United Kingdom - February 2023

Romance – apart from the obvious (the excitement and mystery associated with a loving relationship), a romantic feeling is one of excitement, mystery and remoteness from everyday life, such as ‘the romance of the sea’. This doesn’t mean we love the sea. (Just in case it helps any of our readers, Valentine’s Day is next week!)

In an article in 1916, Lieutenant-Commander Taprell Dorling wrote, “There is without a doubt something fascinating in the great ocean; something intangible and indefinable perhaps, but nevertheless existent” and W H Auden wrote, “… the symbol for the primordial undifferentiated flux, the substance which became created nature only by having form imposed upon it or wedded to it” in ‘The Enchafèd Flood’, where he endeavoured to compare the sea with the conceptual world of certain 19th century writers. Wordsworth, Coleridge, Byron, Shelley and Keats were not known for writing about economics or investing but they understood romance.

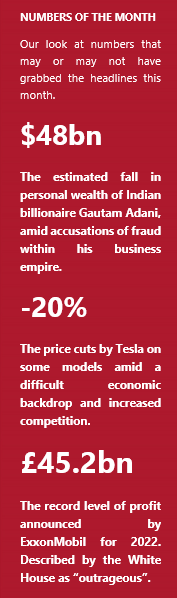

Taking the ‘everyday life’ meaning above, as throughout this edition we have plenty to say on the ‘associated with love’ version, we wonder if investors are feeling romantic about various risk assets. For example, equities provide excitement, a degree of mystery (some more than others) and certainly can deliver a remoteness from everyday life – the dream of making one’s fortune; the nightmare of one’s fortune collapsing almost overnight. For those who don’t track such things, have a read about Adani in India.

There also seems to be a remoteness, disconnect if you prefer, to investor sentiment and the economic and investment landscape at the start of 2023. Seeing many risk assets (not just the aforementioned equities) gather some forward momentum is not unusual ahead of the worst news on, say, a recession. The difference this time is that there are so many issues facing investors, all/any of which could in their own right be troubling and yet they seem to be being brushed aside. This is NOT to say we are negative about everything, far from it. Rather, we feel that some assets/prices have a remoteness from reality. Some investors seem to have adopted a rather romantic view of some assets.

It can be very easy to get romantically attached to the familiar, in this case, UK equities and other assets that might be ‘closer to home’. This can be dangerous, especially if one loses a sell discipline. This is not to say we don’t want to have a home bias for UK investors whose lives are all ‘in sterling’, that makes sense. But we must (and do) assess that same home bias versus global equity markets and other non-sterling assets. Finally, a quote from Lord Byron to remind us that maintaining sensible levels of cash/liquidity is as important today as it was 200 years ago – “Ready money is Aladdin’s lamp”.

North America - February 2023

For once, the US is lagging behind other global stock markets. In recent times this has been very rare but a weaker dollar combined with the reopening of China has meant capital has been quickly redistributed by investors. The US enjoys a high degree of energy independence, which means it has had a relative advantage over other markets when energy prices have been elevated. The easing in both gas and oil prices discussed elsewhere means this advantage has disappeared for now and other regions look relatively more attractive, or at least relatively less unattractive as a result.

The switch from growth to value as the predominant style appealing to investors has also made a significant contribution to the change in fortunes, as growth is more heavily featured in US indices than elsewhere. The US has been so dominant in part because of this feature, exacerbated by the mega-cap tech stocks but these are now under pressure and the opportunities are seen by many as lying elsewhere. All of a sudden, valuations are truly at the front of investor minds and, as we have argued for many years, US stocks are more expensive than their global peers on almost every measure one cares to think of.

Investors’ ‘until-recent’ love affair with large technology companies is perhaps not the intense romance it may first seem. Passive funds are obliged to buy companies based on their size alone and active fund managers have often been scared to deviate too far away from ‘in line’ allocations to these stocks in case it results in career-jeopardising underperformance. Of course, this process can work in reverse too as the ‘romance’ sours.

Is this it? Is this the point where the US embarks on a sustained period of relative underperformance? To a large degree, this is dependent on whether the recent direction of the dollar and energy persists. Policy makers will have a say too.

