United Kingdom - August 2022

With our theme of extreme weather events, we are admittedly riding on the back of, well, just that here in the UK – new record temperatures, brown lawns and hosepipe bans … once again, we find ourselves reflecting the 1970s. As we prepare to publish, we also have the latest Bank of England Monetary Policy Committee decision on interest rates. Not quite the 1970s in that respect, although it is the spectre of inflation that is driving the MPC’s current thinking. The rise of 0.5%, taking the base rate from 1.25% to 1.75%, had come to be expected in recent weeks; however, interest rates at current levels felt almost unthinkable at the start of the year.

Here is a direct quote from the Bank of England, issued on Thursday, 4 August 2022: ‘The main way we can bring inflation down is to increase interest rates. Higher interest rates make it more expensive for people to borrow money and encourage them to save. That means that, overall, they will tend to spend less. If people on the whole spend less on goods and services, prices will tend to rise more slowly. That lowers the rate of inflation.’

The problem the Bank has (actually, a few problems) are as follows: first, yes, higher rates tend to reduce borrowing – but we already have a cost of living squeeze thanks to near double digit inflation. Next, rates remain historically low, and while these increases (from 0.1% in December 2021 remember) are significant, many will see them as affordable.

Third, if consumers do indeed spend less, this will impact margins and put more pressure on businesses, in turn making it less likely that wages will rise, meaning the consumers who are also at work (most of them) will be under even more pressure financially. This might look like the perfect recipe to bring inflation down, but with energy forming such a large part of the current read for UK inflation, it will take months to have an impact.

Finally, if the Bank succeeds in knocking inflation off course, but helps to create a deep and painful recession (they acknowledge at least the recession part of that line is here/coming), we go back to rate cutting to stave off even worse news … but will rates have become high enough to have an impact?

We acknowledge this is a gloomy prognosis – there is no getting away from that. We can still find things we like to invest in; they just need more finding and are fewer right now.

Back to the weather (analogies, anyway) – have we seen the stormiest period for equities, in the traditionally lighter trading summer months (though August has barely started), or can we expect or at least anticipate worse to come? ‘Equities’ is of course too broad a reference – it is not as if they all work in the same way all the time, after all. The same with weather – even in an island as ‘small’ as ours, the difference north to south and east to west can be vast … and so it is at the moment with equity markets.

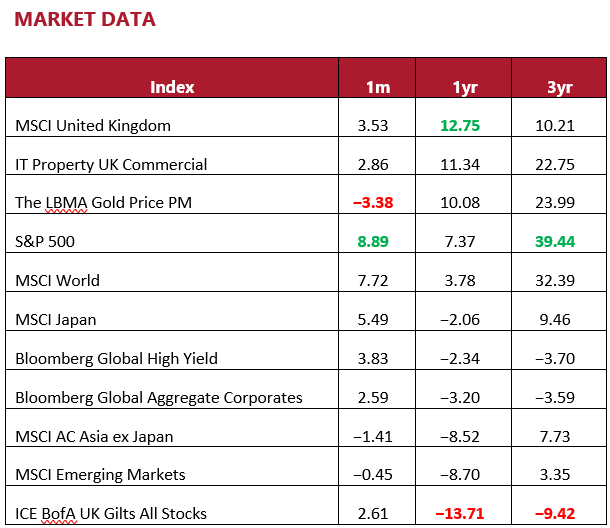

The main UK index has performed well (though within that smaller companies much less so) – and as can be seen from the Market Data table later, much better than not only emerging markets but also most other developed markets. The reasons for this are well versed, and yet the Bank of England Governor is warning about far worse economic conditions here than in many other developed or even emerging economies in the next year or so. Once again, we remind readers that GDP (economic growth, or indeed recession), while not unimportant, is not vital for stock market growth (neither indeed does a strong economy guarantee a positive local stock market – see China).

North America - August 2022

This is a crucial quarter for US equities as the reporting season enters full swing. As we discuss later in this month’s edition, one of the headwinds for corporate earnings is the strong dollar as overseas earnings are going to have been reduced in dollar terms given how strong the greenback has been. Indeed, the extent to which this is reflected in this reporting season is unknown and probably will not portray the overall impact given the inevitable time delays involved.

