United Kingdom - November 2021

Our theme this month is the United Nations (UN). Founded 76 years ago in San Francisco, born out of the ashes of World War II, this intergovernmental organisation is itself the ‘parent’ of UNESCO, the World Health Organisation and more. Its relevance has never been greater, and though the eyes of the world are on Glasgow for COP26, the UN does so much more. Established with the principle to maintain international peace and security, today it oversees great social progress, works tirelessly on human rights issues and is a focal point for many who need a champion. Its 17 Sustainable Development Goals are a call for action by all countries for a global partnership.

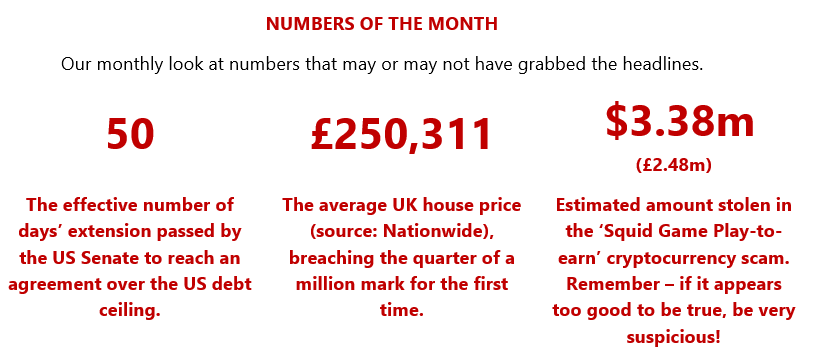

The London Stock Exchange is itself a mini UN, at least from the perspective of where trade is done and/or revenue earned from its many listed entities. Companies listed in London (‘UK equities’) represent more than 100 different countries in this respect, truly global. The largest, currently Unilever, is formed from companies founded in the 1870s, and now includes more than 400 brands, including Axe/Lynx, Dove, Hellmann’s, Knorr, Lipton, Lux, Magnum and Surf. Selling all over the world, personal care, food and refreshment, and home cleaning products are the three main areas of revenue for the business. Utterly global, but a staple of UK equity funds.

Unilever is also often described as a ‘defensive’ stock. The secret of Unilever’s success is that it supplies everyday products (consumer staples) that people use daily throughout the business cycle both in economic booms and recessions. This means that the core business is stable, and the business can grow by improving its brands, moving into adjacent product areas and expanding its product range into new geographies, not least emerging markets. This is not a tip, just an example – think global, buy local can work even in stock markets.

Just before we finished our edit, we heard that the Bank of England Monetary Policy Committee (MPC) decided to leave interest rates at their historical low of 0.10%. The Bank expects inflation to peak around 5% in the first half of next year, and investors had been betting on a rate rise now. Citing furlough’s end and the potential impact on the jobs market, the MPC will surely have a few restless nights ahead of the next decision. The decision did impact large cap stocks, as sterling weakened against the US dollar. Nevertheless, we see UK interest rates as a function of what happens economically from here, rather than a driver of GDP.

Term or word(s) to watch: discontent – probably preceded by ‘winter of’. It is pretty stock wording for newspaper editors to wheel out whenever there may be strife on the horizon as the year comes to an end and is first credited to the editor of The Sun in May 1979, alluding to a quote from Shakespeare’s Richard III.

In 1978/79 the term referenced a tough few months when strikes for higher wages, led by unions opposed to the Labour government’s wage limits, threatened to cripple the country at a time when the weather was the harshest for nearly two decades.

Today, supply side issues, near 300% fuel price inflation (gas) and the latest Covid-19 spike are combining for a Conservative government that, like their Labour counterparts some 40 years earlier, denies there is any crisis.