It looks as if the monetary and fiscal stimulus the US market has enjoyed is going to be impossible to sustain over the next cycle and this could continue to help global peers outperform. Large tech companies look as if they might face a more structural bear market than other industries and this will probably be a headwind for an extended period for the US. Smaller companies are presenting some intriguing opportunities but moving to significantly increased exposure ahead of a US recession (an event that is still more likely than not to transpire in our view), seems premature.

Interestingly, our contrarian nature makes us wonder whether the US might, after a brief period of underperformance, regain its crown. A global downturn would make the US an attractive destination for nervous investors, and the fracturing of global trade amid de-globalisation could well see the US emerge as a winner. The valuation differential still looks unattractive for now though and we are not yet making the move to correct our long-standing underweight to the region.

Europe - February 2023

Europe has enjoyed an excellent run of late and, along with the emerging markets space, has been a key beneficiary of the much heralded reopening of China. There is a lot of optimism around, which naturally makes us sit back and reflect, given the number of challenges that seemed to occupy investors until very recently. The region now finds itself in a position where its central bank is the most hawkish in town – which is something of a turnaround considering how far behind the curve they have been both recently and in other cycles. Considering this, the equity market being so robust again seems like something of a disconnect.

The energy story is a really big deal for European companies that have a large constituency of energy-intensive industries (not unlike Japan), so the easing in prices has been tremendously helpful.

The significant falls in gas prices have been an essential ingredient in the sentiment reversal – Dutch natural gas futures, a regional benchmark, have fallen back to where they were pre-Russia’s invasion of Ukraine and are 80% lower than the August peak. Whether this tailwind is likely to persist is rather debatable – the re-emergence of China, considered a major positive for European exporters, could well boost oil prices over the next quarter and on the supply side, there are further sanctions on the imports of Russian oil products, which are due to come into force as soon as February.

So far, corporate earnings in the region have been suggestive of resilience in terms of profits and margins and, in conjunction with the factors mentioned above, this has been enough for traders to warm to the region. There is a hope here, as indeed there is elsewhere, that recession is going to be avoided and forecasts from many banks and commentators for first quarter economic growth have indeed turned positive. Let’s not also forget the sheer amount of EU fiscal support, which amounted to almost 3% of GDP, that has undoubtedly contributed to the resurgence of the region’s equities over the winter. Cue the scurrying of investors to adjust allocations to add more exposure.

Though some think it overrated, Paris is still regarded as being one of the most romantic destinations in Europe. In truth there are lots of places that can compete in this regard, though it certainly has the edge on Frankfurt. Apologies to the ECB.

In a way, Europe is something of a proxy for our wider view on markets. Yes, there is an obvious gearing opportunity into a global recovery but it just feels too early for us to add to equity holdings. Positions are unchanged this month.

Rest of the world - February 2023

Looking at the current policies of the four major central banks, one stands out. At their most recent respective meetings, the US Federal Reserve increased rates by 25 basis points to between 4.50% and 4.75%, the Bank of England increased rates by 50 basis points to 4.0% and the European Central Bank increased rates by 50 basis points and signalled there is more to come. The Bank of Japan (BoJ) did nothing.

This difference in policy has impacted Japan and the Yen in particular, given what is known as the carry trade, where you borrow in one currency with low rates and translate it to a currency with higher rates. This is mixed news for corporate Japan, benefiting some importers, hurting some exporters and making little difference to many international companies listed in Japan but operating globally.

Japan’s current BoJ policy is for negative rates, with the headline interest rate at -0.10%, designed to deter saving. The bank also has long maintained a yield curve control (YCC) policy, intervening in the government bond market to control the yield of the 10-year bond in a band of -0.50% to 0.50%.

The main reason for this is Japan’s deflation struggles and, unlike other central banks, the BoJ are welcoming higher inflation. This is positive to get the economy moving (as if your spending power increases every month there is no urgency to make big purchases) and out of the decade-long struggle with low or no inflation. The current rate is at 4%, a level not seen for over 40 years, and above the 2% target of the BoJ; however; this is not viewed as sustainable given the transitory impact of higher energy costs.

The bank will be closely watching the so called ‘Shuntō’ period (‘spring wage offensive’) for signs of wage growth, which has not been as strong as in other regions, coming through to embedded inflation around the 2% sustainable target level. Only then will we likely see a change in policy.

