Global markets summary - August 2024

July was marked by significant rotation within equities, as heightened expectations of interest rate cuts in the US and UK spurred a rally in small-cap stocks and other interest rate sensitive asset classes.

While value-orientated stocks and smaller companies played catch up, larger companies broadly underperformed across the board and investors were particularly underwhelmed by earnings released by some of the dominant US technology companies, resulting in the technology sector coming under pressure for most of the month. European stocks were weaker than their US and UK counterparts amid continued political uncertainty and disappointing data, while Chinese equity markets declined due to ongoing challenges within the real estate sector and the cascading effect on the broader economy.

During periods of high volatility and market dislocation, it is not always possible to predict which assets will be marked down the hardest. Typically, smaller companies are perceived as higher risk and, as such, tend to sell off most dramatically during periods of uncertainty. On this occasion, larger companies have been hardest hit as their valuations, especially in relation to US large-cap tech, were the most stretched.

Fixed income markets generally offered positive returns over July, with most developed market government bonds rallying as expectations of policy easing increased. Despite a move away from riskier assets, high-yield corporate debt also had a positive month, supported by the prospect of lower interest rates. In contrast, commodities were bruised by the move towards risk-off sentiment, with industrial metals and agriculture taking the brunt of the pain. In precious metals, gold prices were modestly higher while the price of silver fell.

Although headlines have been sensational and some of the market moves sharp, we do not believe that we are on the cusp of a financial crisis. In 2008, landmark events in the banking sector triggered the great recession. Currently, there is very little evidence of the financial imbalances that precede such a recession; both personal and corporate balance sheets remain in good shape, and we have not seen a widespread downturn in economic data. We should also keep in mind that economic data is backwards-looking and is often revised. While the most recent set of data from the US has been softer, it is not dissimilar to a month ago when markets were more constructive, and a US interest rate cut next month may see this sentiment reverse.

We do not view July’s moves as the beginning of a bear market; our central case is for increased volatility, driven by a combination of weaker economic data and continued elevated political/geopolitical tensions. We expect gains to broaden out to other sectors (rather than be concentrated in mega cap tech) and to markets elsewhere. While we do not view this recent rotation as the beginning of a sustained trend, it is timely that, in terms of asset allocation, we downgraded US equities to neutral and upgraded UK equities to positive at the start of July.

United Kingdom - August 2024

Elections were always likely to be a focus for investors in 2024, with more voters heading to the polls around the world than ever before. With several elections delivering shock results, the UK’s was reassuringly predictable, with Labour securing a strong majority. For investors, increased political stability has been well received and, when combined with robust economic data, sentiment towards UK stocks seems to be improving.

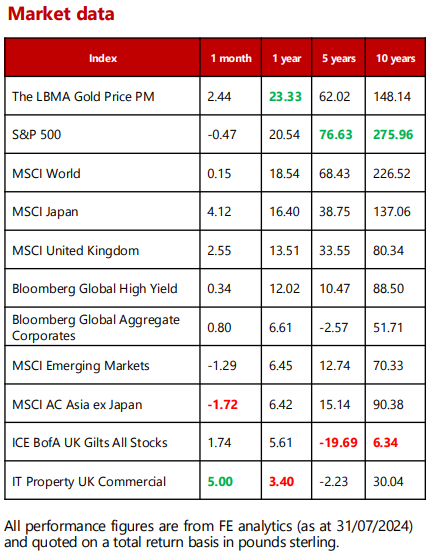

Indeed, the MSCI United Kingdom All Cap delivered strong performance in July (+3.19%), outperforming most other global equity markets. Underlying the headline index performance was a particularly strong showing from mid- and small-cap companies. This outperformance can be attributed to a variety of factors. Firstly, these companies should be the greatest beneficiary from domestic growth and political stability. Secondly, domestically- focused businesses tend to benefit from the strength of sterling, which has been the best performing developed market currency in 2024.

The backdrop for UK equities remains strong. Household savings ratios remain relatively high and inflation appears to be under control, both of which should spell a relatively buoyant consumer. Equity valuations remain low relative to peers, despite recent performance. Equally, with US and Indian equities looking expensive, a myriad of geopolitical issues in Europe, Japan having performed well and China continuing to grapple with growth, the UK seems like a reasonable investment destination.

Importantly, there seems to be a willingness to change from political and regulatory institutions. In July, the FCA implemented the largest changes to listing rules for three decades. The changes aim to make life easier for companies listed or considering listing in London, with amendments to rules on voting rights, shareholder approvals and more. While the changes may come at the expense of shareholders, the aim is to reinvigorate the London Stock Exchange, which has seen the number of listed companies fall dramatically over recent decades.

