Global markets summary

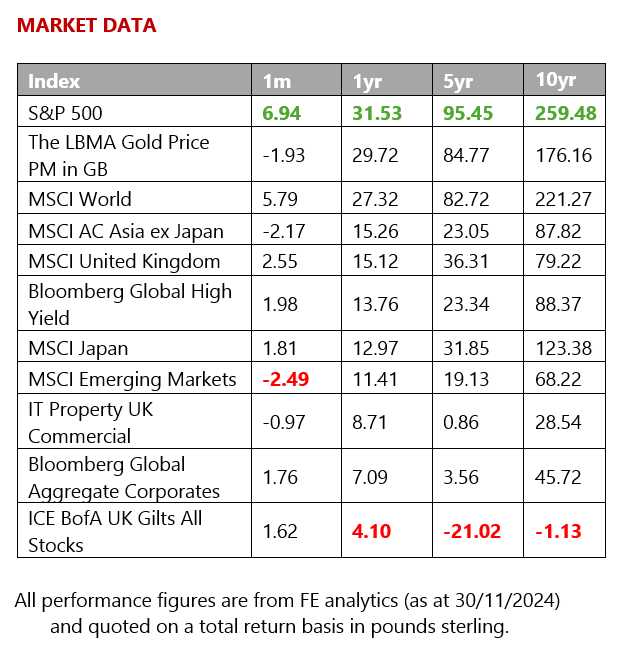

Global equity markets were mixed over November, with developed markets largely outperforming their emerging peers. Unsurprisingly, the US election results were the main driver of market performance over the month. Donald Trump’s decisive presidential victory, which saw the Republican party securing a majority in both chambers of Congress, drove US equity markets higher, with the S&P 500 ending the month up 5.83% in local currency terms and 7.04% for sterling investors, thanks to the relative strength of the US dollar. Investors appear to be embracing the prospect of further tax cuts, deregulation, and expansionary fiscal policy, as well as the implementation of a more nationalist ‘America first’ trade policy.

Away from US markets, the election result was met with a degree of caution, as uncertainty remains about US foreign policy, as well as the policy responses of other regions. UK markets made modest gains over November while the broad European market ended the month down. Overall, emerging markets trailed developed markets by nine percentage points. The MSCI China Index declined 4.12% in local currency terms as investors added concerns about a future trade conflict to existing worries that the previously announced government support measures are insufficient to overcome the domestic real estate and confidence crisis.

The current rush into developed-market risk assets could persist through the end of the year but thereafter, the outlook is more complex. Despite the very positive reaction of US equities and the dollar to Trump’s victory, with investors seeming to expect a repeat of 2016, we note that, eight years later, economic conditions are starkly different.

Major central banks continued to lower interest rates during November, with rate cuts on both sides of the Atlantic. However, bond markets only marginally benefited as investor focus shifted to a potential second wave of inflation ignited by President-elect Trump’s policy proposals in the US and an inflationary budget in the UK.

Although the calendar year will change in January, the driving forces behind the markets are likely to remain the same. The evolution of economic fundamentals, and the impact of policy changes on them, will continue to be crucial. As we enter the new year, investors may start to question whether smaller companies, value stocks, and cyclical sectors will be supported by a more laissez-faire environment or weighed down by stubbornly high inflation and rates.

United Kingdom

While the UK Budget was announced in October, it continued to attract column inches in November. Last month, we commented that what ‘remains to be seen is how consumers and businesses will react to the Budget’, and early data points remain mixed.

Backward looking data over the month certainly suggests that the UK economy slowed in recent months. GDP figures, which measure overall economic output, fell relative to the previous quarter, suggesting a slowdown. This is juxtaposed with forward-looking consumer confidence data, which picked up materially over the month.

The Bank of England took a balanced approach at its meeting in November, deciding to cut interest rates to 4.75% but noting the plans set out in the Budget to add to inflationary pressures, and signalling a gradual path to further cuts.

Though we will hopefully enjoy some political stability in the UK over the next year, investors now have to grapple with the uncertainty that a Trump presidency may bring. Tariffs look certain and are likely to create volatility, as well as the potential for higher inflation. Equally, choices for senior roles in government are likely to have significant implications for UK companies. Most notably, pharmaceuticals businesses AstraZeneca and GSK sold off sharply on news that Robert F Kennedy Jr was to be put forward as US Secretary of Health and Human Services, given his scepticism around vaccines.

The changes from the UK Budget and the election of President Trump have added a layer of complexity to proceedings, and we believe that active managers could add value over the next few years. Within our UK Dynamic fund, we continue to favour mid-cap stocks, which tend to be more domestically focused and less susceptible to trade wars. Interest rates look unlikely to fall sharply anytime soon, which we think lends itself to companies with solid balance sheets that are distributing capital to shareholders today.