The Bank of Japan may also be less willing to significantly change policy direction until April, given the upcoming retirement of governor and creator of the current policy Haruhiko Kuroda. However, there was an unexpected tweak to the yield control policy in December, which widened the YCC band (by 0.25%). Even after Mr Kuroda’s retirement, many analysts forecast that the headline rate will remain unchanged throughout this year, leaving Japan out of step with the other major central banks.

Elsewhere in the world, China continues to regain economic traction following the end of its zero-Covid policy, which we covered in more detail in last month’s commentary. India’s market has continued to perform well, although a scandal around losses at Adani Group is currently unfolding, demonstrating the need to have robust processes in place when dealing with emerging markets; even if India and China investing is more mainstream, this risk still needs to be considered.

We remain constructive on Japan equity, seeing many companies as undervalued compared to other regions. Elsewhere, we retain exposure to India and broad emerging market strategies in our higher risk portfolios, as well as a specific Asia Pacific allocation, which will include China.

Commodities - February 2023

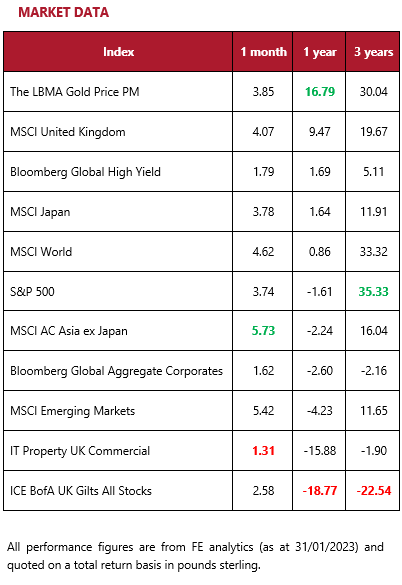

It has been a good start to the year for gold investors, with spot prices up 3.85% and the MSCI Gold Miners index up 9.23% over January. As a reminder, gold tends to perform well during periods of negative real interest rates (i.e., periods when inflation rates exceed interest rates) and investors appear to be optimistic that central bank policy will be less aggressive in 2023.

Demand for the yellow metal is not just speculative, indeed physical demand was particularly high in 2022, as central banks around the world expanded gold reserves. According to the World Gold Council, annual demand increased by 18% last year and central bank purchases hit a 55-year high. The exact reasons for this are not entirely clear but are likely deep rooted in geo-political and macroeconomic tensions.

Key purchasers over the year included Turkey, Russia, China and the Middle East, all of which could be turning away from the US, as part of a more bifurcated geo-political landscape, with those in the east turning their back on the west. The decision by western nations to freeze Russia’s dollar reserves has certainly had a part to play and so too might the current high levels at which the dollar trades.

Wedding season in India runs from November to February and gold forms a significant part of the celebrations. Gold is typically gifted to daughters, which was historically a way of sharing wealth, from a time when males would inherit the vast majority of family assets. Indian wedding expenditure is so high that global physical demand can see a notable peak during this time.

We believe there are several catalysts for gold over the next 12 months, be it a hedge against negative real rates or geopolitical risk. Its tendency to display low correlations with other asset classes makes it a key part of portfolio construction.

Currency - February 2023

Currencies are widely regarded as one of the most unpredictable assets, influenced by a myriad of factors, many of which are almost unforecastable. However, investor returns are inextricably linked to currency movements and adopting the approach of sticking one’s head in the sand is not advisable.

One theme that could be interesting over the next year could be the instability of emerging and frontier market currencies. Indeed, Turkey continues to grapple with a weaker lira and has recently unveiled a raft of proposals to prop up the currency, including rewarding businesses for holding the lira over US dollars. In Lebanon, a crippling economic crisis led the central bank to devalue the currency by 90%, causing more inflationary pressure in a country where the cost of goods rose by 170% in 2022 alone.

Pakistan has found itself in a similar boat and has been forced to abandon currency control measures, in order to push for a bailout by the International Monetary Fund (IMF). Iraq has recently sacked the governor of its central bank, following a slide in the dinar. The Egyptian pound hit fresh lows in January and it too is seeking assistance from the IMF.

In South America, the ascension of Lula da Silva to presidency in Brazil has provided a left-wing ally to Argentina.

While the two countries may be rivals on the football field, they appear closer than ever politically and announced plans to operate under a new, shared currency.

