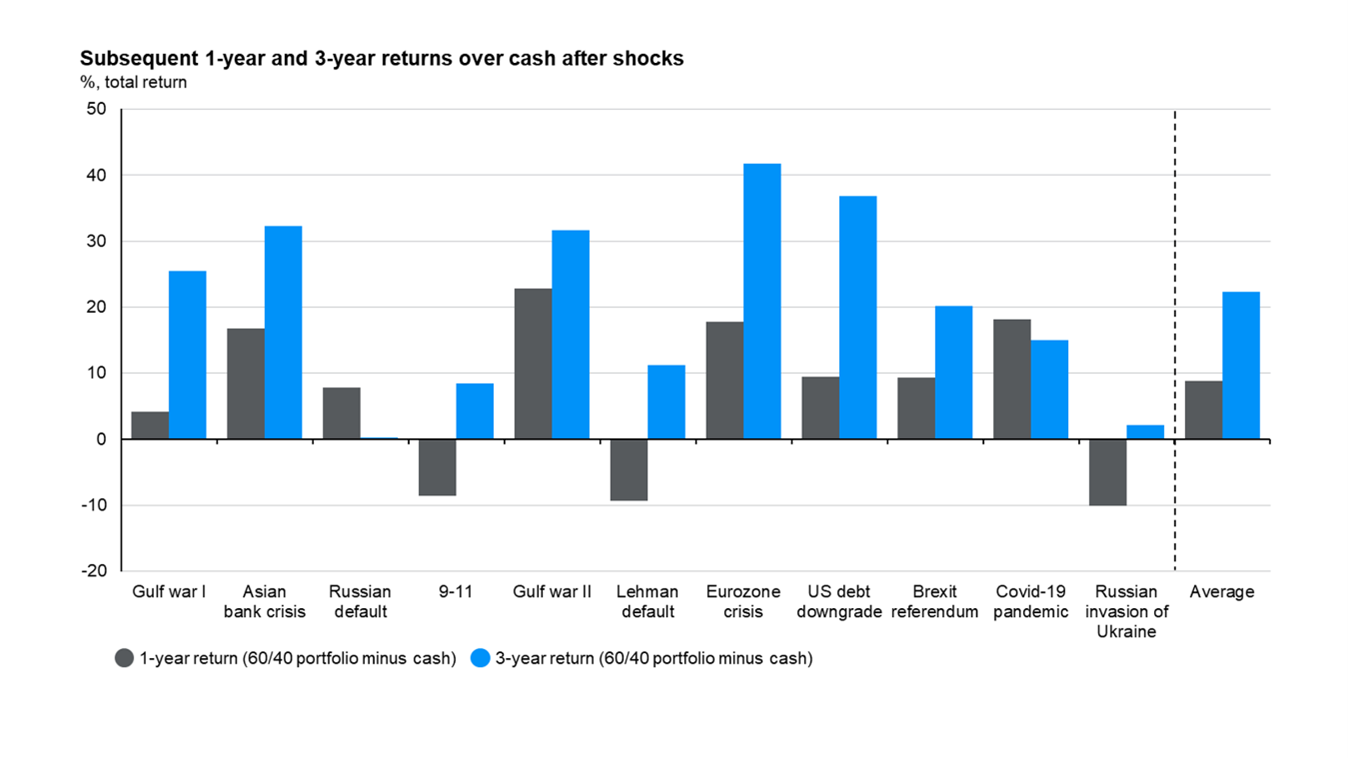

Chart 3

Markets after shocks

But what about extraordinary years, where there are market shocks? The below shows the return of a 60% S&P 500 and 40% 10-year US Treasury portfolio, over one year and three years after major shocks.

Source: JPM Guide to the Markets (UK) as at 31/03/2025

The Russian default/Russian Flu Crisis of 1998 occurred just before the Tech Crisis in 2000, which has impacted on the three-year figure.