North America - November 2021

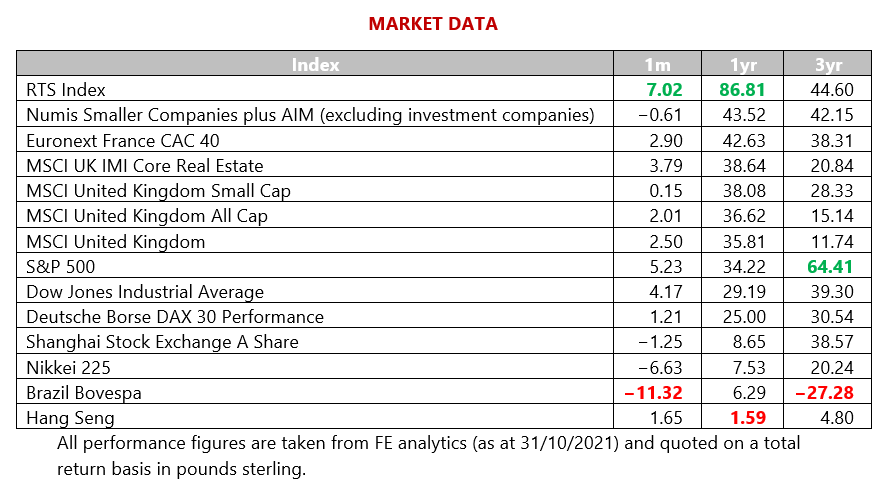

After September had seen the worst month for North American equity markets since the pandemic began, October saw fears recede and improved sentiment on corporate earnings took the Dow Jones and S&P 500 indices to record highs. This is perhaps surprising if we just look at the economic data, where the US Q3 GDP expansion rate fell to 2% annualised compared to the 6.7% reading in Q2. Of course, we need to bear in mind that the figures have seen Q2 2020 ‘fall out’, with that quarter – which saw part of the initial recovery from the pandemic – being replaced by the more sluggish Q3 2021.

The UN is headquartered (the word itself an Americanism) in New York, occupying the same purpose built premises since 1951. From the little known Glass Wall (1953) to blockbusters such as The Avengers franchise, the UN building has entered popular culture, perhaps a sign that the organisation now has a place in all our lives.

Consumer spending, traditionally a large part of US GDP, has been reined in recently, which is partially a result of global supply chain issues. This can be seen in the port of Los Angeles, which handles 40% of all inbound shipping to the US and is a key part of supply chains from Asia. Shortages of shipping containers as well as workers for the docks and within the supply chain have led to the average length of time a container is idling at the dock rising from four days (pre-pandemic) to at least nine days. Warnings have been made that some goods including toys may be in short supply for Christmas.

Elsewhere in the US, the Federal Reserve was widely expected this month to announce the beginning of the tapering of its $120 billion a month purchases supporting the bond and mortgage markets … and has now done so. This had been signalled by Chairman Powell last month with his announcements much trawled over for indications of the future path of interest rates.

It is the current consensus that two rate hikes are expected before the end of 2022, with some elements of inflation being seen as more long lasting rather than transitory as previously assumed.

Finally in terms of the politics, October also saw the US Congress pass a stopgap measure to push the need to increase the US debt ceiling back to 3 December, with this being passed on partisan lines. We can expect a repeat of the deadline brinkmanship then. The Democrats also continue to struggle to get through a new stimulus package targeting infrastructure, social care and climate change. Compromises so far have seen the value of this come down from $3.5 trillion to $1.75 trillion, with priorities like family leave and free community college stripped away.

The US equity market, at an index level, continues to look expensive relative to other markets, with Technology stocks in particular richly priced. We still selectively like other areas of the US market and have been increasing our exposure to value names. We also continue to have indirect exposure through our thematic equity holdings.

Europe - November 2021

European equity markets enjoyed strong gains over October, recouping all of September’s losses as robust third quarter earnings reports drew in investors. Data released over the month showed the French and Italian economies growing faster than expected in the third quarter, while supply shortages constrained German output. Despite these positive indicators it is unlikely to be smooth sailing as we move into 2022.

We see investor sentiment continuing to teeter between optimism over strong earnings and growth prospects with apprehension around the risks of higher inflation, interest rates and energy prices.

The Vatican City is one of two permanent non-member observer states in the General Assembly of the United Nations. In fact, it has never applied for full membership to the UN. The other is Palestine.

