United Kingdom - March 2022

It is a sombre lead this month. Despite suggestions from intelligence agencies that Russia was seriously considering invading Ukraine rather than merely bluffing, European politicians and indeed investors were far from prepared for the appalling events that are now unfolding. The word tragedy is so over-used it has almost been robbed of meaning; it is certainly appropriate here as we see a sovereign state brutalised by its neighbour.

Of course, President Putin does not acknowledge that it is a neighbouring country as such, with his recent address confirming that he doesn’t believe in Ukraine’s sovereignty. The sense of powerlessness among Western countries is real. If we do not get involved militarily in a direct way, Ukraine looks destined to be slowly destroyed despite her heroic resistance.

If we do, perhaps via the imposition of a no-fly zone, we will be effectively at war with Russia and risk testing whether Putin’s reference to nuclear weapons is a mere threat or something else. The world has united, however, in the imposition of a comprehensive set of sanctions that target individuals, the Russian central bank and ultimately undermine the Russian leadership by wrecking the country’s economy. Equity markets have been understandably shaken with safe havens such as government bonds and gold in demand, as we would expect. Usually, and callously we might argue, these geopolitical events see swift market recoveries as investors see through them, but the circumstances around this one make extra caution necessary.

We send our collective best wishes to everyone who is impacted by Russia’s attack. We also recognise that our role is not to be political, but rather to consider all circumstances that do/might impact investments, and henceforth we return here to those matters.

Where this leaves central banks and their plans is uncertain. The instability is having a significant impact on commodity prices, with Russia’s dominance in many markets meaning that disruption and sanctions create a headache for policy makers. The Bank of England (BoE) and others seem less likely to want to raise rates in an environment that could threaten the post Covid-19 economic recovery, but at the same time the rocketing prices of oil, gas and some food commodities mean that inflation cannot just be left unchecked. Some commentators were probably getting ahead of themselves talking about a return to the 1970s and stagflationary conditions, but this now looks plausible.

The Ukraine–Russia conflict creates the perfect backdrop for a downturn in economic activity and rising prices. The BoE is facing a CPI print of as much as 8% in April according to some economists and Andrew Bailey’s pleading for employees to not ask for too much in the way of pay rises seemed rather desperate.

UK GDP rose by 7.5% in 2021, which suggests we have some decent momentum (though it must be placed in the context of a 9.4% fall in 2020), but real household disposable incomes are under pressure (not least from energy prices) and things look challenged. Our stock market actually looks attractive relative to many others – the energy sector is well represented and that other significant value stock sector, financials, should benefit from a rising rate environment, though the going has been tough of late.

Sterling should hold up, especially against the euro given that European economies are feeling most pressure from the conflict, and rate rises there look less likely. Here, things have calmed down after the scandals surrounding Covid-19 restriction breaches – infuriating as they were – and all eyes are now on the much more serious events discussed above.

Our theme this month is innovations much earlier than we realise. A bit of a mouthful, but some really fascinating stories follow throughout this month. Keep smiling – it helps.

Most of us have no concept of having to leave our homes and/or loved ones and travel across our own country to a friendly border, to save our lives. Frankly, the situation is incomprehensible from a human perspective. However, our role is to comprehend the implications for financial markets and manage the assets of our clients accordingly. We continue to do this during this time of great uncertainty.

Term or word(s) to watch: oligarch – part of the sanctions response from the UK has included measures taken against Russia’s oligarchs, so plenty of action is expected on the London housing market scene and also (as we are now seeing) at a certain West London football club. Oligarchs are of course the members of an oligarchy – a form of government run by a very small group of people – usually royalty, military figures or, in Russia’s case, businessmen who essentially control a country or meaningfully dominate it politically and economically. Oligarchy itself comes from the Greek term to mean ‘rule by the few’. More measures against the Russian elite are expected, providing as they do another means of pressurising the Putin government via monetary means.