With most of the shocks above, portfolios had recovered just a year later and had posted strong returns over three years. There is a saying from value investor Benjamin Graham: “In the short run, the market is a voting machine but in the long term, it is a weighing machine”. Initially, markets can overreact to negative news and shocks, as swayed by sentiment, emotion and the herd mentality of others selling; investors ‘vote’ with their money and markets can sell off more than fundamentals justify. Over the longer term, it is the (weighing of) earnings of the underlying companies that will ultimately determine equity returns.

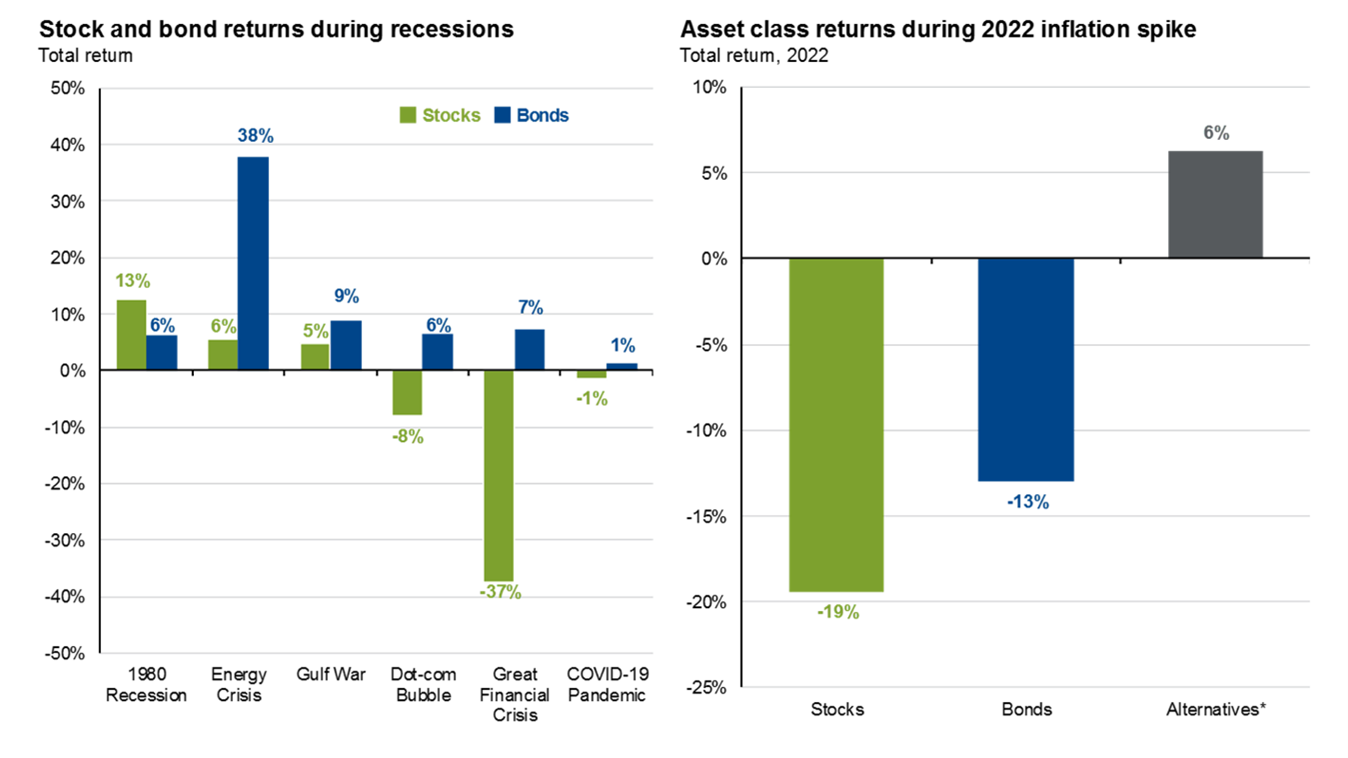

Chart 4

Diversification by asset class (and the case of 2022)

Those with keen eyes on Chart 3 will see it was for a portfolio, not just equities. Diversification remains a powerful tool and as inventor of modern portfolio theory Harry Markowitz is credited as saying, “diversification is the only free lunch in investing”.