North America

Over November, US equities bested other markets significantly as markets responded favourably to Donald Trump’s election victory. The US market outperformance mirrors the year-to-date trend, with US stocks once again outpacing the rest of the world, with the main market rising over 25%. The market performance has been largely fuelled by the strength of beneficiaries of the artificial intelligence (AI) boom as well as the prospect of lower interest rates.

Although there is evidence of slowing growth in certain areas of the economy, namely the manufacturing sector, overall, economic data from the US remains robust. Personal income rose 0.6% in October, roughly double consensus estimates, while personal spending rose 0.4%, a tick above expectations. Pending home sales also defied expectations for a decline and rose 2.0%, even as September’s gain was revised up to 7.5%, the strongest gain in nearly two years. Measures of inflation expectations by the households, businesses, and financial markets remain consistent with the Fed’s 2% target. However, President-elect Trump’s proposals (including lower taxes, new tariffs, and deportations) could drive inflation higher.

This year, we saw the US economy fall back to equilibrium, and the much-discussed soft landing (where economic growth slows but does not contract and inflation pressures ease) appeared to be delivered. The key question as we move into the new year is: can this momentum be sustained? There remains some uncertainty around how President-elect Trump will tackle central issues on the US political agenda, including tighter immigration controls, more relaxed fiscal policy, businesses deregulation, and tariffs on international goods. This uncertainty has driven our recent preference for active management within the US equity portion of our core portfolios. Within our multi-asset solutions, we have been rotating out of passive index tracking funds and into actively managed funds with specific mandates over the past quarter.

We retain a neutral stance on US equities, acknowledging that the region continues to enjoy several tailwinds. However, the relative expense of valuations for US stocks – based on both stock-level valuation models and top-down expected return estimates – prevents us from taking a wholly positive view.

Europe

European markets had a challenging November, with the EURO STOXX 50 returning -1.53% (in £ terms) over the month as the region endured political instability and uninspiring economic data. Concerns about the impact of President-elect Trump’s US trade policy as well as earnings warnings from the automotive and consumer goods sectors were also unhelpful.

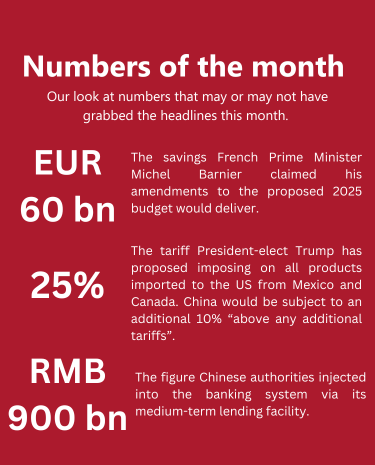

Economic data continued to point to weakening growth across the bloc. Data released over the month showed that Germany, the eurozone’s largest economy, continued to struggle in the last quarter of this year with retail sales decreasing more than anticipated over October. Recent outbreaks of political instability across the bloc have contributed to investor jitters over the region’s stock market. Towards the end of the month, the political temperature in the region’s second largest economy, France, reached boiling point, with far-right and leftwing opposition parties threatening a no-confidence vote in the incumbent Barnier government following discussions around the French budget. The no-confidence vote, which will take place on Wednesday 4 December, is highly likely to topple the three-month-old French administration.

According to a preliminary estimate, annual inflation in the bloc accelerated for a second month in November to 2.3% from 2.0% in October. The increase did not come as a surprise, as last year’s declines in energy prices ceased being incorporated in the annual rates. However, underlying inflation unexpectedly declined with services’ prices easing. As at time of writing, markets still expect the European Central Bank (ECB) to lower borrowing costs in December, although the size of the reduction remains uncertain.

Our stance on European equities remains neutral given that the outlook for growth remains uninspiring and President-elect Trump’s expected tariff policies could pose a significant headwind. That said, the impact of tariffs is likely to be deflationary for Europe and increase scope for the ECB to cut rates further.

Rest of the world

For the first three quarters of the year, Asia Pacific (ex-Japan) markets languished, trailing developed markets by a significant margin. This changed dramatically in September when Chinese authorities committed to further monetary and fiscal support, soothing investor concerns and supporting a broad rally across Asia Pacific equities. While we have seen Asia Pacific markets pull back as investors began to doubt the efficacy of the stimulus package, they look on course to end the year in positive territory, with the MSCI China Index delivering 17.69% and the MSCI Asia Pacific ex Japan Index returning 15.13% year to date (end November) in local currency terms.

November was a more challenging month for the region. Following Donald Trump’s victory in the US presidential election, trade risk has increased as an American first trade policy poses a risk to growth outside of the US. It appears that the President-elect will stack his cabinet with ‘China hawks’, signalling a tough stance, potentially forcing the Chinese authorities to enact further stimulus measures.