North America - March 2022

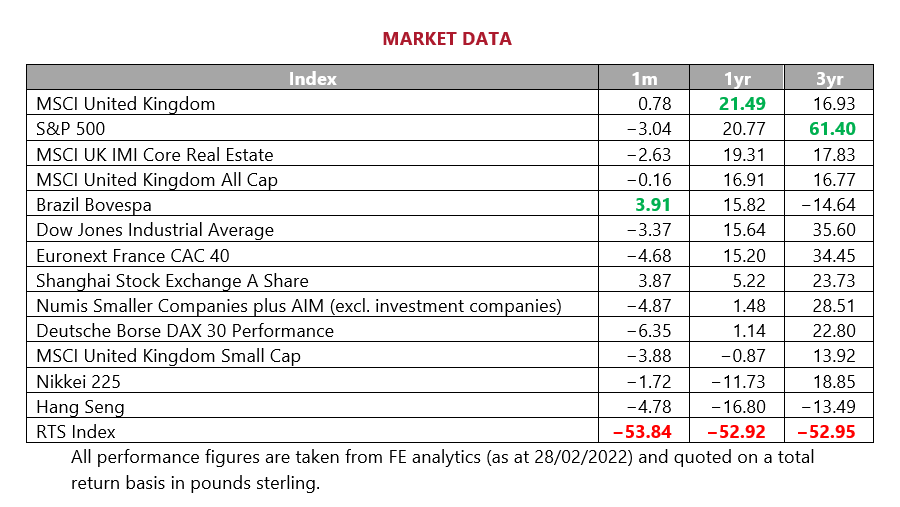

No equity market has been immune to the ramifications of the Russia–Ukraine conflict. US markets have been materially impacted and, as elsewhere, investors are nervously assessing what the prospects might be for the rest of the year. The significant representation of the technology sector makes the US index more vulnerable than others to the threat of rate rises. With inflationary pressures gathering pace, further hikes look inevitable.

This hints at probably the central issue for markets at the moment. On the one hand, we have inflationary pressures that are being exacerbated by the geopolitical strife, meaning a tightening of policy seems unavoidable. Yet at the same time, the impact on growth means that there could be a justification for not moving as quickly. Indeed, one of the concerns for many seasoned investors at the moment is that the Federal Reserve is going to tighten to such a degree that it will induce a recession. In fact, the recent Atlanta Fed survey suggested Q1 GDP fell to 0%, so further tightening looks risky in this context. A really difficult position for the central bank to find itself in – but don’t have too much sympathy as we might have expected their loose policy since the financial crisis of 2008/09 to bring the day of reckoning to bear much sooner than it has.

In a world of elevated uncertainty and market volatility the US will obviously hold some appeal over many markets. For overseas investors the dollar is likely to be seen as a safe haven at least compared to many emerging market currencies and this may protect against outflows. The switch away from tech and growth names is not entirely set in stone either remember – value areas of the market have enjoyed a strong run and the rates narrative can also go into reverse, as highlighted above.

Upwards revisions of earnings estimates may have lost some of their momentum, but corporate earnings have been decent and although this is clearly no predictor of what lies ahead, this has limited the market reaction to the challenges elsewhere. For now, the number of unknowns means that quality names are also likely to remain popular with investors as they provide some reassurance in times of stress.

The elevator was invented in the late nineteenth century. Operator-less, they caused much concern amongst worker unions. However, the Strike of 1945 and a concerted PR push meant that mass adoption ultimately took place.

The US may have some defensive characteristics in times of market angst, but at high valuations these look less convincing, and we would not be adding to direct US exposure. Themes remain our way to go here – insurance has been very helpful indeed and healthcare remains a solid long-term bet in our view.

Europe - March 2022

The European Central Bank (ECB) had an informal meeting on 24 February that was originally meant to be to discuss the timing of the ending of their bond purchasing programme, a key step before an initial interest rate increase later in the year. The events in Ukraine, however, have made the economic outlook more difficult.

In the short term, energy prices have spiked and any disruption in Russian supply, where Europe gets roughly 40% of their gas, will be inflationary. Many European companies have warned that they will need to pass on these higher energy costs to their end customers. EU sanctions against Russia will also have some direct impact on some European businesses, notably those involved in the Nord Stream 2 gas pipeline. There has also been supply chain disruption, as seen in Volkswagen where two German plants have had to idle after not being able to get electrical wiring from its Ukrainian supplier.

While the Model T was the first mass production car introduced to the world in 1908, many regard the three-wheeled Benz Patent Motor Car as the first automobile, invented in 1886. French inventor Nicolas-Joseph Cugnot had built the world’s first full size self-propelled land vehicle over 100 years prior in 1769. Originally designed to replace horse-pulled drays to transport cannons, it also was involved in the first ever vehicle accident when a prototype crashed into a Paris wall in 1771.