While we are always wary of the erosion of shareholder rights, we see the development as an essential part of making the UK market competitive with the US and others. We see it as yet another positive news story for UK equities and believe domestic equities represent a compelling investment opportunity. In our UK Dynamic Fund, we continue to tilt towards mid- and small-cap companies, which we feel could be the greatest beneficiaries of the positive change we see ahead.

North America - August 2024

Overall, US shares ended July in positive territory, but the headline figures mask the sharp rotations within the market. Growth stocks (those with strong future growth potential) were particularly weak, with investors moving towards more lowly-valued companies. The IT sector fared worse than any other through July, amid worries that the US might seek to impose further restrictions on what semiconductor equipment can be sold to China. Allied with weakness in the communication services sector, this weighed on the S&P 500 Index.

One of the most striking dynamics over the month was the shift towards smaller companies, which led to the largest one- month outperformance of the Russell 2000 (a small-cap US stock market index that makes up the smallest 2,000 stocks in the Russell Index) versus the Nasdaq 100 (an index of the 100 largest non-financial companies listed on the Nasdaq stock exchange) in over 20 years.

For much of the year, investors expected that the US Federal Reserve (Fed) would deliver a ‘soft landing’, curtailing inflation without toppling the economy into a recession. Over July, however, investors grew dubious on the Fed’s ability to stick the landing. Weak US labour market numbers released shortly after the Fed held interest rates steady at 5.25%- 5.50% have led to widespread fears that the central bank’s inaction could lead the US into recession. As we noted in the market summary, we do not anticipate a full-blown recession but we do expect to see the US economy cool and view a rate cut at the next meeting in September as highly likely.

We do not view this recent rotation as the start of a prolonged trend. We think US mega cap tech will rebound before too long but that gains will broaden out to other sectors and to markets elsewhere. Despite the pullback observed throughout the month, growth stocks have returned 16% year-to-date, contributing to the 14% year-to-date (to end July) gains in broader developed market equities.

While we do not anticipate a US recession, we have downgraded our exposure to US equities within portfolios to neutral, based on our view that valuations were looking a little stretched. We have ensured that we are not overexposed to one area of the market by adding specific exposure to a value-orientated position several months ago.

Europe - August 2024

The majority of European equities struggled over July as investors digested a disappointing Purchasing Managers’ Index (PMI) alongside continued uncertainties around the French election.

Reflecting moves across global markets, information technology sectors sold off while weak consumer demand weighed on the luxury goods and automotive segments within the consumer discretionary sector. Despite the widespread weakness, a handful of sectors did enjoy positive returns; strong quarterly earnings and positive clinical readouts helped to support stocks in the healthcare sector and a move towards interest-rate sensitive assets boosted utilities, and real estate.

Even with France supporting growth amid the Olympics, the eurozone economy was seen grinding to a halt in July with the flash PMI indicating that the economy was near stagnation, with a reading of 50.1, down from 50.9 in June. The manufacturing recession continues to be the main hinderance but the services sector is also starting to slacken, which should perturb the European Central Bank amid signs that inflationary pressures are continuing to persist.

An initial estimate showed that annual inflation in the eurozone picked up to 2.6% in July from the 2.5% registered in June. A consensus estimate had called for inflation to decelerate to 2.4%.

Taking a broad range of data into account, the full picture for the bloc is not quite so

straightforward. The European Commission’s consumer confidence indicator for the euro area actually increased in July and has improved steadily since February amid optimism that borrowing costs would decline. While a decline in service sector activity was viewed as a negative, services inflation eased for the first time in three months. This variegated outlook has led us to retain a neutral stance on European equities.

We maintain a balanced exposure to European equities within core portfolios via a complementary blend of actively-managed strategies focusing on specific areas of the capitalisation scale.

Rest of the world - August 2024

The Japanese equity market experienced high volatility during July, reaching a historical high early in the month then correcting sharply. While some of the moves may have been driven by the weakness in global tech stocks, pressure from a stronger yen and the prospect of higher rates, the substantial swings appear to be caused by speculative activity rather than any change in fundamentals. Japanese macroeconomic conditions remained solid over the month with no major negative developments; as such, the sharp shift in the Japanese yen appears to have been driven by short-term money. We have covered this in greater detail as per a request in the ‘Ask us anything’ section.

Overall, Asia Pacific equities faced several headwinds in July, including ongoing concerns around China’s economy and lacklustre earnings from US technology companies. Stocks in Taiwan were particularly affected by the sell-off in technology stocks towards the end of the month, with semiconductor makers experiencing the sharpest price falls. However, despite the monthly downturn, Taiwan remains the best-performing market in the Asia Pacific index year-to- date. Similar to Europe, the healthcare sector was the strongest sector across the region, driving modest gains across Indian and Indonesian markets.