Indeed, trade policy risk, as well as a strengthening US dollar, negatively impacted several emerging markets over November. Latin American markets also bore a significant brunt of the pain as President-elect Trump indicated that plans to impose a 25% tariff on all imports from Mexico would be one of his first executive orders. This approach is in line with the President-elect’s prior use of tariffs during his first term. You may remember 2018, when tariffs were imposed on Mexican steel and aluminium (based on national security concerns). These were subsequently lifted a year later as part of the United States-Mexico-Canada Agreement trade negotiations. This is consistent with our base case view that Trump favours tariffs as a negotiating tactic, with substantial threats used to secure important concessions from trading partners. While this could be relatively constructive for global equity markets over the long term, such tactics are not without risks and tend to evoke short-term market volatility.

Within our core portfolios, we retain a neutral stance towards Asia Pacific and emerging market equities, accessing these regions via a blend of actively and passively managed funds. Developments over November strengthened our conviction that Western developed market equities (such as the UK and US) are better positioned over the medium term.

Fixed income

Although US and UK central banks met market expectations by lowering interest rates over the month, investors’ expectations were scaled back with fewer rate cuts now pencilled in for 2025. The reassessment was largely driven by President-elect Trump’s potentially inflationary policy proposals in the US and the aftermath of the UK Budget. Concerns over future fiscal extravagance also pushed bond yields higher, a trend more pronounced for UK Government debt (gilts) towards the month’s end, though the divergence from other regions was modest.

While equity markets are more positive, the bond market appears on edge and to be warning of a serious concern that interest rates may move higher due to fiscal risks and inflation dynamics. Against this backdrop, we continue to favour bonds with a lower duration (sensitivity to interest rate changes) and prefer corporate credit over sovereign debt. We are currently skewed towards high-yielding areas of the market as default rates remain low and earnings estimates are supportive.

While the path of interest rates remains uncertain, we maintain a balanced exposure to a broad spread of fixed income assets within core portfolios. We view the neutral/negative correlation to equities that fixed income assets now provide as beneficial to multi-asset portfolios.

Ask us anything

Q: Why has there been so much hype around AI and do you think it will continue?

A: Investor exuberance of AI has been a defining characteristic of 2024. In the first half of the year, six stocks (Meta, Alphabet, Microsoft, Nvidia, Amazon, Apple) accounted for more than half the total return of the US equity market. Unsurprisingly, these companies are all linked, in some way, to AI. Leading producer of the chipsets that power AI, Nvidia has recently become a household name. The company’s shares have climbed more than 600% since the launch of generative AI chatbot ChatGPT in November 2022. Subsequent strong revenue and earnings growth across the board has pushed the concentration of the US equity market to record levels.

The outlook for these companies remains generally positive. Although not homogenous, they do share common characteristics that allow them to dominate their respective industries with high barriers to entry. Unless there is significant regulatory intervention to break these ‘franchises’ (which is of course less likely when the US is under Republican control), they will likely remain highly profitable companies and important components of global portfolios.

That said, we are not blind to the risks these companies face. As you have likely heard, these companies now sit on lofty valuations, which means that a majority of the ‘good news’ for these companies has now been priced in and could entail that any less than stellar results or developments are punished harshly by the stock market. In addition, some investors have begun to raise their eyebrows over the sheer volume of spending being directed towards AI. The three main providers of AI infrastructure, Microsoft, Alphabet-owned Google, and Amazon are investing gigantic sums in an AI ‘arms race’, and the rate of spend shows no sign of abating.

Within our core portfolios we have a neutral stance (meaning that we are in line with our benchmark) to US equities, but we are more balanced than peers in terms of style exposure. We hold the mega-cap tech companies via a blend of an actively managed US growth focused fund and passive index tracking funds, but we also maintain a position in value-orientated stocks as we expect performance of the market to be less concentrated in 2025.

If there is a question you’d like to pose to our team, please reply to this email or write to [email protected].

The Monthly Market Commentary (MMC) is written and researched by Scott Bradshaw, Lauren Hyslop and Jonathon Marchant for clients and professional connections of Mattioli Woods and is for information purposes only. It is not intended to be an invitation to buy, or to act upon the comments made, and all investment decisions should be taken with advice, given appropriate knowledge of the investorʼs circumstances. The value of investments and the income from them can fall as well as rise and investors may not get back the full amount invested. Past performance is not a guide to the future.

Mattioli Woods is authorised and regulated by the Financial Conduct Authority.

Sources: All other sources quoted if used directly, except fund managers who will be left anonymous; otherwise, this is the work of Mattioli Woods.