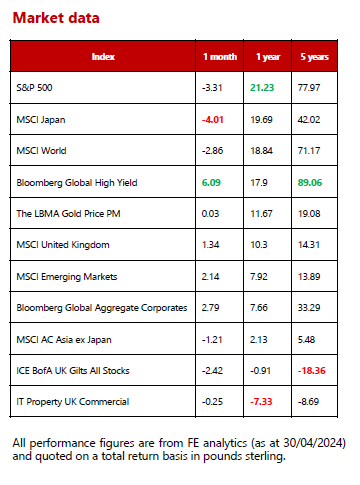

Global markets summary - May 2024

As we move through 2024, market expectations for the number of interest rate cuts have changed significantly. Over the first quarter, equity investors took these shifting expectations in their stride as well as shrugging off rising geopolitical tensions. April, however, brought about a change in tone with mixed returns from equity markets and, interestingly, a reversal of market leadership with the MSCI China, Asia Pacific (ex-Japan) and UK large cap all delivering positive returns (in £ terms) while US, European and Japanese markets lagged.

This turn in investor sentiment was primarily driven by data emphasising the pertinacious grip of inflation on the US economy. Central banks have emphasised their ‘data dependenceʼ and, unfortunately for those betting on rate cuts, that data is not consistent with interest rate cuts in the near term. The US employment and inflation numbers for March were both stronger than expected, pointing to a resilient labour market and the disinflation process stalling above the Federal Reserveʼs 2% target.

The ‘higher for longerʼ interest rates narrative drove bond yields higher (and prices lower) over the month. Areas least sensitive to interest rate expectations were the most resilient, with corporate bonds outperforming developed market government debt.

Mid-month investors flocked to safe haven assets, such as physical gold, unsettled by a significant escalation in Middle East tensions after Iranʼs drone and missile assault on Israel. Fortunately, we ended April with greater optimism around the potential for a ceasefire, which stabilised investor risk sentiment. The oil price, a beneficiary of threats to supply, ended April flat against this backdrop of easing tensions between Israel and Iran.

Last month we warned that complacency levels were elevated, and it appears that investors received a healthy dose of reality over April as the prospect of interest rate cuts were pushed out further still. However, regarding the market cycle, our view is that we remain in a disinflationary recovery, which favours equities over fixed interest. As such, any substantial equity market pull back should be seen as a buying opportunity, not the start of a prolonged bear market. Despite the recent volatility and the news cycleʼs focus on geopolitical concerns, there are fundamentally driven reasons why we remain optimistic towards a range of equity markets. We continue to favour US, European and Japanese equities ahead of China and the Asia Pacific region.

United Kingdom - May 2024

At a headline level, it was a good month for UK stocks, with the MSCI United Kingdom All Cap Index rising +2.37%. As is often the case, the headline fails to tell the whole story. While smaller companies ended the month flat, mid cap stocks suffered a -2.44% fall during the month.

Mid cap stocks typically have greater exposure to the domestic economy. Given the positive economic data over the month, we would have hoped for stronger performance. Net mortgage approvals reached their highest monthly level since June 2022 and business activity in the UK grew at the fastest pace in almost a year. Inflation fell from 3.4% in February, to 3.2% in March. While it is a step in the right direction, it was less of a fall than the market had hoped for and equity investors may be waiting for longer than expected for the interest rate cuts.

Higher interest rates are not putting off bidders and we continue to see elevated levels of takeover activity in the UK. In April alone we saw nine bids, in what looks to be like another strong year for takeover activity. While takeovers are difficult to predict, we hold a number of positions in the UK Dynamic Fund that we think may be attractive targets to private equity or trade buyers.

Crucially, we do not enter positions solely on the basis of takeover potential. We believe that the best way to generate attractive returns is to ensure they can arise from multiple different sources. Specifically, we like to see potential for earnings growth, expansion in valuation multiples and attractive dividends. If we receive the odd attractive bid along the way, then that is a bonus!

North America - May 2024

Historically, April has been a good month for US equities. Since 1950, when the US main market (the S&P 500) delivers positive returns in the first three months of the year, it averages a 1.8% gain in April. This year, however, turned out to be an outlier, with the S&P 500 finishing the month down 3.26% (in £ terms). So, what happened this year and has the worldʼs best performing market over most time periods lost its mojo?

