United Kingdom - June 2021

Our theme this month is competition. Is competition all about winners? Does anyone ever remember the runner up? Does competition matter, whether in sport, business, the world of finance/investment or simply in life? We stand on the cusp of the (normally four-yearly) Olympics, we see competition for the consumer pound/dollar/euro etc. fiercer than ever, there are a plethora of options vying for investor money (more than ever, which does not necessarily make it better), and we have a new competition for and between vaccines thanks to the Covid-19 pandemic. It is fair to say that in some of the above, winning matters more than it does in others.

In the UK we love a competition … and the stock market is no different. Every listed asset (equity) is in competition for investor cash. One difference to some elements of what we see as ‘normal’ competition is that there can be many winners. For example, if you run a listed business and investors take kindly to what they see, cash can/does flow into your shares. You do not have to receive the most cash, or see your shares rise as much as others, to consider yourself a winner here.

Globally, the UK stock market would not be seen as a winner in the last 15 months or so. Some individual equities have performed exceptionally well, of course, but as an index, the main (largest 100 stocks) index has been a laggard in comparison. So what else is happening locally?

The inflation ‘spike’ in April (up from 1% year on year in March to 1.6%) has been well signposted, and while we fully expect higher rates again in the coming months, we remain comfortable that the UK is in a good place on this measure. Economically, we also know that the economy here has suffered at least as much or even more than many other developed economies globally. With such a high level of vaccine delivery here, this could also supply a solid base on which to build.

A wet May has not helped the UK’s retail and/or hospitality industries to recover as strongly as they might have hoped, but the promise of a further reduction in restrictions later this month does bode well. The extent to which that bounce in GDP is factored into equity markets remains to be seen. The UK looks decent value relative to others, and we are investing accordingly.

Term or word(s) to watch: China – yes, we know, this seems odd, as everyone knows about China … but for many reasons, we do believe the Middle Kingdom, the factory of the world, the likely source of the Covid-19 pandemic and with a fascinating (and long) history of invention, might spend even more time in the news in the coming months. China, at turns modern and ancient … and under pressure.

First, President Biden has given his intelligence community a challenge – redouble efforts to investigate the origins of Covid-19 … and report back in 90 days. Then we have the ongoing issue of the Uyghur population … and environmental pressures both internally and externally.

Add in slightly more historic dramas around the likes of Huawei etc. and it is easy to see that China remains a headline grabber. So important, globally, expect much more to be written and said about China in the coming months.

North America - June 2021

Valuations remain an obstacle for many (including us) when it comes to the US. If one uses the CAPE measure (a cyclically adjusted measure of price/earnings multiples), the S&P 500 is trading at close to 37× earnings, which is enough to bring one out in a cold sweat. Historically, returns for the following decade from such a starting point are disappointing at best. Of course, this does not stop those advocates for the US continuing to provide reasons why things are ‘OK’.

So much of the main US index is, if not technology in its pure sector classification, then at least digital in some way, fundamentally harnessing technology in their models to achieve rapid growth. Indeed, a lot of consumer discretionary businesses fall into this category. Of course, there could have been a paradigm shift and if you want growth names, these are the businesses that will achieve it and the sorts of valuations you will have to pay.

However, that does not explain away the vulnerability to style rotation as investors reassess value stocks. Of course, if the inflationary winds that have concerned many do show some signs of easing – China’s measures to calm the commodity markets would be an example of how this could happen – then growth may return to the ascendancy and the US may look better positioned style-wise than any other market.

We have heard a lot about the possible challenges to large tech companies from antitrust probes. Antitrust laws are pieces of competition legislation aimed to protect customers from predatory business practices. The Sherman Act, the Clayton Act and the Federal Trade Commission Act make up the core of this legislation in the US.

Can we really justify these valuations and, more importantly, even if we can get close to doing so, can we justify extensive exposure to the US market as a whole? We still think not and maintain the focused thematic approach. Positioning somewhat further away from pure growth where we do have generic US exposure for adventurous clients is a step we may take, but overall, our methodology is unchanged.

Europe - June 2021

Data from Deloitte Access Economics has suggested that since Covid-19 struck, the average size of the OECD countries’ economies is 2.7% smaller. Only six countries have grown and while China and South Korea might be expected – given the earlier impact there, which has seen the nations further along with their response – Lithuania and Romania are perhaps more surprising to see on this list and ones that rarely feature in our commentary.