These factors make the economic backdrop for Europe less certain in the short term, meaning it is less likely the ECB will want to remove the bond purchasing stimulus at this time, effectively delaying rate rises even with potentially rising inflation.

Elsewhere, there have been winners with Germany’s announcement that it will be sharply increasing its defence spending with a €100 billion fund to modernise its military as well as meeting the 2% NATO defence spending commitment. The package includes replacing air force jets with new ones to be built in Europe.

Geopolitical risk has dominated the month and conflict with Russia is likely to be inflationary in at least the short term. We still like European companies even with the challenges to the European economy, but we remain watchful of the risk.

Japan - March 2022

Japanese equities were not immune from the broad falls equity markets experienced over February but, on a relative basis, Japanese markets showed greater fortitude than the majority of peers. Over February, the MSCI Japan index delivered −1.13% while the Topix, which represents Japan’s largest firms by market capitalisation, returned −0.40% compared with −2.59% from the MSCI All Companies World.

Japan was able to avoid the brunt of falls because the region has limited economic interests in Russia and is not a particularly prominent trading partner. Although some Japanese auto and wholesale trading companies do have exposure to Russia, it is very minimal and does not represent a significant part of their operations or sales.

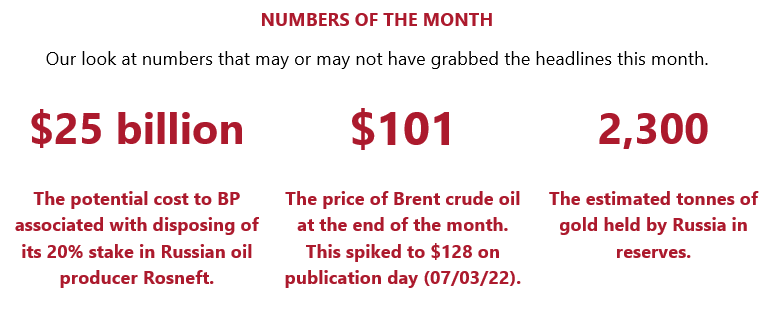

However, Japan is likely to eventually feel the impact of soaring oil and gas prices that Russia’s invasion of Ukraine has worsened. Crude oil imports from Russia accounted for 3.6% of Japan’s total last year, while the figure was 8.8% for liquefied natural gas. The further rise in energy costs is expected to exacerbate inflationary pressures that have come as a shock to Japan following decades of deflation and flat prices.

Inflation has averaged an annual 0.3% over the past 30 years but is tipped to reach 1.1% in 2022 – not eyewatering by global standards but huge in Japan. Persistently high inflation figures are fuelling speculation that the Bank of Japan (BoJ) is increasingly likely to move away from its negative interest rate policy and embark on tightening monetary policy. This would make stocks positively correlated with interest rates, namely banks and insurers, look particularly interesting.

Multinational video game behemoth Nintendo is arguably one of Japan’s best known companies, but did you know that it has been around since 1889? Proving the point that Japan has long been home to durable and innovative companies, Nintendo began its life almost a century before the Nintendo Entertainment System took the tech world by storm as a company producing playing cards (Hanafuda cards translated as ‘flower cards’).

We continue to invest selectively in Japanese equities, enjoying the diversification and exposure to quality companies it adds to portfolios.

Asia Pacific - March 2022

The signalling of central bankers in the West has been almost universally hawkish, with higher interest rates appearing likely. As we have mentioned before, this can pose difficulties for equity investors, as companies grapple with higher interest costs and the potential of a slowing economy.

Interest rates in many Asian nations are on a completely different path, with inflation generally less of an issue. Indeed, the People’s Bank of China (PBOC) has taken a more dovish stance since December, with policy makers indicating that maintaining economic stability remains a priority. This led to a 60bp cut in the reserve ratio and a trimming of interest rates by 10bps, the first rate cut since April 2020.

The year 2022 is the second year of the latest five-year plan and the Chinese government is advocating ‘common prosperity’, aimed at boosting consumption but also improving the social safety net. The two aforementioned areas give investors some forewarning as to where the next government crackdown may occur, having already targeted education and technology in 2021. Though the quality of the data is often questionable, the housing market appears to have started to stabilise, with prices broadly flat in February, following five months of consecutive declines.