The market pull back was largely driven by speculation around the future path of interest rates. Inflation data has continued to surprise on the upside for the past quarter, making the narrative that these surprises are all attributable to ‘one-offsʼ in individual components harder to swallow for investors. As such, markets are now bracing for policymakers to hold interest rates at historically elevated levels. While we expect this to create headwinds for smaller companies, letʼs not forget that the US stock market is home to some of the worldʼs largest companies that have already displayed incredible resilience in the face of a global pandemic and aggressive interest rate rises.

Over the month, we saw a slew of positive corporate results particularly from technology giants. According to data from Refinitiv, of the 265 companies in the S&P 500 that have reported earnings to date for Q1, 79.2% reported above analyst expectations. This compares to a long-term average of 66%. Given our current preference for resilient companies with strong balance sheets and pricing power, we view April as a temporary blip in the US equity market trajectory rather than the precipice of a sharp fall.

We viewed the pull back across US markets over April as a welcome opportunity to top up positions in US large cap stocks. We maintain an overweight position (versus peers) to US equities via a blend of large cap growth and large cap value strategies.

Europe - May 2024

European stocks recorded their first negative month since October after a flurry of earnings and data weighed on investor sentiment. Most sectors declined over April with the auto space leading the way following disappointing earnings from a number of carmakers. Healthcare stocks were one of the only sectors to buck the trend, making modest returns over the month driven by persistent demand for weight loss drugs such as Wegovy.

Despite Aprilʼs lacklustre stock market performance, the outlook for European equities continues to brighten. The European Central Bank (ECB) does not appear to be facing such sticky inflation issues as the US Fed. Eurozone CPI is now 2.4% and while the ECB held rates at 4% for the fifth consecutive meeting, they virtually promised a 0.25% cut to interest rates in June in an unusually univocal signal to markets.

We can expect further cuts over the year should the ECBʼs forecasts remain on track. Crucially, policymakers want clear evidence of wage pressures moderating and not being passed on via higher prices before they embark on a steady course of rate cutting. The combination of cooling inflation and interest rate cuts should then put the European consumer in a healthy position as real wages recover, and individuals feel less steadfast about maintaining a higher level of savings ‘just in caseʼ.

Europe is set to take centre stage in May as Sweden gears up to host the global phenomenon that is the Eurovision Song Contest. Just in the nick of time, it appears that the bloc has gone from a shameful ‘nil pointsʼ at the start of the year to a more respectable score as gross domestic product (GDP) across the eurozone expanded by 0.3% in January to March, according to statistics body Eurostat. This means the region has escaped recession and beaten forecasts for growth. So, despite weaker returns over April, we look forward to the coming months for European equities with mild optimism, given current market conditions.

We maintain a neutral position towards European equities, viewing it as a little too early in the market cycle to move to an overweight position. It is, however, an area of continuous discussion that we expect to revisit as more data is released.

Rest of the world - May 2024

Chinese equity markets have lagged most peers over the medium term, as a post-Covid bounce back has so far remained elusive for the worldʼs second largest economy. However, the region had a strong April amid tentative signs of an improvement in the macroeconomic picture as GDP growth came in at a 5.3% annualised rate for the first quarter, which was much higher than expected. This supported Chinese equities over the month with the rally extending to Asia Pacific stocks.

We maintain a degree of caution around the space, noting that consumer confidence remains weak and has not yet recovered to anywhere near pre-pandemic levels. The ongoing downturn in the real estate sector has had a profound impact on overall consumer sentiment given 60% of Chinese household wealth is tied up in property. The poor performance of Chinese stocks over the last couple of years has only exacerbated this negative wealth effect, with households increasingly less confident about their future income prospects. It is our view that the Chinese government must step up stimulus measures to repair consumer confidence and enable them to support the economy on a sustainable basis.

While we have no direct allocation to China within portfolios, we do maintain a measured allocation to Asia Pacific equities based on our view that there are some outstanding companies located in the region. A good example is Samsung Electronics, a non-US beneficiary of the artificial intelligence (AI) boom. The company reported solid Q1 earnings in April as profits jumped more than four-fold from a year earlier at the worldʼs largest maker of memory chips, topping analyst estimates. Its semiconductor division returned to profitability as companies like Microsoft and Alphabet led a surge in spending on AI services. The results underscore how demand for the memory chips that power modern electronics and AI is starting to rebound after a severe downturn.

Japanese equities enjoyed a period as the stock market darling over the first quarter of 2024 but wobbled during April. Last month, we wrote that an equity market pull back due to a short-term momentum reversion was not out of the question; admittedly we did not expect to see it happen so soon. The slump was driven by US rate expectations moving to higher for longer, which exacerbated the Japanese yenʼs recent weakness against the US dollar, prompting intervention from Tokyo to stabilise the currency. A weaker yen generally reduces foreign investor interest in Japanese stocks, impacting equity market performance.