When we do get a pivot from the Federal Reserve, and the likely consequent softening of the dollar, this currency headwind should turn into a tailwind. Corporate earnings are actually in reasonable shape once we strip out the currency impact, and when global equities recover, the US could be exceptionally well placed to benefit. That said, the US market is in the main domestically focused in terms of revenues (around 70% for the S&P 500). It certainly has nothing like the international earnings profile that the UK market does. The effect will of course be greater if we fish in the mega cap space.

Drought problems are affecting large parts of the globe, but Death Valley in the US still deserves its reputation on the low rainfall front. Average annual rainfall is less than 50 mm, which is lower than even other deserts receive.

Valuations still remain ahead of elsewhere (multiples of cyclically adjusted earnings are still around the 30× mark!) and this ‘premium’ is unlikely to change whatever the market conditions, given the wider attractions of the market. The underperformance this year clearly reflects the fact that some of those areas that have become most outrageously valued – high growth, tech – are more highly represented in the US. If value becomes the dominant style, the US might still lag, but the growth–value battle is far from over in markets (indeed growth has led the recent rally in stock prices).

A recession will do cyclicals no favour and a reduction in rates of slower monetary policy tightening could yet mean growth names recover further – and from much more attractive valuations.

Europe - August 2022

It is perhaps a sign of what an extraordinary period we have been through since the financial crisis that investors were surprised by a 0.5% rise in interest rates from the ECB. Bear in mind that this was an increase in its main rate to zero! Realistically there was not much alternative as the central bank has to do something to respond to the persistently high inflation, but it comes at an interesting time. Economic data is not moving in the right direction with eurozone business activity falling to a 17-month low in July and the prospect of a recession looking all too real. On top of this we have the possibility of a worsening in the energy outlook for the continent with Russia essentially able to engage in blackmail given its (current) control over natural gas. Patience with the hard-line tactics from European leaders towards Ukraine is already starting to wane and tensions lie ahead.

All this is well documented but the developments in Italy have come as more of a surprise. The resignation of Mario Draghi from the government follows the opposition leaders boycotting a confidence vote and means snap elections will now be held. A new bond buying programme is being unveiled by the ECB, which comes at a time when spreads of Italian bonds have been widening over those of German ones and this has caused significant unease. As we have warned previously, those structural problems haunting the eurozone have not gone away and a stagflationary environment is really not what policy makers and investors are looking for. If any central bank can be said to be facing an almost unwinnable balancing act between controlling inflation and avoiding recession, it’s probably fair to say the ECB fits the bill.

Last year saw the worst floods in Europe in over a century – Germany, Belgium and the Netherlands were all heavily affected with over 200 fatalities and many more lives devastated.

Due to the perilous outlook and the extreme negativity towards Europe, some will see an opportunity to add to allocations. For us this looks too early and conversations around trimming exposure are inevitable given the cocktail of risks. For now, we are holding positions at current levels.

Rest of the World - August 2022

The shocking assassination of ex-Prime Minister Abe has left Japan reeling. Although a discrete event, the tragedy has added further to the unsettled atmosphere in the country and comes at a time when there is concern over wider security. Japan has warned over increased cooperation between Russia and China and many politicians are pushing for increased defence spending and a revision of the country’s pacifist constitution. Any radical increase in defence spending is likely to run into significant opposition from the more fiscally reserved of the country’s politicians and Japan has, in common with many other nations, just reduced its growth forecast.

In terms of monetary policy, the Bank of Japan has re-stressed its determination to keep rates low and stimulus high. The yen therefore remains under significant pressure and the trade deficit deterioration from higher energy prices and other causes has exacerbated this. The weak yen could benefit some stocks but penalise others (those whose manufacturing occurs largely abroad, for example), and the direction of the yen is sufficiently unclear to mean that its traditional safe haven status is far from assured.

As has been the case in most geographies over the year to date, large cap and value style strategies are the ones that have fared best. Further deterioration in global growth prospects would probably see the market cap performance bias maintained, but the value style (well represented in the banking sector in Japan) might not see a continuation of its good run. The market as a whole does offer the investor a degree of margin of safety from a valuation perspective – it remains cheap relative to most other developed markets – but this has been the case for some time.