It seems likely that property will remain a hot topic though and the fortunes of the sector have broad implications. Global commodity demand has long been linked to construction volumes and Chinese property debt makes up a significant portion of Asian fixed income markets. Given the reportedly vast quantities of vacant space that exist in the market, it was surprising to see the Ministry of Housing and Urban-Rural Development committing to building a further 2.4 million units this year.

The use of toilet paper has been recorded as early as the sixth century ad in China and it is believed that mass production started as early as the fourteenth century.

Higher interest rates have caused significant headaches for equity and fixed income investors, after decades of benign inflation and record low rates. Asia appears to provide a degree of insulation from the hawkish overtures of central bankers in the West, though they will of course be hurt should we see a slowing of the global economy.

Emerging Markets - March 2022

We wrote last month about the impact that geopolitical crises can have on emerging markets. Though some have suggested that contagion across the EM space would not necessarily be a direct consequence of the events in Ukraine, there are clear signs of sentiment turning negative as a result. The repercussions are being felt not just regionally in Eastern Europe, but equities, bonds and currencies across the whole complex including Latin America and Asia have also come under sustained pressure.

Many countries had built up substantial foreign reserves buffers and current account surpluses, but Covid-19 has had the inevitable effect of reducing these, leaving some vulnerable to instability or idiosyncratic risks.

Rising commodity prices are actually a negative for the space overall, for although there are clearly large commodity producers listed in some emerging markets, most economies here are actually energy consumers rather than producers.

One of our preferred options in the space – India – has vulnerabilities in this area and this perhaps explains the rather uneasy refusal from the countries’ leaders to condemn Russia’s actions in Ukraine more forcefully. Increasing oil and gas prices and also agricultural commodity price rises are going to have a disproportionate impact on developing economies.

India might be able to claim to be the birthplace of plastic surgery. The religious texts, the Vedas, perhaps 4,000 years old, mention rhinoplasty in great detail, but were they the first – who really ‘nose’?

Inevitably , there are always going to be opportunities in what is such a differentiated space, but we have gathering headwinds here and the sector is to be treated with caution. India will not find this period easy, but we are maintaining positions – China is much reduced in portfolios though we still have holdings for Adventurous clients.

Spotlight on: global dividends - March 2022

The Janus Henderson Global Dividend Study gives us insights into the levels and trends of dividend payments around the world. This year’s edition revealed that 2021 saw a very strong recovery in levels with overall payouts increasing by 17%. This is perhaps not much of a surprise given improved confidence having weathered the initial phase of the pandemic in 2020, when many corporates built up cash reserves

The year 2021 was also boosted by a large number of special dividends. Special dividends, unlike regular dividend payments, are usually one-off distributions that follow an extraordinary event. The increase in one-off payments was partly down to the reduction in built-up cash reserves, but the mining sector also played a large role. The industry benefited from the reopening of economies around the world, paying out double the previous record level. Closer to home, Rio Tinto led the way, with their 2021 financial year dividend of £12.3 billion – the second largest payout ever from a UK market constituent.

Looking ahead, 2022 is highly unlikely to see the same level of growth and may struggle to retain the same payout levels. While we would expect regular dividends to continue to recover, a repeat of the same level of special dividends is likely to return to more ‘normal’ levels.

Dividends and income can be a key part of returns for longer-term investors due to the power of compounding. We consider income as part of portfolio construction and the wider financial planning process.

Fixed Income - March 2022

The conflict in Ukraine has wide ranging implications for the fixed income sector. Clearly there are direct implications for the emerging market debt space, where both Russia and Ukraine are constituents of widely followed indices. Indeed, the two countries account for 3% and 2% respectively of the J.P. Morgan Emerging Markets Bond Index Global Diversified benchmark, which tracks a range of sovereign and state-owned enterprise bonds.

Clearly, the likelihood of default on these bonds has grown significantly and many have effectively written down the value of Russian sovereigns to zero, on the basis that they cannot be traded or settled.

High yield bonds could also endure a difficult period, with higher interest rates and inflation compounding the issues in Eastern Europe. The cost of hedging default on European high yield now stands at a multi-year high, with protection in high demand.