Similar to our tactic with Asia Pacific equities, we are focused on individual companies listed on the Japanese market and find that their performance reveals much about broader market sentiment. Over April, Lasertec’s stellar earnings report drove its stock up nearly 15%, while West Japan Railway’s share buyback announcement spurred an 8.6% increase in its shares. We remain cautiously optimistic on the medium- and longer-term outlook for Japanese equities as two key themes continue to play out: corporate governance improvement that is driving better capital efficiency and higher shareholder returns; and the shift from deflation to inflation.

We maintain a measured exposure to broad Asia Pacific and emerging market equities as well as specific exposure to Japanese companies across portfolios. For now, we remain neutral in terms of our positioning to these areas versus peers.

Fixed income - May 2024

It was another challenging month for fixed income investors who eagerly await a change to monetary policy. US government bonds fared worst as interest rate cuts, which were previously expected to come in June/July, have likely been pushed back to later in the year. Over the month, treasury two-year yields topped 5%, climbing to their highest level since November 2023. The US dollar continued to display strength, notching its fourth consecutive monthly advance – the longest winning run since September 2022.

We have pulled back on our exposure to US government bonds in anticipation of a deluge of issuance as fiscal budget deficits remain wide and are unlikely to narrow. This suggests that long-term yields in the US are likely to remain elevated, even if the Fed does embark on its long-awaited cutting cycle. We are also wary of oversupply in the market. We have noted a shift in the composition of US government debt buyers. Foreign central banks used to be the backbone of the market, but their appetite for US debt has dwindled as their pools of foreign-exchange reserves have shrunk or flatlined over the past decade. The Fed has also retreated from the market as it worked to shrink its balance sheet. Overall, the baton has passed from those who need to buy to those who choose to buy, such as mutual funds and hedge funds, who tend to be much more fickle customers.

Although most sub-sectors of the fixed income universe ended April in the red, corporate debt outperformed government bonds, in line with the prevailing trend over the past year. Within corporate credit, lower- rated segments (high yield) of the market fared best given their lower sensitivity to interest rate movements.

While we continue to see value in maintaining a balanced allocation to fixed income across most portfolios, we are now moderately underweight to the asset classes compared to peers, as valuations are expensive and rate cuts may be pushed back to later in 2024. We currently have a preference for corporate bonds over government debt.

Ask us anything - May 2024

Q: What is the Mattioli Woods view on growth, interest rates and inflation?

A: Our central case is that 2024 sees relatively lacklustre global gross domestic product (GDP) growth that will gradually improve during the latter part of the year. We expect that bank lending conditions will remain relatively tight well into 2024 and the impact of monetary policy (i.e. higher rates) will take longer than usual to filter into real economies. Moving into the second half of 2024 and the beginning of 2025, we expect consumer spending across developed markets will be supported by lower headline inflation alongside relatively robust wage growth.

In terms of our outlook on inflation, we do expect further falls at headline level with domestically-driven inflationary pressures easing somewhat through 2024 and gradual interest rate cuts following. As central bankers were reluctant to abandon the ‘transitoryʼ label for inflation on the way up, they may prove reluctant to revive it on the way down, with policymakers keenly aware of the risk that domestically-driven inflation proves sticky.

Although central banks have emphasised that they will be data dependent, this does not mean they will not use forecasts for the economy and inflation as a basis for decision-making. They do, however, seem to want strong evidential backing for a decision to cut rates, which has pushed out market expectations as that evidence will take a bit longer to accumulate. The central case remains ‘higher for longerʼ to tackle the stubborn ‘last mileʼ of inflation but that rates should still be cut in 2024.

If there is a question you would like to pose to our team, please reply to this email or write to [email protected].

The Monthly Market Commentary (MMC) is written and researched by Scott Bradshaw, Lauren Hyslop and Jonathon Marchant for clients and professional connections of Mattioli Woods and is for information purposes only. It is not intended to be an invitation to buy, or to act upon the comments made, and all investment decisions should be taken with advice, given appropriate knowledge of the investorʼs circumstances. The value of investments and the income from them can fall as well as rise and investors may not get back the full amount invested. Past performance is not a guide to the future.

Mattioli Woods is authorised and regulated by the Financial Conduct Authority.

Sources: All other sources quoted if used directly; except fund managers who will be left anonymous; otherwise, this is the work of Mattioli Woods.