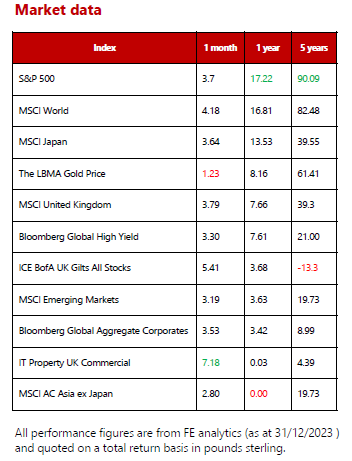

Global market summary

Firstly, a very happy new year to our all readers! January has become associated with new beginnings and the time for setting targets or goals through resolutions. Whether you are aiming for a healthier lifestyle, starting a new hobby or simply this being the year you finally get round to sorting out all the junk in the loft, the best goals are measurable and realistic. When it comes to the global economy, the key considerations continue to be inflation, the unfinished business from 2023 for central banks, and the interest rate tools used to combat this.

December frequently (although not reliably) enjoys a so called ‘Santa Clause rallyʼ for equity markets. There are many theories as to why markets frequently do well in December, including Christmas bonuses and the end of the calendar year potentially boosting returns, along with lower trading volumes as traders take holidays. For the month just passed, the positivity can more justifiably be traced to the economic data, with sustained falls in inflation figures as well as improved consumer confidence, suggesting we may not get a deep recession and that interest rate cuts (in the US) could be as early as the second quarter.

While momentum has swung in this direction, economic data will continue to trigger fluctuations in expectations and associated changes of leadership style between value and growth equities. Add in heightened geopolitical tensions in Eastern Europe and the Middle East, as well as the noise that comes with the various elections, and volatility is unlikely to be a habit left in 2023.

Elsewhere in 2024, expect political noise and potential volatility, although not all elections will weigh on markets equally. In the UK, expectations seem to be for an election in the second half of the year, with the poll having to happen by January 2025. The market so far appears sanguine about the outcome, given that the outcome is likely to result in a moderate Government (certainly juxtaposed to the Johnson v. Corbyn contest of a few years ago). The more consequential election in the US will be in November and battles in court rooms may also have a bearing on who can stand, let alone win. A plethora of threats remain, not least geopolitical risks and the delayed impact of interest rates transmitting to the real economy. Chinaʼs property market and lower trend growth may also be a headwind.

Although there are plenty of risks on the horizon, there are also plenty of reasons to be positive. Fixed income looks increasingly attractive in terms of both the coupons from bonds and the prospect of capital returns when rates are cut. There are also many high-quality businesses with resilient cash flows as well as interesting valuation opportunities in some of the more distressed areas of market for the brave.

We remain constructive on the outlook for 2024 even with expected higher volatility. There are lots of positive data points despite the threats. We remain underweight equity, neutral on fixed income (where yields look attractive) and cash. We continue to believe a well- diversified, global portfolio across asset classes is the best place to be to navigate markets in the new year.

United Kingdom - January 2024

To say that things looked ‘gloomyʼ for the UK as we entered 2023, is something of an understatement. A recession was simply a case of ‘whenʼ, not ‘ifʼ. However, the market defied the odds and conventional wisdom, with UK equities delivering a return of 8% over the year, including dividends. While this might lag the 15% delivered by global equities, it was a better result than many had expected.

Returns were delivered by a particularly strong November and December for UK stocks, owing to weaker inflation data. The areas of the market that rallied most were those worst affected by higher interest rates. Indeed, the likes of property and smaller companies staged a spirited comeback in the final two months of the year, delivering returns of 23% and 15% respectively.

While we might not have the likes of NVIDIA in the UK market, there was one stock that delivered similarly strong returns over 2023. Rolls Royce, whose shares had fallen around 70% between the start of 2019 and the end of 2022, staged a remarkable recovery. At the start of 2023, the new CEO described the business as a ‘burning platformʼ, in a stinging assessment. A cost-cutting programme, combined with ambitious targets and a rebound in global travel, helped shares to soar 222% over the year, making it a top performer in UK and European markets.

The strong performance of Rolls Royce shares serves as an important reminder as to the impact that earnings growth and expansion in valuation multiple can have on share prices. When working together, these twin engines (pun intended) can help to drive strong shareholder returns.

We continue to believe that the UK remains attractively valued, relative to other global equity markets and its own history. The Spring Statement has the potential to provide a catalyst to UK markets, particularly if the Chancellor can enact measures to increase UK equity ownership. We see plenty of exciting opportunities and remain on the lookout for 2024ʼs Rolls Royce!