Both Eastern European countries had been growing rapidly before the pandemic, especially with their technologies sectors. Illustrating this, last month, Lithuanian second-hand online clothing marketplace Vinted raised a further €350 million in equity capital, valuing the company at €3.5 billion, continuing the growth of the country’s first so-called unicorn company (a start-up valued at over $1 billion when it first comes to market). Romania has also been challenging traditional Asian destinations like India for IT offshoring and has a strong depth of highly educated workers.

German swimmer Franziska van Almsick has the distinction of having won the most Olympic medals without having won a gold, having four silver and six bronze medals. The swimmer also held the world record for 200 metres freestyle (long course) from September 1994 (bettering it in August 2002) for over 12 years, until it was beaten on 27 March 2007 by current holder Italian Federica Pellegrini. This record stood only for one day with France’s Laure Manaudou improving the time. Pellegrini would reclaim the record in August of that year and went faster still four times, with the current record set in July 2009 and perhaps now unlikely to be beaten following the banning of hi-tech swimsuits.

Inflation in the eurozone increased to 2% in May, from the 1.6% reading in April, exceeding the target of below (but close to) 2%. As with elsewhere, the debate on whether central banks should act or let the economy run above target continues.

The language used by the European Central Bank (ECB) has suggested they see this as an issue of temporary rather than structurally higher prices. Looking through the data, a 13.1% increase in energy prices has been one of the most significant drivers, and this will fade over time as the energy price crash of 2020 moves out of the starting data.

There also seems to be little sign of wage growth, which might also signal higher structural inflation, despite the reopening of service elements of economies. Supply chain issues are also likely to impact the short-term numbers, with the shortage of parts and logistics issues still impacting the data, but likely to improve over time.

As with elsewhere, Covid-19 has not been dealt with, and variants and regional lockdowns remain a significant threat to the European economic recovery. Inflation has spiked higher, and most signs suggest this is temporary; however, should this become structural we might see an ending of accommodative policy from the ECB, which markets are unlikely to react positively to. We own selected European companies in our portfolios, via well-researched funds.

Japan - June 2021

We deserve a bit of escapist joy after the misery of the last 15 months. For some, that comes in the form of sport, but it appears that the Tokyo Olympics are under threat. Public opposition to the event going ahead is growing and several leading media publications have also come out in favour of cancelling for the second year in a row. Positive noises in recent days cannot paper over the issues. As sports fans, we hope there is a way for this festival of competition to go ahead; we will know soon enough.

Japan’s economic output fell more than expected on an annualised basis to the end of March 2021, which some are blaming on a less than rapid rollout of vaccines. Many of the country’s largest cities are still operating under Covid-19 related restrictions. Some analysts are now expecting that downgrades will have to be made to full year GDP forecasts and there is concern that the bounce back is going to be much weaker here than elsewhere.

Interestingly, vaccine development in Japan came to a halt several decades ago after a court decision that left the government potentially exposed to side effects of inoculation programmes. This has led to a reliance on other countries and the process for approving vaccines in Japan is also much more cumbersome than it is in the US and Europe.

There may well turn out to be no Olympics, but there is still the glamorous and ultra-competitive world of Sumo! There are apparently 82 acknowledged/official ways of winning a sumo bout (called ‘kimarite’), the exact one used being announced immediately following the fight outcome. The most common technique is Yorikiri – where the attacker drives his opponent backwards while constantly holding onto his mawashi (don’t ask).

So poor vaccine progress, a possible lost economic mini-boom from an Olympics’ cancellation – what about some positives? Well, Japan still offers global leading companies in several sectors and plenty of opportunities for investors. Crucially, a lot of negative news is priced in, and the market remains undeniably cheap compared to most peers. The UK has rallied in recent months after its own ‘unique’ challenges, leaving Japan as perhaps the most attractive developed market on valuation grounds.

Yes, there may be difficulties posed by the effects of Covid-19 and apparent policy shortcomings, but if you were choosing between Japan and, say, India and assessing which would better weather the storm, you would probably go with the former.