In the US, things are more nuanced. Investors appear more concerned by the broader macro environment, though some stand to benefit from it. The high yield space contains a significant amount of energy exposure. Clearly higher oil and gas prices help to increase profitability and reduce default risk there.

US treasury bonds have provided a safe haven for investors. The yield on the 10-year has tumbled from 2% to 1.75% since the Russian invasion and has helped to erase some of the poor performance that investors experienced during the start of the year.

The first known bond in history dates from around 2400 bc in Mesopotamia (modern day Iraq) and guaranteed the payment of grain. At that point in time, corn was widely used as currency.

We have been engaging with our managers in the emerging markets debt space to understand their exposure to both Russia and Ukraine. Exposure is low, owing to the aforementioned size of benchmark positions and prudent risk management. However, we continue our regular dialogue with these managers regarding fund flows, given that the current situation could negatively impact sentiment towards the sector.

Commodities - March 2022

Much debate has surrounded whether holding gold is reliable as an ‘insurance’ in portfolios. There are question marks over its consistency in protecting against inflation it has to be said, but Ukraine–Russia presents a setting in which we really would expect it to perform – a crisis of geopolitics and hence economies. True enough, it has been a strong performer of late, and each deterioration in news flow is reflected in the rising price of the metal.

It is true that in challenged liquidity conditions such as we are seeing emerge in many areas of the market, gold can succumb to selling pressure as investors are desperate to get their hands on dollars. Treasuries often fall prey to the same fate. Having recovered some momentum, though, gold looks very good against the cocktail of risks facing the markets, not least the prospect of stagflation that is certainly more likely as a result of the appalling events unfolding.

The disruption to the commodities space from the conflict is very real given Russia’s importance in various markets. In addition to the effect on oil and gas from the war, Russia also dominates the market in the mining of platinum and palladium where there was already no spare capacity. In the base metals arena, aluminium and nickel are also gaining with the demand–supply dynamics similarly challenged. Even something like neon, which is essential in the semiconductor industry (and is a by-product of steel manufacturing), the market is hugely dominated by Russia.

Russia is also the largest exporter of wheat in the world with Ukraine also a considerable producer, so agriculture is contributing to the inflationary impulse too. The possible weaponisation of commodities (or further weaponisation if we take the view that this has already happened with natural gas), is a real and frightening prospect for the global economy and markets.

Basic perhaps in its technology, but the Davy safety lamp was an early transformer of the mining industry. Created in 1815, it was primarily designed to allow miners to carry out their roles without the flame igniting the methane gas found in high quantities at greater depths.

All of these areas are of course able to be accessed by investors, but as we discussed last month this can be challenging to execute in practice. However, gold looks ideally positioned to benefit from ongoing volatility, improved sentiment in the commodity space and the possibility of a slowdown in growth at a time of stubbornly high inflation.

Property - March 2022

We are well into the earnings season for UK companies and we have seen generally positive numbers from REITs. The most eye-catching results have been in the industrial space, where there have been staggering increases in asset values for a number of vehicles. The likes of SEGRO and Tritax Big Box REIT posted increases of 40% and 27% respectively over 2021.

The investment case for the industrials space remains relatively simple. Online retail continues to grow, increasing the need for warehouses for storage and logistics. Crucially, consumers have become accustomed to next day delivery, which has required supply chains to evolve and led to the growth of ‘last mile logistics’, where smaller sites are used as part of the distribution network. Last mile sites need to be close to urban conurbations to ensure the speed of delivery and proper staffing. However, with a seemingly insatiable demand for residential projects, the supply of such facilities has been muted for some time.

These factors have culminated in market dynamics that favour landlords and we have seen significant yield compression in the space. What this has meant is that owners of these sites can charge higher rents when negotiating new lease terms, which in turn leads to higher property values. Indeed, we have seen some vehicles showing lower levels of retention, as they seek to ‘churn’ the portfolio and bring in new tenants on more attractive terms.

One innovation that was created much earlier than we realised was the escalator. A patent attorney from Massachusetts, US, is credited with patenting ‘revolving stairs’ in 1859. It wasn’t until 1896, under a different patent, that the first working prototype was made.

While recent NAV increases help to reduce the premiums on which some of the industrials vehicles trade, the yields on offer in some sub-sectors are staggeringly low. While we can see the growth angle and have selective exposure, we are conscious of both the potential growth from here and the relative attractiveness of other sectors.