Earthquakes are unfortunately rather common in Japan and some scientists believe they can be triggered by extreme meteorological events. The main fault lines responsible are the Itoigawa-Shizuoka Tectonic Line (ISTL), which cuts across Honshu north to south just west of Tokyo, and the Median Tectonic Line (MTL), which is an east-west trending fault that parallels the Nankai Trough from the Kii Peninsula into the heart of Kyushu.

No particular catalyst is foreseeable for Japanese equities in the short term, but given the balance of other options in the equity market, holding allocations at current levels seems justified. Elsewhere, there are no changes to our Asia or Emerging Market allocations.

Commodities - August 2022

In last month’s edition, we commented that metals prices had started to roll over, due to concerns over global growth prospects. In July that became evident in the equity arena, as a number of mining stocks reported results. Rio Tinto, whose large exposure to iron ore makes its fortunes closely tied to Chinese construction growth, announced a sharp drop in profits and cut its dividend by more than half. For miners, higher labour and energy costs have coincided with falling metals prices, making the situation particularly painful. Most large cap miners have now given up the significant gains they made in the first quarter of the year and the days of bumper payouts could be over for now.

The outlook for energy producers is more positive, with oil and gas prices remaining stubbornly high. The latter continues to be incredibly sensitive to news developments and European gas prices jumped towards the end of July, as flows from Nord Stream 1 were cut to 20% of normal capacity. This follows a decision in June to cut supplies to 40% and heaps more pressure on the region. The situation is wreaking havoc on European utilities, with nationalisations and bailouts occurring across the continent. France has moved to take EDF, Britain’s fourth largest householder energy supplier, out of private hands completely. In Germany, the government has provided Uniper with a €15bn rescue package, taking a 30% stake in the business.

Higher gas prices lead to higher fertiliser prices, which feed through to higher food prices. Soft commodities are also affected by extreme weather. Weather derivatives are financial instruments that allow corporations and individuals to increase or reduce risk associated with weather. This niche corner of financial markets allows farmers to hedge against poor harvests.

We retain energy and broad mining exposure for higher risk clients. While the latter has sold off, we believe in the long-term benefits of holding exposure to these types of businesses. In the case of energy transition metals, the long-term dynamics of tight supply and high future demand remain intact.

Responsible Assets - August 2022

At the end of July, it was one small step for Joe Manchin but one giant leap for mankind. The West Virginia senator, and critical swing voter in an evenly divided US Senate, surprised Washington recently by saying he will support a bill aimed at cutting planet-heating emissions. Senator Manchin (who also happens to be a coal company owner) has made headlines by repeatedly thwarting the Biden administration’s attempts to pass legislation aimed at tackling climate change. The new proposal is part of a reconciliation budget that can only be passed with all 50 Democratic votes in the Senate, due to unified Republican opposition, meaning Manchin’s acquiescence was crucial.

So, why did Manchin change his tune? It seems a reasonable conjecture that the current energy crisis has highlighted the importance of a self-reliant future for the US in terms of energy supply. The choice between being beholden to Russia or Saudi Arabia is like a case of picking your own poison. We wrote previously that clean solutions could offer energy independence for countries forced to rely on oil and gas rich nations, and now it appears that politicians are taking this seriously. The proposed spending, which is part of a broader package known as the Inflation Reduction Act, would set aside $369bn for climate and clean energy programmes.

One of the main features of the bill is its allowance for large tax credits for clean energy, such as solar and wind power, enabling such projects to go ahead on a large scale. Some $30bn is also earmarked for states and utilities in order to aid the transition to renewable, zero carbon electricity. This vast level of spending should provide an uplift for several companies in the space such as NextEra.

Climate change can’t be blamed for every extreme weather event, but evidence continues to mount that the frequency of such events is increasing. Getting large countries like the US and China to enact meaningful climate change policy is vital to slowing down climate change, but most agree that changes already witnessed are irreversible.

We continue to provide exposure to companies facilitating the shift to a more sustainable economy within portfolios. We see evidence that the energy transition is accelerating in all regions and believe that this is reflected in an improved and increasingly robust earnings outlook for much of the space.