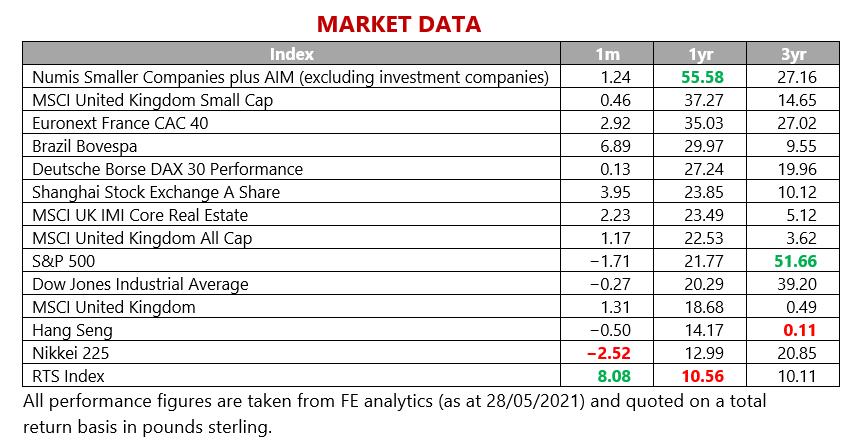

Positions remain unchanged. We allocate to Japan believing we will see decent returns medium term and recognising that, while hardly a basket case when it comes to equity returns in recent years (see the Market Data table later on), value remains.

Asia Pacific - June 2021

In the Europe section we mentioned six countries’ economies were bigger than they were at the start of the pandemic. Along with the four we mentioned, Australia has also returned to its pre-pandemic size. As well as being able to control Covid-19, commodity prices have been beneficial, particularly iron ore exports to China, which, despite diplomatic tensions, has few other supply sources. (For completeness, the sixth country is Chile, which has benefited from higher copper prices, but is under threat from a recent surge in Covid-19.)

The momentum behind Australia is somewhat under threat by further regional lockdowns to control variants, including in Victoria, the second most populous state, which is currently in its fourth lockdown that will last until 10 June. Progress on rolling out vaccines has also been very slow, with just 2% of the country fully vaccinated compared to around 44% in the UK.

Elsewhere in Asia, Taiwan’s bicycle makers Giant and Merida have both seen extremely strong demand for parts and bicycles. Giant now generates 30% of its revenue from electric bikes (known as e-bikes, and not just in Yorkshire). This surge in demand has been caused by people being forced to stay more local and exercise during the pandemic.

While this has been positive in the short term, it also represents another example of global supply chains being stressed (following on from the semi-conductor issues we covered in our last Commentary). Such has been the increased demand that some high-end parts (such as those from Japanese manufacturer Shimano) have a waiting time of over 400 days (even with the firm operating at full capacity). This supply shortage is potentially inflationary as parts are priced for rarity.

It does, however, seem this demand spike is temporary. Bikes last a long time and in a more normalised environment this initial surge will fall away and supply chains should normalise. It has also seen brands look at more local manufacturers rather than rely on the global leaders. This has not just been seen in bikes. It could potentially be a more permanent inflationary force, or at least see an easing of the disinflationary forces of globalisation from the last 50 years.

Economic data from Australia is positive but fragile. Supply chains in Asia have been stressed by the pandemic and supply shortages could be inflationary globally, both temporarily (given supply shortages) but potentially longer term if supply chains are restructured. We remain constructive on the outlook for Asia.

Emerging Markets - June 2021

It was interesting to see China‘s currency reach its highest level against the US dollar for three years with the renminbi now up 10% in a year. Foreign capital flows into the country have been substantial as the recovery from Covid-19 has gained pace, but this creates challenges for the Chinese leadership. China already faces challenges over rising commodity prices (note some of the recent crackdowns on speculation and monopoly activity in the sector) and asset price bubbles, which have the potential to be very destabilising.

The leadership is showing signs of being active in controlling the potential excesses – not just over commodities but also cryptocurrencies. The strong renminbi softens inflationary pressures, but it also makes things more difficult for China’s exporters as their goods become relatively more expensive for overseas buyers.

Emerging markets as a whole are going to need this strong recovery to continue. There are vulnerabilities across the globe and each one faces its own unique challenges.

As investors seek returns from sources that are less correlated with developed markets, some are starting to look at frontier markets. This is probably even truer in the fixed income space than it is in the equities arena. Here, of course, the higher risks bring significantly enhanced yields.

