Global market summary - February 2024

The ‘almost everything rallyʼ that market participants enjoyed over the final few months of 2023 was not carried into the new year. Performance across asset classes was mixed in January, while select areas of the equity market eked out gains, core government bonds reversed some of last yearʼs gains as market participants scaled back the number of rate cuts priced for 2024.

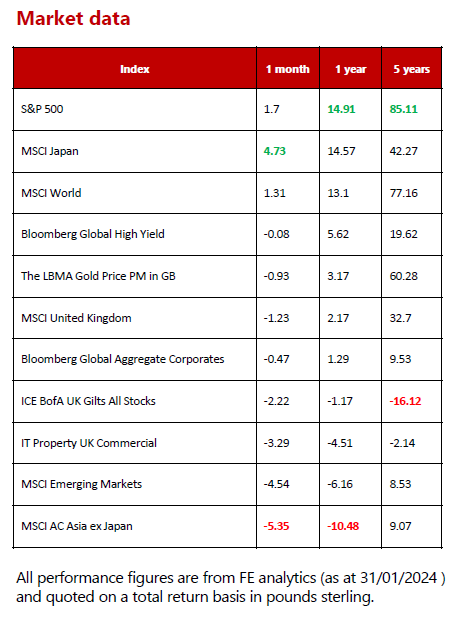

Developed markets continued to outperform emerging markets over the first month of 2024. The major US indices ended the month in positive territory still driven by mega cap technology companies, European equities also made gains on a flurry of encouraging corporate results, while a weaker yen supported Japanese equities. Despite a mid-month bounce, Asia Pacific (ex- Japan) equities remain the laggard as market participants retain a degree of scepticism around the potential efficacy of Chinaʼs recently announced additional stimulus measures.

Commodities performed well (led by oil) as prices rallied amid worsening tensions in the Middle East and disruption to shipping through the Suez Canal continued. Drone attacks on Russian infrastructure added to the uncertainty in the global energy market. The situation increases the risk of supply chain disruptions, but while shipping costs have increased, the total impact is far lower than the fully fledged disruption seen during Covid-19 lockdowns.

Closer to home, checks on EU goods coming into the UK on animals and plants have now come into force, potentially adding time at the border for imports. There also appears to be positive progress on arrangements on Northern Ireland, which may see the devolved administration return. The former two are both examples of potential bumps in the otherwise downwards trend of inflation but these are not predicted to be major.

Although spring may feel a long way off amid the relentless grey skies, wind and rain, February has us looking ahead to brighter days. As we look forward to the rest of 2024, we believe this year will mark another step towards a return to the prior low growth/low inflation regime following the large swings in demand and inflation experienced in 2021 and 2022.

While the destination looks clear, the journey itself might continue to prove turbulent as it is subject to macroeconomic developments and central banksʼ guidance, as well as political and geopolitical events. We believe that the weeks/months of short- term corrections and rallies are likely to continue until we see more clarity around the monetary policy outlook. We do however, believe that the net impact of macro, policy, and political developments in 2024 should overall be supportive for both bond and equity markets.

We have been actively positioning the portfolios to reflect our more constructive views on developed market equities and fixed income, increasing exposure to both areas while reducing alternative assets such as infrastructure, real estate, and more costly hedge- fund-style strategies.

United Kingdom - February 2024

UK equities started the year in negative territory, with the MSCI UK All Cap index down 1.34% over January. As a reminder, November and December had been strong months for the domestic market, predominantly down to hopes that interest rates would be cut sooner than expected. Inflation data in January tempered the excitement of UK investors by coming in marginally higher than expected. This was compounded by a slump in the oil price, weak retail sales data and several profit warnings from companies.

A profit warning is an announcement by a company that its earnings are likely to be lower than expected. Share price reactions tend to be ugly and it is not uncommon to see 20%+ falls on such news. The difficulty for UK investors is that companies have been issuing profit warnings all too regularly.

Indeed, data published by EY-Parthenon showed that 18.4% of UK-listed companies issued profit warnings in 2023. This compares to 17.7% seen during the peak of the financial crisis of 2008. What is clear from the data is that higher inflation and higher interest rates have caused problems for companies. In fact, increased costs of labour, materials and debt payments accounted for nearly 40% of profit warnings, and delays in decision making from customers were attributable for 25%.