Markets across China were down amid ongoing concerns about its economic health. In order to combat continued economic malaise, Chinese authorities implemented measures to provide liquidity to support the financial system, including cutting the reverse repo rate, a key short-term policy rate, and lowering the benchmark loan prime rate. These efforts aim to stimulate lending and support economic growth amid ongoing market challenges, but investor reaction was tepid.

We have a neutral exposure to broad Asia Pacific and emerging markets’ equities across core portfolios as well as a small allocation to Japanese equities.

Fixed income - August 2024

July was generally a good month for fixed income assets. Government bond yields took a sharp leg lower (resulting in an increase in bond prices) towards the end of the month as market bets on imminent rate cuts intensified. The potential start of a rate- cutting cycle, being crucial for bond markets, meant that central banks took centre stage once again.

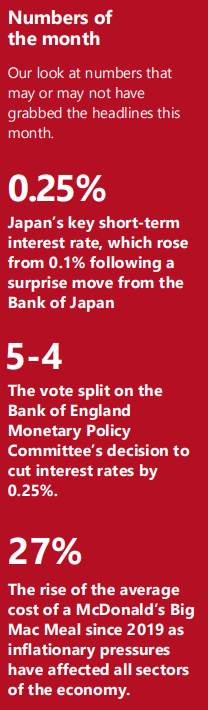

The US Federal Reserve (Fed) has indicated that it is ready to cut interest rates as soon as September, after voting to hold them at 5.00-5.25% for the eighth consecutive meeting. Similarly, barring any major data surprises, the European Central Bank (ECB) appears to be gearing up for a September rate cut. In contrast with other major central banks, the Bank of Japan raised interest rates to 0.25%. Although the Bank of England met expectations by cutting rates to 5% at their July meeting, stronger-than-expected GDP growth in the second quarter, combined with persistent services inflation, suggests that UK interest rate cuts may be more gradual compared to the US and Europe.

Returns from corporate debt were broadly positive with higher-quality investment grade bonds outperforming high-yield bonds. Across developed markets, the underlying growth outlook remains healthy thanks to robust consumer balance sheets and solid levels of business investment. This combination should keep corporate defaults low. Given our anticipation of heightened volatility across markets, we believe that credit selection remains key, and within core portfolios we have sought to invest in active managers seeking bonds with favourable income and solid fundamentals.

Overall, our central case is that the next move for the major developed market central banks is policy easing rather than tightening. As a result, the medium-term outlook for fixed income still looks attractive.

Ask us anything - August 2024

Q: What is going on in Japan?!

A: We have made the bold assumption that this question relates to the recent investment market volatility within the region, given that this is the area on which we are most qualified to provide comment!

We have seen back-to-back record falls (in points terms) of the Japanese Nikkei 225 Index since the October 1987 crash. This has seen Japanese markets fall over 20% from the all-time high levels seen in July.

Alongside weak US economic data and disappointing major tech company earnings, the volatility in Japanese markets was exacerbated by a surprise change in Japanese monetary policy. The unanticipated interest rate hike from the Bank of Japan led to investors winding down yen-funded trades that had been used to finance the acquisition of stocks for years.

This is known as a ‘carry trade’, wherein an investor borrows in a currency with low interest rates, such as the Japanese yen, and reinvests the proceeds in higher-yielding assets elsewhere. The trading strategy has been hugely popular in recent years and, as such, its reversal has had a sizeable impact on markets.

Over the month, the Japanese yen strengthened from 162 yen to 150 yen against the US dollar by the end of July. A stronger yen is seen as a negative for the large exporters who dominate the Japanese index, and the currency is likely to remain strong, especially with the Bank of Japan increasing interest rates at a time when other major central banks are cutting.

However, currency alone has not driven the sell-off, with many international investors selling Japanese equities, on broad concerns over global equity markets and a shift towards risk-off sentiment. While the fundamentals of Japanese equities have been improving in terms of greater shareholder returns focus, ultimately, much of the rally has been driven by overseas investors, and with sentiment turning, many have seen Japan as an easy place to take profits and/or reduce risks around the currency.

If there is a question you would like to pose to our team, please reply to this email or write to [email protected].

The Monthly Market Commentary (MMC) is written and researched by Scott Bradshaw, Lauren Hyslop and Jonathon Marchant for clients and professional connections of Mattioli Woods and is for information purposes only. It is not intended to be an invitation to buy, or to act upon the comments made, and all investment decisions should be taken with advice, given appropriate knowledge of the investor’s circumstances. The value of investments and the income from them can fall as well as rise and investors may not get back the full amount invested. Past performance is not a guide to the future.

Mattioli Woods is authorised and regulated by the Financial Conduct Authority.

Sources: All other sources quoted if used directly, except fund managers who will be left anonymous; otherwise, this is the work of Mattioli Woods.