If emerging market local currency bonds might be expected to bring an investor 5%, frontiers could be running at almost twice that level, which is enticing many institutional investors who previously would not have considered the space.

Some of the emerging countries of the world also feature some interesting competitive sports among their national pastimes. Sepak takraw hails from Southeast Asia and is a form of volleyball played with the feet rather than the hands. In Myanmar it is often viewed as an art form rather than a sport as there can often be no opposing team (!) and the objective is to keep the ball elevated in an artistic and interesting manner.

We do have some frontiers equities exposure in more growth and adventurous portfolios as part of the broader emerging market piece and we acknowledge the opportunities there – as always, caution is the watchword.

Spotlight on Agriculture - June 2021

Agricultural commodities are not being left behind in the rapid ascent of commodity prices, which must make some consumers wonder how it is possible that this will not translate into higher inflation at some point. Bloomberg’s Commodities Agricultural Sub-Index is up over 20% this year with cash receipts at US farms as high as they have been in almost a decade.

The price rises have been broad as well as swift – with everything from corn to live hogs seeing rises. Some of these increases have been exacerbated by the effects of the La Niña climate cycle last year that added supply restrictions to the mix. Whether these rises are sustainable or not is of course a completely different question.

A lot of food producers were caught out by the outbreak of Covid-19 and are actually running higher stock levels, so the effects of the demand side dynamic on prices may be subdued after the initial spikes. Long term, the Food & Agriculture Organisation’s index of food prices has actually hardly moved in over half a century. This is not to underestimate the short-term effects of price increases though – they can have devastating impacts on societies and shape political outcomes across the world (the Arab Spring and Modi’s ascent in India are arguably examples of this in practice).

Talking of competition, agriculture is often cited by economists as an example of a perfect competitive market. Production is widespread geographically with undifferentiated products and individual producers having no control over prices. This dynamic drives prices down to a level that covers the cost of production with only a small scope for profit. This is the theory at least!

There are some truly fascinating investment opportunities in the agriculture space – many of which have a technological skew – and we achieve some exposure through one of our thematic environment funds that has a clean economy focus. Other than this, agriculture is not yet one of our core thematic ideas although we continue to monitor and analyse the space.

Fixed Income - June 2021

Market chatter around inflation persisted over the month of May. Investors retain a laser focus on signs that the US economy is running ‘hot’. Indeed, year-on-year and month-on-month numbers have produced some elevated Consumer Price Index (CPI) prints in the US as well as in the UK. The fact that US inflation jumped to its highest level in 13 years thoroughly spooked investors, concerned that we may see an end to zero interest rate strategies sooner than expected.

Investors are sensitive to the risk that a higher inflation reading will result in contractionary monetary policy as the Federal Reserve (Fed) tries to dampen down economic growth.

Despite valiant efforts by Fed officials to assuage markets, the fear that the Fed may have to consider pulling back some of their crisis support for the US economy persisted throughout the month. For their part, Fed officials have repeatedly stated that monetary policy will remain accommodative and insisted that they could tame inflation, if necessary, without throwing the economic recovery off track by engineering a ‘soft landing’.

While we do not, at present, forecast inflation or other indicators, we do recognise that inflation and inflationary pressures have increased. The situation now is essentially the inverse of what we saw a year ago when pandemic shutdowns were beginning, which caused an anomalous period of deflation. Oil prices, for instance, plunged at the start of the pandemic because there was an oversupply. Prices are now more or less returning to pre-pandemic levels, but the irregularity of the pandemic is distorting the overall picture.

It is also key to remember that the Fed’s inflation target has shifted to allow an average of 2% inflation. There really is no clear end in sight as there has been no indication of how long the Fed intends to average. Remember the point – inflation is always year on year … and a year ago things were pretty dire – as this year progresses, we expect inflation (UK and US) to fall back from highs (probably next two to three months) towards those 2% levels.

In the UK, the Bank of England (BoE) announced it intends to keep the interest rate on hold at a record low of 0.1%. The BoE will also be maintaining the size of its quantitative easing programme at £895bn, while the weekly pace of gilts (UK government bonds) to be purchased was reduced to £3.4bn per week – the BoE stressed that this is purely operational rather than a change in policy. The BoE also painted a benign outlook for inflation and appeared to be in no hurry to start thinking about higher interest rates.

