Global markets summary

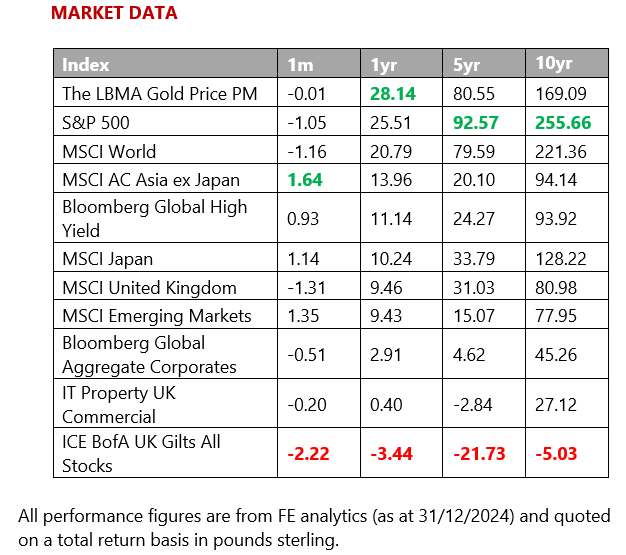

Global equity markets appeared to stumble at the last hurdle over December. While stock markets on both sides of the Atlantic saw record highs in 2024, over the last month of the year, developed market equities pulled back abruptly. The retreat was seemingly driven by end-of-year profit taking as well as a growing recognition that President-elect Trump’s policies may not be entirely positive for markets. Despite a lacklustre finish, we should note that US equities led global stocks higher over the year as the S&P 500 delivered just over 25% to £-based investors for 2024. The S&P 500’s performance stands in slight contrast to the main UK, European and Asia Pacific markets as, although they ended in the year in positive territory, most made single-digit gains.

Although 2024 experienced more than its fair share of geopolitical events, it was generally a good year for investors, with most asset classes delivering positive returns. This was thanks largely to a resilient economic backdrop, particularly in the US. Overall, risk assets (i.e. equities) outperformed, while in the fixed income space, yields continued to rise over 2024 as expectations for major central bank interest rate cuts were continuously scaled back. Corporate debt outperformed government bonds, led by high-yield debt as investors sought higher returns in a low-growth environment.

We greet 2025 with an optimistic yet balanced outlook, aware that two years of gains and a broadening market suggests a lot of good news is already priced-in to a growing number of stocks. Over December, we acted within our core multi-asset funds to reflect these concerns by raising cash to 6%, taking profit from outperforming areas. We do, however, continue to see enough appreciation potential across individual companies to maintain a constructive and somewhat risk-on stance, and we will deploy the excess cash as and when we see opportunities.

United Kingdom

Much like the prior year, UK equities delivered solid, but unspectacular returns in 2024. Like so many countries around the world, the UK held a general election this year. While politics tends to have a limited impact on investment markets over the long term, we cannot forget that the long term is comprised of many shorter periods, where the difference between expectation and reality over those periods can lead to market fluctuations. The expectation around the Labour Government was that the party would be pro-growth and gentle on taxes. However, following their election, their rhetoric turned negative, which combined with uncertainty around the Budget, proved unhelpful for UK equities.

From the perspective of UK companies, it is fair to say that the Budget was unpopular, with the main talking point being the significant increases in the labour costs for those with large domestic labour forces. Additionally, the higher levels of tax and increased public spending will likely do little to help growth prospects while also stoking concerns around another wave of inflation.

The Bank of England does appear to have inflation under control, but services inflation is proving stubborn and committee members are reluctant to stoke a second wave of inflation by lowering interest rates too quickly. They must balance this with recent economic data and sentiment, which has been softer than expected.

Given interest rates have not fallen as fast as expected, it is not particularly surprising that some of the biggest winners during 2024 were the banks. After a period of poor returns, they continue to benefit from elevated interest rates. Their ability to lock in higher interest rates for future years means they should continue to benefit from the current rate environment for some time yet.

While UK equities did not live up to our expectations in 2024, we see a number of reasons to remain positive on the domestic market. Valuations remain at a steep discount to historical levels and developed market peers. Crucially, we continue to see a number of catalysts for the market, namely high levels of takeover activity, share buybacks and increased political stability. Our UK Dynamic Fund continues to find a plethora of opportunities, particularly in the small and mid-cap space, which could be the greatest beneficiary from falling interest rates in 2025.

North America

Despite besting most other equity markets over the last year, US markets had a lacklustre December. It seems that the famed ‘Santa Rally’ failed to materialise this year, with the S&P 500 ending the month -2.42% in local currency terms. For sterling investors, the strength of the US dollar was beneficial, as the same index delivered -0.97% in £ terms.