Responsible Assets - March 2022

In 1988 McDonald’s received permission from the Communist Party to start business in the Soviet Union. When the first restaurant opened two years later in Moscow, more than 5,000 people were in attendance. It was seen as a watershed moment for capitalism and, since then, Western brands have made in-roads, albeit slowly, into Russian society.

However, a combination of the stark reality of Russia’s actions, political pressure and a greater focus on corporate responsibility has led CEOs across the world to offload Russian investments at any cost, unwinding decades of progress.

Russia’s economy has hardly been a vibrant one over the past few decades. In fact, despite its size, its GDP is smaller than Italy’s. However, it is a country that is blessed with vast resources. As such, oil is one sector with close ties to Russia.

As a result of the Ukraine–Russia conflict, BP announced that they would sell their 20% stake in oil and gas producer Rosneft, potentially taking a $25 billion hit on the transaction. Shell and ExxonMobil have several joint ventures that they are now ceasing. Outside of big oil, almost every household name imaginable has taken the decision to exit the market. Apple, Google and Facebook have scrambled to curtail their services in Russia and other major brands are suspending delivery and operations.

The reaction from the corporate world has been heartening, regardless of their underlying motives. The damage caused by the actions of President Putin may make CEOs and shareholders think twice about ties with other autocratic regimes.

Currency - March 2022

While Russia wages war in the streets and skies of Ukraine, Western democracies have retaliated with unprecedented economic measures. As we mentioned earlier, the aim appears to be collapsing the Russian economy in an attempt to force President Putin to de-escalate or, better still, spark a regime change.

The rouble nears record lows and credit rating agencies continue to cut their assessment of the outlook for the economy. Russian assets have been destroyed in value and foreign earnings there are effectively worthless. The Central Bank of Russia’s attempts to stabilise the rouble by more than doubling interest rates to 20% proved ineffective, in the wake of measures cutting off transfers via SWIFT and Euroclear. It appears that all that remains of the rouble is rubble.

UK Interest Rates - March 2022

It all seemed so certain … another 0.25% rise at the next Bank of England Monetary Policy Committee meeting looked guaranteed. Conventional wisdom was that inflation would peak soon after and the economy would have the chance to cool.

However, a lot can happen in a month. Concerns over the health of consumers and their ability to stomach rate rises have been heightened with the conflict in Ukraine. After all, what impact will a rate rise have when inflation is being driven by oil prices and oil prices are being driven by geopolitical conflict? It now looks like, compounded by a rising tax burden, UK households face a standard of living crisis.

As we outlined earlier in the Commentary, with GDP forecasts being cut and inflation forecasts seemingly trending higher, the threat of stagflation is plausible. Central bankers around the world appear to be walking a very fine line and we await the next meeting with bated breath.

The Monthly Market Commentary (MMC) is written and researched by Simon Gibson, Richard Smith, Scott Bradshaw, Jonathon Marchant and Lauren Wilson for clients and professional connections of Mattioli Woods plc, and is for information purposes only. It is not intended to be an invitation to buy, or to act upon the comments made, and all investment decisions should be taken with advice, given appropriate knowledge of the investor’s circumstances. The value of investments and the income from them can fall as well as rise and investors may not get back the full amount invested. Past performance is not a guide to the future. Mattioli Woods plc is authorised and regulated by the Financial Conduct Authority.

The MMC will always be sent to you by the seventh working day of each month, usually sooner, is normally delivered via email, and is free of charge as the MMC is generally made available to clients who have assets under our management in excess of £200,000, and to all clients under our Discretionary Portfolio Management Service (DPM). Normally, the MMC costs £397 + VAT per annum. Professional advisers and their clients should contact us if they are interested in receiving a monthly copy.

Sources:

www.bbc.co.uk,

www.bloomberg.com,

Financial Express,

www.thedragonsblade.com,

www.express.co.uk,

www.pitstoppin.co.uk,

www.sibcyclinenews.com, www.vr-12.com,

www.smalltalkbigresults.wordpress.com,

www.anonw.wordpress.com

www.avantida.com,

www.plazmedia.com,

www.viewzone.com,

www.mmn.com.

All other sources quoted if used directly; except fund managers who will be left anonymous; otherwise, this is the work of Mattioli Woods plc.