It still appears likely that the timescale for a hiking cycle to begin will not be until 2023 at least. In the eurozone, ECB President, Christine Lagarde, continues to insist that it is ‘way too early to think about long-term policy’. The message from developed market central banks is clear: we ought to expect lower rates for longer. This really matters for fixed income investors.

In the corporate bond space, there is an unabated thirst for credit in almost all currencies. This was evidenced by Amazon’s oversubscribed raise of $18.5bn of debt across bonds of eight different maturities at the beginning of May.

As one of the ‘winners’ of the past year, Amazon does not appear to urgently need the cash but has been tempted by cheap money. Spreads have fallen dramatically since the Fed stepped in to shore up the corporate bond market in the face of a severe sell-off caused by the Covid-19 pandemic.

Now, average levels are below those from before the pandemic struck, making it a very attractive time for companies to borrow cash from investors. Amazon also set a record for the lowest spread on a 20-year corporate bond at 0.7%. While we do expect to see more companies issuing debt in this environment, we remain committed to ensuring that investors are appropriately compensated for the risk they are taking on.

We note that the current environment is not particularly attractive for a fixed income investor. We have however found some areas of value in the space such as emerging market debt and convertible bonds.

Commodities - June 2021

While many commodity investors have been getting increasingly excited about the energy transition and what this means for a number of metals, oil has been enjoying a strong rally. Indeed, at the end of May, Brent Crude prices nudged up against the $70 per barrel mark, an 18-month high. Severe cuts by OPEC and Russia enacted last year have helped to keep supply constrained but have been gradually unwound in step with a recovery in economic activity.

On the demand side, air travel remains materially lower than pre-pandemic levels and a sharp increase is likely to be supportive for the oil price. As one of the biggest consumers, OPEC policymakers will continue to follow the situation unfolding in India and the approach taken by local governments to lockdowns and the movement of individuals.

On the supply side, all eyes are on Iran and the potential for sanctions to be removed by the US. Reports suggest that the country is grappling with power outages, food shortages and inflationary pressure, all of which could spill over into civil unrest. This might force Supreme Leader Ali Khamenei’s hand on the nuclear deal and an agreement with the US could see up to 2.5m barrels of oil per day return to the market. Despite this, commodity house forecasts remain bullish, with Goldman Sachs tipping black gold to reach $80 per barrel before the end of the year.

Limiting competition is pretty much the main reason why OPEC was formed in the first place. As a reminder, the Organisation of Petroleum Exporting Countries was founded in 1960 and comprises 13 nations. Delegates from each nation meet up on a monthly basis to set production numbers and thereby influence the oil price. OPEC, therefore, provides the go-to example of a ‘cartel’ and anti-competitive behaviour for economics teachers around the world.

Oil is a key input for a number of products, as well as a vital component for inflation indicators. Though we do not have direct exposure to the spot price or related equities (though we may indirectly through our regional and thematic allocations), we keep a close eye on developments in the market and potential implications for our wider portfolios.

Property - June 2021

Incessant rainfall during April and May did little to lift the spirits of UK retailers, already battered by Covid-19 and the ongoing shift to e-commerce. Over the month of April, the British Retail Consortium reported a 40% drop in footfall, relative to 2019. Arguably the most remarkable statistic is the fact that April showed a 29% improvement on the previous month, a sign of quite how bad things had become.

The Retail Gazette reported that Central London and coastal towns were the main beneficiaries of the warmer weather enjoyed for most of the country towards the end of May. Central London footfall rose by 17% from the week before and most large cities in the UK were just short of the 10% mark.

While it is great to see people returning to the high street, there is a long way to go to repair the economic damage the pandemic has caused landlords. In its annual report to the end of March, British Land reported a 10% drop in the value of its shops and offices, equivalent to more than £1bn. Shopping centres were hardest hit, with the businesses reporting a 36% decline in values. The fall is particularly shocking considering the multi-year declines these assets had endured going into the pandemic.

Physical and online retailers are in competition and, up to this point, there has only been one winner. Those with physical stores lament the business rates they have to pay, claiming that online retailers have an unfair advantage. The introduction of an Online Sales Tax is an idea that has been floating around for some time and we may receive more clarity in Autumn 2021, when the Business Rates Review is due to be released. Others suggest that tax relief for certain commercial property related costs could be introduced.