Currency - August 2022

In July, the US dollar hit its highest level in 20 years and managed to reach parity with the euro. A strong dollar is increasingly problematic for US corporations, with foreign earnings translating back at lower rates and their exports comparatively more expensive. This has been highlighted by several blue chip names from a range of sectors over the past quarter and is expected to wipe billions off corporate earnings. IBM, Johnson & Johnson, Netflix and Microsoft have all warned of the impact. In terms of exposure, 29% of S&P 500 sales are generated outside the US. For the technology sector, this number rises to 59%.

The main reason for US dollar strength is the speed and size of interest rate increases, outstripping that of many peers around the world. With so much inflation being caused by the commodities space, the fact that the dollar is typically the global pricing mechanism adds fuel to the fire.

The situation is problematic for emerging market governments, many of which have significant debt piles denominated in US dollars. These obligations have become increasingly onerous and have already led to significant social unrest in countries like Sri Lanka. The issue isn’t isolated to Asia; indeed Latin American nations have hefty levels of exposure. Over half of Argentina’s debt is priced in dollars and the potential for yet more turmoil there remains high.

We continue to consider the strength of the dollar in our decision making. Indeed, it was part of our decision to removing emerging market debt exposure towards the start of the year.

Healthcare - August 2022

The broad healthcare sector is one of the few to have delivered a positive return over the last year. Spending on healthcare is generally non-discretionary for governments and households alike. However, as long-term investors in healthcare, we believe the space is not simply a defensive place to hide during a crisis but is an important part of any well-balanced portfolio.

We do acknowledge some short-term headwinds for the space. Covid-19 waves continue to impact certain countries at various times, which is impeding the ability of healthcare providers to function normally. In addition, a red-hot labour market in the US is putting pressure on providers like hospitals. Such periods, however, present active managers with interesting opportunities to pick up stocks with strong long-term fundamentals at cheap valuations.

Much like the Russia–Ukraine war and ensuing energy crisis shone a light on the fragility of energy supply changes, the Covid-19 pandemic highlighted the need to make health services more resilient to future crises. This is particularly vital when we consider that a majority of developed markets have an ageing population. Budget pressures across global healthcare systems have made investing in efficiency enhancing technology a necessity not just a convenient option.

Over the past few years, new technology has opened up a vast array of possibilities from new treatments to new methods of accessing healthcare. As well as new options for treatments, new markets are opening up as growth in emerging market economies enables more people to access healthcare services. It is these opportunities we seek to access by investing in healthcare for the long term and we believe that a broad exposure to the space remains appropriate within core portfolios.

The Monthly Market Commentary (MMC) is written and researched by Simon Gibson, Richard Smith, Scott Bradshaw, Jonathon Marchant and Lauren Wilson for clients and professional connections of Mattioli Woods, and is for information purposes only. It is not intended to be an invitation to buy, or to act upon the comments made, and all investment decisions should be taken with advice, given appropriate knowledge of the investor’s circumstances. The value of investments and the income from them can fall as well as rise and investors may not get back the full amount invested. Past performance is not a guide to the future. Mattioli Woods is authorised and regulated by the Financial Conduct Authority.

The MMC will always be sent to you by the seventh working day of each month, usually sooner, is normally delivered via email, and is free of charge as the MMC is generally made available to clients who have assets under our management in excess of £200,000, and to all clients under our Discretionary Portfolio Management Service (DPM). Normally, the MMC costs £397 + VAT per annum. Professional advisers and their clients should contact us if they are interested in receiving a monthly copy.

Sources:

www.bbc.co.uk,

www.bloomberg.com,

Financial Express,

www.thedragonsblade.com,

www.express.co.uk,

www.pitstoppin.co.uk,

www.sibcyclinenews.com,

www.vr-12.com,

www.smalltalkbigresults.wordpress.com,

www.anonw.wordpress.com

www.avantida.com,

www.plazmedia.com,

www.viewzone.com,

www.mmn.com.

All other sources quoted if used directly; except fund managers who will be left anonymous; otherwise, this is the work of Mattioli Woods.