There did not appear to be one main catalyst for the sudden downturn, but we can attribute the sell-off to several factors, including end-of-year profit taking and concern over the Federal Reserve’s 2025 outlook, as well as a comedown from the euphoric high following the US Presidential results, with investors acknowledging the uncertainty around President-elect Trump’s policy plans and their implications for markets.

Even taking December’s sell-off into consideration, the S&P 500 ended 2024 up over 25% following a 24% gain the previous year, marking its best two-year run of performance this century. The index has now made annual gains of more than 20% four times in the past six years. The rally has been led by a handful of mega-cap technology (or technology-adjacent) stocks, particularly those exposed to developments in artificial intelligence. Shares in chipmaker Nvidia have gained 176% over the year, while Meta, which has also bet heavily on the nascent technology, has risen 69%.

Over 2024, we saw US economic performance decouple from the other major regions and the question investors now face is whether US economic exceptionalism will remain intact into the new year. The outlook for the region is uncertain as President-elect Trump will come to office in January with his party controlling both Congress and the Senate, and commentators remain ambivalent about the economic consequences of his various policy ambitious.

Against this equivocal backdrop, we retain a neutral stance towards US equities; valuations are unambiguously high, but it is not out of the question that levels could be sustained and maybe even go higher over the short term.

Europe

European equity markets endured a challenging December. The EURO STOXX 50 index, which represents the largest companies in the eurozone, saw a slight decline of about 1.5% in local currency terms on the back of economic weakness and political uncertainty in the bloc’s largest economies.

Economic data for the eurozone released over the month showed signs of prolonged weakness, particularly in the manufacturing sector. The composite PMI (Purchasing Managers’ Index) fell to 48.1, indicating contraction. Sentiment was worsened by political instability in key countries like France and Germany. In France, budget negotiations faced significant hurdles, while Germany’s coalition government collapsed, leading to expectations of elections in the new year.

Although it has moderated over the year, inflation remains a concern. In December 2024, the eurozone’s inflation rate was 2.2%, a slight increase from 2.0% in October. This rise was primarily driven by higher costs in services and food, alcohol, and tobacco. More encouragingly, though, energy prices continued to exert a downward pressure on the overall inflation rate. The slight uptick in inflation data did, however, create concerns about the outlook for interest rates and called into question the certainty investors had around the scale and pace of the European Central Bank’s (ECB) rate-cutting path. Furthermore, US President-elect Donald Trump’s warning about potential trade tariffs on the European Union also undermined sentiment.

Despite the abundance of headwinds, we remain neutral on European equities. We believe that a considerable amount of negativity has been priced into European markets and, as such, valuations are relatively attractive, which may result in tactical opportunities arising.

Rest of the world

Like most other developed equity markets over December, Japanese equity markets experienced weakness in local currency terms. Weakness in the Chinese economy and caution about the incoming US administration’s policies, including additional tariffs, contributed to diminishing investor risk appetite. The Bank of Japan’s monetary policy meeting in December, along with expectations of an interest rate hike in January, added to the cautious sentiment in the market.

Sterling investors, however, generally enjoyed positive returns from Japanese equity markets over the month given favourable currency exchange rates. The Japanese yen weakened against the British pound, which meant that when converting their investments back to sterling, investors benefited from the currency movement. While domestic consumption and capital investment remained firm over the latter half of the year, external demand, particularly from China, continued to be weak, leading us to remain neutral on Japanese equities.

The MSCI Asia Pacific ex Japan Index experienced a slight decline of 0.2% in local currency terms over December. While some sectors (such as technology and financials) showed resilience, others like manufacturing and consumer goods faced challenges due to supply chain disruptions and fluctuating demand. Performance varied across different countries within the index; markets in Australia and South Korea performed relatively better, while those in China and India faced more significant declines.

November activity data pointed to the uneven nature of China’s recovery amid a looming trade war with the US. Retail sales expanded a below-consensus 3% from a year ago, down from October’s 4.8% rise and highlighting Chinese consumers’ unwillingness to spend. However, industrial production was a bright spot, rising a better-than-expected 5.4% from a year earlier amid demand for robots, passenger cars, and solar panels.

We maintain a neutral outlook on Asia Pacific and emerging market equities. While recent measures to expand the Chinese economy into higher value‑added sectors, including electric vehicles and semiconductors, will help diversify their economy in the long run, the faltering property sector will likely need a much larger renovation before it turns around, and the recent policy easing measures from the People’s Bank of China were underwhelming.

Fixed income

It was a tough end to the year for developed market government debt, as concerns about persistent inflation on both sides of the Atlantic led to rising yields and falling prices for intermediate and long-term bonds. In the UK, the Bank of England’s (BoE) decision to maintain interest rates at 4.75% amid rising inflation and stagnant economic growth led to higher yields on government bonds, as investors demanded more return for holding them.