While we continue to believe that UK equities offer long-term value, we must carefully manage our way through shorter- term headwinds. In our UK Dynamic Fund, we have taken steps to reduce our sensitivity to discretionary spending. Avoiding profit warnings altogether is almost impossible. However, by investing in companies with strong balance sheets, at reasonable valuations, we can mitigate the significant declines that can occur.

North America - February 2024

Following a strong finish to 2023, US equities had a sluggish start to January as investors started to reassess how soon interest rates will be cut across developed markets. Sentiment picked up towards the end of the month, following better-than-expected growth data and signals from the US Federal Reserve (Fed) that rates have peaked, bolstering hopes for cuts later in the year. Technology stocks continued to lead the S&P 500 index to consecutive record highs with the S&P 500 delivering 1.7% in £ terms, while an equal weighted version of the index ended the month down 0.75%

Fed officials cemented the end of their aggressive rate hiking campaign by opting to hold interest rates steady at their January meeting. While Chairman Powell cautioned that March was too soon to anticipate rate cuts, the recent flurry of robust growth and employment data has left us looking ahead to a soft landing for the US economy. In addition, January delivered some reassuring news on the struggling manufacturing sector. Revisions to the gauges of factory activity over the month beat expectations indicating the best, if still moderate, pace of growth in the sector since September 2022.

Our analysis of this data has led us to become more positive on US equities overall, believing that the artificial intelligence driven rally in US mega cap tech stocks that buoyed the market in 2023 can broaden out as inflation cools and monetary policy becomes more supportive.

In our view, until a new significant macro catalyst emerges, developed market stocks (particularly large cap quality companies with defensive characteristics) are more likely to outperform or at least better manage to weather the volatility associated with rapid markets gyrations. As such, we have been increasing our exposure to a broad range of US large cap stocks.

Europe - February 2024

European markets endured the same lacklustre start to the month as the US, with investor appetite waning across the globe. However, a slew of positive earnings, and better-than-expected economic data as well as a central bank announcement towards the end of the month supported markets, allowing the MSCI Europe ex-UK Index to deliver a moderately positive return of 0.35% over January.

The European Central Bank (ECB) kept rates on hold at its January meeting and reiterated its commitment to remain data dependent. While no clear trajectory for interest rate cuts was given, investors remain confident that rates have reached peak levels. Annual consumer price inflation continues to move in the right direction, with the headline rate slowing to 2.8% in January from 2.9% in December. The core rate, which excludes volatile food, energy, alcohol and tobacco prices, also ticked lower to 3.3%. We also learned, towards the end of the month, that the eurozone economy unexpectedly avoided a recession in the final quarter of 2023. Gross domestic product (GDP) during the period was unchanged compared with the previous three months and 0.1% higher than a year earlier, with expansions in Spain and Italy partially offsetting a contraction in Germany.

Over the month, larger companies outperformed their smaller peers, with some of Europeʼs most valuable companies in the healthcare and consumer discretionary space leading the way. Danish drugmaker Novo Nordisk notched an all- time high after forecasting another year of double-digit growth. While luxury goods company LVMHʼs shares bounced following sales figures that reassured investors about the sector’s resilience to economic headwinds, particularly in China. Luxury peers Kering and Hermes were also swept upwards in the rally.

Over January, we increased our exposure to European equities across the board, believing that markets were pricing in too much negativity around the region. The region is home to some outstanding companies with global reach that in our view is poised to benefit from near-term macroeconomic conditions.

Rest of the world - February 2024

We saw weak performance from the Asia ex- Japan equities in January driven by ongoing concerns about the Chinese economy. Disappointing retail sales and further deterioration in housing activity added to investor apprehension and, although fourth- quarter GDP figures were in line with expectations (5.2%), this is historically weak for the region. There were stimulus measures announced by the Peopleʼs Bank of China (PBOC) over the period, but market participants were disappointed by the size and scope of the measures, viewing them as inadequate to reignite activity. According to the Chinese lunisolar calendar, this Saturday we are due to enter the year of the Wood Dragon, which is said to be associated with enhanced vitality and creativity. Hopefully the Government can turn this towards economic policy for the new year.