North America - January 2024

At headline level, US equities had a very strong year in 2023, with the Nasdaq enjoying its fifth best year, although it is fair to say not all US equities participated in this rally. In US dollar terms, the S&P 500 returned 25.67% but using an equal weighted version of an index to get the return of the average stock, this falls to 13.17%. As we have covered before, the ‘Magnificent Sevenʼ – Alphabet, Amazon, Apple, Meta Platforms, Microsoft, NVIDIA and Tesla – have been where most of the gains have been concentrated.

Plenty has been written around the potential of artificial intelligence (AI), which has driven investor exuberance for these stocks. However, looking beneath the surface, the exposure to this nascent technology differs vastly between the seven, with semi- conductor chip maker NVIDIA arguably having the most tangible link. Tesla perhaps is the least focused on AI, while the other five are more mature businesses, which makes exponential growth more challenging, particularly against the backdrop of increasing regulatory interest. Apple experienced a regulatory headache recently around patent infringement on blood pressure monitoring, which led to a block on US sales of its new smart watches. From the fundamental perspective, these stocks look very expensive relative to peers. The market has high expectations for these names and is likely to harshly punish underwhelming earnings or unexpected issues.

Elsewhere in the headlines, the growing media circus around the US election has further gathered pace. Former President Trump has faced a litany of legal issues around whether he can run again, with Colorado and Maine both citing the 14th amendment to disqualify him, whereas other states have taken the opposite decision. Ultimately, it will be up to the US Supreme Court to decide.

Market participants will become more interested in the election as it approaches in November, and usually we would expect some volatility in sectors that may be exposed to new policies. The cost of drugs and level of regulation have both seen volatility for healthcare and financials names in previous cycles. It is worth remembering that at this stage, many proposed policies will just be for the candidateʼs political bases, and these will get watered down to try to win an election and even then, must navigate the US House and Congress, which has proven increasingly difficult over recent years.

We see returns in US equities broadening in 2024 with the Magnificent Seven stocks looking increasingly expensive and a slowing growth backdrop. The election later in the year could add volatility but also present investment opportunities.

Europe - January 2024

One feature of financial markets in 2023 was the disconnect between how the economy and equity markets behaved. That is especially true for the eurozone; the bloc has ended 2023 teetering on the brink of recession while its stock market was one of the best performing in the world. It appears investors were able to view weaker economic data through the ‘bad news is good newsʼ lens, surmising that a cooling economy should eventually lead to central bank rate cuts and a period of more supportive monetary policy. In addition, according to flow data from JP Morgan, European equities also benefited from money moving out of China and into regions viewed as less worrisome.

Data released over the year shows that higher interest rates have weighed on the eurozone economy. Eurostat data showed that eurozone GDP fell by 0.1% quarter-on- quarter in Q3, while the eurozone purchasing managersʼ index (PMI) fell to 47.0 in December. This suggests the regionʼs economy is also likely to have contracted over the final quarter of the year. This has boosted expectations that there may be no further interest rate rises from the European Central Bank and led the MSCI EMU index to advance 7.8% over Q4. Top-gaining sectors included those most sensitive to interest rates, including real estate and information technology, while healthcare and energy were the two main laggards.

Within core portfolios, we maintain a measured exposure to European equities. We blend a growth-orientated strategy and income-focused fund for the best long-term risk-adjusted outcome. The income-focused fund delivered 12% over the year, while the growth fund returned 16% with most of the positive performance coming in the final months of 2023.

Rest of the world - January 2024

We start this section by looking at Japan, which began the year with an earthquake. This most recent seismic event has thankfully not resulted in major damage; it is a testament to how prepared Japan is for these disasters that we did not see something akin to the events in 2011 around the Fukushima powerplant. While there is local damage, this was away from more key economic areas and, on opening after the new year holiday, the Japanese equity market has barely reacted. Away from the disaster, new rules on Japanʼs version of the individual savings account have come into force, with tax incentives making investing in equities more appealing than keeping money in cash, which should boost domestic demand.

China continues to grapple with its weaker domestic growth and property market issues, with 2023 being a year to forget. Reporting from the Financial Times1 suggests that 87% of the foreign investment into Chinaʼs stock market this year (no doubt hoping to benefit from the post Covid-19 reopening bounce) has now flowed out. Investor confidence remains weak and although Chinese equities look cheap, until these structural issues are addressed, we could see further declines suggesting they are cheap for a good reason.

The suggestion that other emerging markets simply rely on being the supplier to China has been challenged. Having taken different monetary policy approaches during the pandemic and not extending borrowing, many emerging markets have been able to cut interest rates. While the Chinese market was in negative territory over the year, large gains were recorded in Argentina as well as Eastern Europe (Poland, Hungary, and Romania), which were among the first nations to cut interest rates.

We continue to like Japanese equities and still see further returns to come from corporate reforms. We remain selective when investing in emerging markets, with a bias away from China (and no direct Chinese investments).