The announcement drew consternation from economists around the world and we will continue to monitor through the lens of our emerging markets equity allocations.

As we were reminded by the Arab spring, economic hardship can create significant political instability, and this is something we remain alert to. The strength of the dollar remains a major headache for a number of emerging market countries. On the other hand, a weakening of the greenback could present an opportunity for a revival in the fortunes of those who have suffered.

Responsible assets - February 2023

While 2022 saw some major challenges for energy markets, this does not appear to have slowed Europe’s transition to clean energy. For the first time ever, wind and solar generated more electricity in the European Union than any other source, which has, for now, thwarted the feared return to coal power.

Solar and wind shouldered the bulk of the energy burden, as levels of hydropower were at their lowest for at least 20 years, amid a severe drought and a backlog of maintenance issues that plagued France’s nuclear power fleet. Solar power stepped up just when the bloc needed it most, with a record growth of 38 terawatt-hours compared with 2021, thanks to a high installation rate. Wind saw a similar rise, with an increase of 33TWh compared with 2021.

While mild weather was a significant supportive factor, concerns about costs and improved energy efficiency measures were also helpful in reducing dependency on traditional forms of energy. It is early days but 2023 is on track to be even cleaner than last year. Just 28 days into the year, the EU was already down 37% on gas generation. As we wrote last year, the energy crisis has in part proved to be a catalyst for the energy transition.

Did you know you can have a windfarm wedding? For instance, Whitelee Windfarm Centre in Scotland can be hired for a wide range of events including meetings, corporate functions and yes, even nuptials.

Across portfolios. We invest in companies that are helping to facilitate the transition to a more sustainable economy and benefiting from Government initiatives to promote renewable energy.

Fixed income - February 2023

After nearly a decade in the doldrums, fixed income is coming back into style. Thanks to rising interest rates across the globe to quell runaway inflation, bonds now offer attractive yields. While the apparent peak in interest rates makes us tentatively more positive on equities, the combination of higher yields on offer and an imminent economic slowdown could provide a sweet spot for bonds. However, we do not believe all fixed income will enjoy the same gains over the year and are, as always, advocates of being scrupulous in terms of asset selection.

In the government bond space, we like both US Treasury Bonds and Emerging Market Debt. We have seen a repricing that has brought US Treasuries back to fair value and the move away from concerns over rising inflation to slowing growth is supportive of government debt. Emerging market debt (EMD) has enjoyed a strong start to the year, as there are signs the US dollar has peaked as well as real yields presenting selective opportunities. A weaker dollar is typically supportive for EMD as it alleviates governments’ financial constraints and fiscal positions as much of their debt is denominated in US dollars.

Market dispersion has increased in the credit market. We maintain a preference for higher quality debt and are keen to avoid highly leveraged names, as we see corporate cash balances decreasing and earnings concerns persist. We remain particularly cautious on the high yield space because we expect an increase in the default rate over 2023.

We have to assume that the 1919 American silent film ‘Bonds of Love’ is a not a romantic drama about debt securities. However, we may never really know as the film, which was distributed by Goldwyn Pictures and starred Pauline Frederick, is now considered lost.

While we have increased our fixed income exposure in portfolios, we have done this selectively, with a preference for US government debt and investment grade credit.

The Monthly Market Commentary (MMC) is written and researched by Simon Gibson, Richard Smith, Scott Bradshaw, Jonathon Marchant and Lauren Wilson for clients and professional connections of Mattioli Woods and is for information purposes only. It is not intended to be an invitation to buy, or to act upon the comments made, and all investment decisions should be taken with advice, given appropriate knowledge of the investor’s circumstances. The value of investments and the income from them can fall as well as rise and investors may not get back the full amount invested. Past performance is not a guide to the future. Mattioli Woods is authorised and regulated by the Financial Conduct Authority.

The MMC will always be sent to you by the seventh working day of each month, usually sooner, is normally delivered via email, and is free of charge as the MMC is generally made available to clients who have assets under our management in excess of £200,000, and to all clients under our Discretionary Portfolio Management Service (DPM). Normally, the MMC costs £397 + VAT per annum. Professional advisers and their clients should contact us if they are interested in receiving a monthly copy.

Sources: All other sources quoted if used directly; except fund managers who will be left anonymous; otherwise, this is the work of Mattioli Woods.