In contrast, the Japanese equity market enjoyed a strong start of 2024, driven by large cap stocks and a weaker yen, which is beneficial to exporters’ earnings. Foreign investors led the rally on expectations of structural changes in Japan, including the launch of the new NISA (Nippon Individual Savings Account) for Japanese retail investors. Much like the British ‘ISAʼ, the scheme is aimed at incentivising Japanese citizens to invest some of the trillions of yen currently held in cash into the stock market by offering tax advantages.

Indian equity markets also eked out a modest gain over the month thanks to inflows from foreign investors, who view the countryʼs stock market as an attractive alternative to China. Most other emerging markets declined over the month on worries that the US central bank will keep rates higher-for-longer, a negative for most emerging economies.

Despite currently having a bias towards developed markets, we continue to invest in emerging markets, but we remain selective with a bias away from China (and no direct Chinese investments). We retain a position in Japanese equities that is well placed to benefit from the long-term structural growth story.

Fixed income - February 2024

In a partial reversal of the positive performance experienced over the final quarter of 2023, global government bond yields rose in January (meaning prices fell) as the likelihood of interest rate cuts as soon as March were pushed out until later in the year. Although inflationary pressures look to be subsiding across developed markets, robust labour markets and non-committal statements from central bank officials on the future trajectory of interest rates were enough to spook investors.

Despite short-term volatility, we maintain a positive outlook on government debt, given signals from major central banks that interest rates have peaked. We have deliberately kept duration within portfolios at a short-medium level given our view that rate hikes are further away than the bond market has priced in.

Investment grade corporate debt was in negative territory over January but did outperform government bonds given its overall lower duration (sensitivity to interest rates). Despite the rise in yields, we can see that several bond investors are looking past the next few months of potential volatility. The appetite for high-quality corporate debt remains high with quick uptake for new bond issuance over the month.

We maintain conviction that 2024 is poised to be a strong year for returns from both government and high-quality corporate debt. However, we expect short-term volatility in yields as market participants have become more attentive to surprises in economic data.

Responsible investing - February 2024

It is not often you read the words ‘excitingʼ and ‘legislationʼ in the same sentence but hear us out; the UKʼs regulatory body, the Financial Conduct Authority (FCA), has just released some game-changing rules and guidelines for responsible investment products.

Some of the most useful feedback we have received from clients has been around responsible investing, with some commenting that it is a confusing area and others voicing scepticism around the materiality of any positive impact. The FCAʼs sustainability disclosure regime (SDR) aims to cut right to the heart of these concerns, with rules for the marketing of investment funds based on sustainability characteristics. Once the rules are in place, the FCA will be able to review and challenge any funds marketing themselves under the sustainable umbrella and could take enforcement action where serious misconduct has taken place. In our view, this type of action is needed to encourage investor confidence in the space, which has been eroded by firms indulging in greenwashing (essentially, making exaggerated claims about their productsʼ sustainability features).

Another interesting element of the regime is the proposal for UK retail sustainable funds to adopt one of four labels to describe the fundʼs sustainability approach. This should help investors select funds most closely aligned with their aims and views. Funds without a label will not be able to market themselves as ‘sustainableʼ and will be prevented from using terms such as ‘sustainabilityʼ or ‘impactʼ in their names.

We support the introduction of a sustainability disclosure regime and have been working hard behind the scenes to ensure that our Responsible Equity Fund will be fully compliant when the rules come into force.

The Monthly Market Commentary (MMC) is written and researched by Scott Bradshaw, Lauren Hyslop and Jonathon Marchant for clients and professional connections of Mattioli Woods and is for information purposes only. It is not intended to be an invitation to buy, or to act upon the comments made, and all investment decisions should be taken with advice, given appropriate knowledge of the investorʼs circumstances. The value of investments and the income from them can fall as well as rise and investors may not get back the full amount invested. Past performance is not a guide to the future. Mattioli Woods is authorised and regulated by the Financial Conduct Authority.

The MMC will always be sent to you by the seventh working day of each month, usually sooner, is normally delivered via email, and is free of charge as the MMC is generally made available to clients who have assets under our management in excess of £200,000, and to all clients under our Discretionary Portfolio Management Service (DPM). Normally, the MMC costs £397 + VAT per annum. Professional advisers and their clients should contact us if they are interested in receiving a monthly copy.

Sources: All other sources quoted if used directly; except fund managers who will be left anonymous; otherwise, this is the work of Mattioli Woods.