As we have written countless times, not all retail is ‘bad’. There are plenty of high quality assets about, paying attractive and secure income. There will become a point at which shopping centres and those assets most out of favour become attractive, though we are not convinced we are at that point yet.

Responsible Assets - June 2021

In May, a Dutch district court issued a landmark ruling forcing Royal Dutch Shell to set more ambitious climate change targets. The court ordered Shell to ensure that carbon emissions in 2030 were at least 45% lower than the figures reported in 2019. After, the business announced its disappointment at the ruling and has indicated its intention to appeal. The case has wider ramifications for the corporate world. Firstly, the degree to which courts can influence corporate strategy. Secondly, the precedent that the case has set in holding companies responsible for environmentally harmful activities on the grounds that they have failed to meet their human rights obligations.

On the day the news was announced, shares in Royal Dutch Shell were largely unchanged. This suggests that either the market believes that risks of legal action are already reflected in the share price or that the ruling is unlikely to have a material impact on the business. Either way, should the case hold up after appeal, we could see a raft of cases against firms from a range of industries.

While oil is an obvious target, a number of firms in the sector have made significant commitments to reducing emissions over the past few years. Shell was something of a laggard in that respect and the case might cause others to take more drastic action. The attention of climate activists will almost certainly turn to other industries in the not too distant future, with aviation and steel likely to be in the cross-hairs.

As a society, we face the difficult task of estimating how much oil usage is too much. At the moment, there is no denying that we need it and weening ourselves off our oil dependency will take time. Some countries will take longer than others, but we must acknowledge that inaction has grave consequences for the planet.

Currency - June 2021

How many currencies does China have? Two. However, this is not straightforward … you will hear the terms renminbi and yuan referred to interchangeably. In essence, the renminbi is the official name for the currency and translates as the ‘people’s currency’ in Mandarin.

The yuan is the unit of account and the mechanism for pricing goods and services on the mainland. The yuan has smaller denominations, with one yuan equal to 10 jiao and 100 fen. The renminbi and yuan nomenclature is similar to sterling and pound in the UK.

There are, however, two separate currencies. CNY is the most widely used and its local value is dictated by the People’s Bank of China. CNH is freely tradeable, much like most other major currencies, and trades internationally. This can lead to the value of the two currencies diverging. The Middle Kingdom fascinating as ever …

UK Interest Rates - June 2021

Is there scope for surprise when it comes to UK base rates, as set by the BoE? The answer, as ever, has to be yes, but it really would be a surprise if rates were to rise short term. Despite plenty of chat and media inches on the topic of inflation, we believe the Monetary Policy Committee will continue to look through the short-term and ‘known’ issues and keep rates as low as possible to continue to support and encourage the economic recovery that is so vital for UK plc this year. Indications are that rates are more likely to gently rise towards the end of next year … and even then, possibly only back to the heady heights of c.0.75% by the end of 2023?

The Monthly Market Commentary (MMC) is written and researched by Simon Gibson, Richard Smith, Scott Bradshaw, Jonathon Marchant and Lauren Wilson for clients and professional connections of Mattioli Woods, and is for information purposes only. It is not intended to be an invitation to buy, or to act upon the comments made, and all investment decisions should be taken with advice, given appropriate knowledge of the investor’s circumstances. The value of investments and the income from them can fall as well as rise and investors may not get back the full amount invested. Past performance is not a guide to the future. Mattioli Woods is authorised and regulated by the Financial Conduct Authority.

The MMC will always be sent to you by the seventh working day of each month, usually sooner, is normally delivered via email, and is free of charge as the MMC is generally made available to clients who have assets under our management in excess of £200,000, and to all clients under our Discretionary Portfolio Management Service (DPM). Normally, the MMC costs £397 + VAT per annum. Professional advisers and their clients should contact us if they are interested in receiving a monthly copy.

Sources:

www.bbc.co.uk,

www.bloomberg.com,

Financial Express,

www.thedragonsblade.com,

www.express.co.uk,

www.pitstoppin.co.uk,

www.vr-12.com,

www.smalltalkbigresults.wordpress.com,

www.mmn.com,

www.avantida.com,

www.plazmedia.com,

www.sibcyclinenews.com,

www.viewzone.com,

www.anonw.wordpress.com.

All other sources quoted if used directly; except fund managers who will be left anonymous; otherwise, this is the work of Mattioli Woods.