While the US Federal Reserve (Fed) implemented two 25-basis-point rate cuts in November and December, the overall cautious tone of Fed officials created uncertainty in the bond market. The uncertainty around how growth and inflation dynamics will unfold and the impact of Donald Trump’s presidency on these factors led to rising US bond yields. The Fed will likely find itself walking a tightrope next year ahead of Trump’s administration kicking into gear, and we could see central bank policy divergence as we move through 2025. Central banks will all have to run their own race, and keeping pace with each one will be part of the challenge for fixed income investors in 2025.

Performance was mixed in the corporate debt space, with high-yield debt outperforming investment grade credit, which delivered subdued returns over the month as investors grappled with inflation concerns and cautious monetary policies from central banks. High-yield bonds performed relatively better, benefiting from shorter maturities, which means their individual bond prices are less sensitive to interest rate change.

Within the fixed income space, we retain a preference for short duration (less sensitive to interest rate changes) and high-yield debt, which has served us well this year. Encouragingly, a major macroeconomic shift is not required for bonds to perform well over 2025 given that starting yields are currently above their 20-year average in most sectors.

Ask us anything

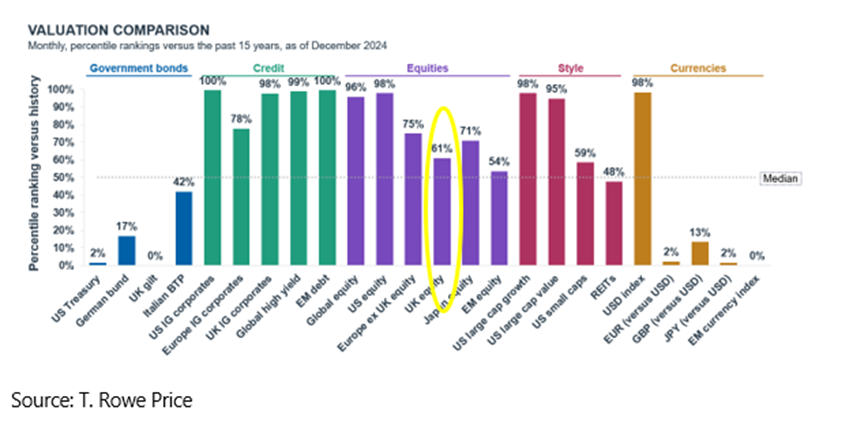

Q: After reading last month’s market commentary, I note you are more ‘positive’ on UK equities while you are ‘neutral’ on US despite acknowledging the problems facing the UK economy, can you clarify your reasoning here?

A: We believe there are a number of fundamental reasons supporting our positive view of UK equities. We continue to find it a compelling argument that UK equities are currently undervalued compared to historical and international standards (see chart below). In our view, this presents an attractive opportunity for investors looking for value as well as a margin of safety against future losses. There is also an expectation of continued corporate activity in the form of mergers and acquisitions in the UK, as the low valuations of UK companies make them attractive targets for strategic and private equity buyers.

In addition, the UK market offers attractive dividend yields, with many companies now engaging in share buybacks. This not only provides income to investors but also supports share prices by reducing the number of shares in circulation. The structure of the UK market also looks attractive, having a good balance between cyclical and defensive sectors, which can provide resilience in various economic conditions.

Despite the broad discontent investors and business owners have registered for the recent Budget, the reduction of political uncertainty following the general election in July 2024 has created a more stable environment. Additionally, the Bank of England’s recent rate cuts and a slightly improved economic growth forecast for 2025 contribute to a supportive backdrop for equities.

We do, however, accept that risks to our view remain – tight labour markets could keep wage inflation stubbornly high – and that fiscal consolidation may need to be accelerated. This is why our overweight to the UK market is marginal.

It is also key to note that when we say we have a ‘neutral’ stance to a region, we mean neutral in relation to each of our multi-asset funds’ own benchmarks. For instance, despite our positive stance on UK equities, US equities account for the largest portion of all the funds’ equity components, with our multi-asset Balanced Fund having around 27% allocated to US stocks at neutral.

If there is a question you’d like to pose to our team, please reply to this email or write to [email protected]

The Monthly Market Commentary (MMC) is written and researched by Scott Bradshaw, Lauren Hyslop and Jonathon Marchant for clients and professional connections of Mattioli Woods and is for information purposes only. It is not intended to be an invitation to buy, or to act upon the comments made, and all investment decisions should be taken with advice, given appropriate knowledge of the investorʼs circumstances. The value of investments and the income from them can fall as well as rise and investors may not get back the full amount invested. Past performance is not a guide to the future.

Mattioli Woods is authorised and regulated by the Financial Conduct Authority.

Sources: All other sources quoted if used directly, except fund managers who will be left anonymous; otherwise, this is the work of Mattioli Woods.