1https://www.ft.com/content/b71094b0-d974-47fb-83f2-652dd4c0d4c5

Fixed income - January 2024

“Fasten your seatbelts, it’s going to be a bumpy night.” This famous quote from All About Eve evokes many things but fixed income investing is not likely to be one of them. However, the bond market of late has been turbulent to say the least and has not provided the defensive characteristics that investors grew to expect in the four decades before July 2021. Although the final quarter of the year was a very positive one for fixed income markets, marking their best quarterly performance in over two decades, 2023 was not a smooth ride for bond investors. During the first half of the year, investors had to begrudgingly accept major central banksʼ shift in monetary policy direction to a ‘higher-for-longerʼ stance on interest rates. Against this backdrop, bonds less sensitive to interest rates (those with shorter duration, which tend to be corporate debt) outperformed, while longer dated (usually Government) bonds languished.

The end of the year marked a change in fortunes for bond investors, as easing inflation figures across developed markets led participants to anticipate interest rate stabilisation and even cuts in early 2024. As markets priced in more benevolent conditions, Government bond yields fell across the board (meaning prices rose) and despite a slowing growth outlook, the corporate bond market staged an impressive rally too on hopes that a deep recession could be averted as financial conditions eased. The question for investors now is, will the rally continue uninterrupted into 2024?

While the material increase in bond yields has improved their attractiveness versus other assets, selectivity remains important when putting together a bond portfolio. The key risk on the horizon for fixed income is that interest rates fail to sufficiently slow economic growth and inflation. While inflation is moving in the right direction, our view is that it may not continue to temper as quickly as people are starting to believe; money velocity is on the rise, which will likely delay a swift return to central bank targets. The trajectory of energy prices is another factor that could present an inflationary threat.

In the current environment, we do not need to stretch for yield and, as such, hold positions in US and, more recently, UK government bonds in core portfolios. We have supplemented this exposure with investment grade (high quality) corporate debt and emerging market debt. Our view that default rates are likely to tick up in 2024 has led us to eschew high yielding, lower quality bonds at this time.

Real assets - January 2024

Over the past few years, aggressively rising interest rates on both sides of the Atlantic put closed-ended funds under huge pressure, particularly those investing in ‘alternativeʼ, non-equity assets such as commercial property and infrastructure. We have continued to hold such assets in portfolios throughout the tumult and have been rightly questioned on this point.

We certainly will not gloss over it, 2022 and the majority of 2023 was a challenging period for these sectors. As gilt yields started to push up at the start of 2022 and rose consistently higher, it made investing in property and infrastructure relatively less attractive. This is because the perceived risk associated with investing in these assets is higher than lending to the UK Government and as such, investors expect a yield premium. In response, valuers very quickly moved down the values of properties and infrastructure assets, thus pushing the yields up.

In our view, some of the movements over this period were too extreme and presented interesting opportunities for patient investors. Looking at market fundamentals, we were reassured that rental income has remained resilient. In addition, the property and infrastructure market and most of the sectors that interact with them are in far better shape than post-2008; debt is generally a lot more conservative. In the infrastructure space, the inflation protection these assets can offer investors has largely been ignored. Most infrastructure assets have an explicit link to inflation through regulation, concession agreements or contracts. In addition, as the impact of higher rates factors into the real economy, we expect the defensive characteristics of these assets to be beneficial.

Considering the potential for interest rates to stabilise and fall in 2024, the discounts on which many of these vehicles trade to the underlying value of their assets, and the really attractive supply and demand dynamics we see in a number of areas of the property and infrastructure market, we see a great deal of upside to these holdings.

Selectivity is important; in the property space we have favoured areas with more attractive supply/demand dynamics such as industrials, care homes and student accommodation over retail and large office spaces.

The Monthly Market Commentary (MMC) is written and researched by Scott Bradshaw, Lauren Hyslop and Jonathon Marchant for clients and professional connections of Mattioli Woods and is for information purposes only. It is not intended to be an invitation to buy, or to act upon the comments made, and all investment decisions should be taken with advice, given appropriate knowledge of the investorʼs circumstances. The value of investments and the income from them can fall as well as rise and investors may not get back the full amount invested. Past performance is not a guide to the future. Mattioli Woods is authorised and regulated by the Financial Conduct Authority.

The MMC will always be sent to you by the seventh working day of each month, usually sooner, is normally delivered via email, and is free of charge as the MMC is generally made available to clients who have assets under our management in excess of £200,000, and to all clients under our Discretionary Portfolio Management Service (DPM). Normally, the MMC costs £397 + VAT per annum. Professional advisers and their clients should contact us if they are interested in receiving a monthly copy.

Sources: All other sources quoted if used directly; except fund managers who will be left anonymous; otherwise, this is the work of Mattioli Woods.