Equity markets often grab the headlines, particularly when there are big moves, but they are not the only part in portfolios. The below JPM United States Guide to the markets chart shows the return of asset classes during recessions (S&P 500, US 10-year Treasury). Traditionally, fixed income assets are negatively correlated with equities, meaning these two asset classes tend to move in opposite directions. This relationship helps multi-asset portfolios weather various economic shocks, as generally bonds act as a ballast.

Source: JPM Guide to the Markets (US edition) as at 31/03/2025

But what about 2022?

There can be periods where the correlation relationship breaks. The most recent example was 2022, when a spike in inflation caused by the start of the Russia/Ukraine conflict caused interest to be hiked, leading to negative fixed income returns at the same time equity markets fell on lower growth expectations. This is exceptionally rare, and this was the first calendar year since 1977 when both experienced negative returns (and only the fourth time in the last 100 years). The year 2023 saw this change back to normal. Looking over a two-year period, bond/equity correlation over the last twenty years has been negative.

These periods can demonstrate the value of alternatives to add further diversification, with gold a notable strong performer in 2022.

Chart 5

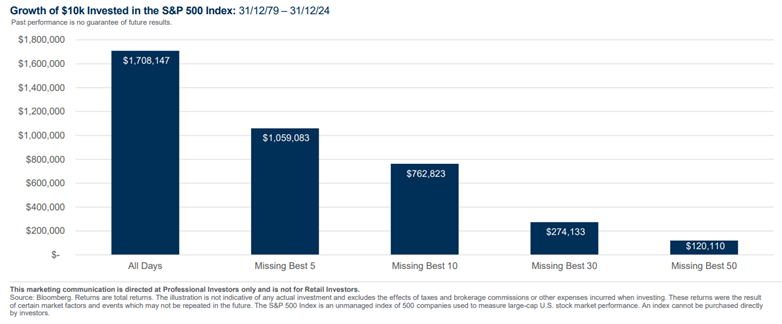

What about timing the market?

We often state that investing is a mix of art and science and on that spectrum, day trading is firmly in the art end with an element of luck. No investor has a crystal ball, and it is impossible to predict when bad days will happen – particularly those resulting from economic shocks, which by their nature are often unexpected.

Getting this call wrong can result in the missing of the best days’ return (which often closely follow the worst days). The below chart from First Trust shows the dramatic impact of missing the best days compared to staying invested, using the S&P 500 index from the start of 1980 to the end of 2024.

Source: First Trust Client Resources Kit – Markets in perspective – as at 31/12/2024

Investors are generally rewarded for sticking with their investment plans and staying invested over time.

Key takeaways

Investing in equities involves taking risk that a client needs to be comfortable with.

- Shocks and drawdowns happen to equity markets but staying invested is usually the best course of action, with equity markets delivering positive returns over the long term.

- Trying to time the market is nearly impossible to do reliably and can result in missing out on longer-term returns.

- Diversification for portfolios remains a key tool in protecting portfolios.

If there is a question you’d like to pose to our team, please reply to the email you received or write to investments@mattioliwoods.com.

The Monthly Market Commentary (MMC) is written and researched by Scott Bradshaw, Lauren Hyslop and Jonathon Marchant for clients and professional connections of Mattioli Woods and is for information purposes only. It is not intended to be an invitation to buy, or to act upon the comments made, and all investment decisions should be taken with advice, given appropriate knowledge of the investorʼs circumstances. The value of investments and the income from them can fall as well as rise and investors may not get back the full amount invested. Past performance is not a guide to the future.

Mattioli Woods Limited is authorised and regulated by the Financial Conduct Authority.

Sources: All other sources quoted if used directly, except fund managers who will be left anonymous; otherwise, this is the work of Mattioli Woods.