Interestingly, the International Monetary Fund (IMF) does not believe Europe will be dragged into an inflation spiral, despite prices rising at the fastest rate in 13 years just last month. In mid-October, IMF European Department Director Alfred Kammer told a news briefing that the surge in energy costs should fade in 2022, saying that, ‘We don’t at this stage expect any inflation spiral in Europe … The high inflation which we are seeing right now is really driven by … an increase in energy prices and we expect that to fade out during 2022.’ Kammer added that labour market slack means inflation is unlikely to push up wages.

Just a week later, data was released showing that inflation in the eurozone has soared past expectations to reach a 13-year high. The European Union’s statistical arm issued a preliminary estimate, pegging the headline eurozone inflation rate at 4.1% in October, which is a considerable leap from 3.4% in September and well ahead of forecasts of 3.7% (Eurostat data).

Inflation in the eurozone is now at its highest level since July 2008, after being driven higher by soaring energy costs, tax increases and growing price pressures as a result of the supply chain crisis. This creates an even bigger headache for the European Central Bank (ECB), which kept rates on hold following the October meeting insisting higher inflation was ‘transitory’ and pushed back against market bets that it would need to hike rates as soon as early next year.

The ECB also indicated that it would continue buying assets under the Pandemic Emergency Purchase Programme (PEPP), albeit at the somewhat moderated rate announced in September. ECB President Lagarde did acknowledge that inflation may take longer to decline than initially expected but reiterated the view that the rate of consumer price increases should slow to less than 2% by 2023. Lagarde also said that she expected the ECB’s PEPP activities to end in March 2022, although she indicated that the central bank would likely decide in December whether to expand a different asset purchase programme to ease the transition.

Despite the potential for increased volatility as investors nervously try to predict central bank actions, we remain more positive on European equities than for some time. We believe the ECB has put policies in place to nurture the bloc’s recovery, which looks to have further to go than developed peers such as the US.

Japan - November 2021

The Japanese equity market has made a strong start to the month with a welcome election victory for new PM Fumio Kishida’s Liberal Party. There was a greater than expected margin of victory for his party, which retains control of the country’s lower house. Clearly a poor result could have had a destabilising effect and this additional stability is important given the number of recent political changes.

Interestingly, the greatest beneficiary from this election appears to be the relatively right-wing Japan Innovation Party, which has focused on regulatory reform, though in reality the number of seats it holds is still small. The opposition is very fragmented in Japan, which is one of the reasons that the Liberal Party has been dominant for so long.

With this election out of the way, investors will be looking at Kishida’s policies in greater detail. It has been a shaky start given contradictory statements in various policy areas, but a priority seems to be some sort of move away from the Abenomics era and a focus on spreading the benefits of Japan’s recovery. The economic security of the country is also high up the agenda and the urgency of defence measures seems to have increased given the challenges posed by China.

Japan became the 80th member of the UN in 1956. This was an important step for the country, which had adopted a pacifist stance after World War II, with the organisation seen by many as offering further support for the country’s neutrality.

Plenty of uncertainty then, but for now the market focus is on the security that this election result brings. Japan still looks like one of the more interesting equity markets out there and allocations reflect this.

Asia Pacific - November 2021

Asian markets enjoyed a rebound last month following a challenging September, albeit a moderate one in comparison to developed markets. From an economic growth perspective, the recovery in many Asian economies remains solid. Rising vaccination rates are enabling economies to gradually reopen, with mobility picking up accordingly and economic surveys are moving higher as a result. Indeed, flash purchasing managers’ indices (PMIs) have improved in the majority of countries, though China is one glaring exception.

Broad Asian indices have been restrained by weakness in Chinese markets as investors digest concerns over energy blackouts, weaker manufacturing activity and the impact of the beleaguered property sector.

Next time you are struggling to stay awake during a meeting spare a thought for those present on 23 January 1957 when the longest speech in its history was made to the UN. For five hours, Indian representative V.K. Krishna Menon defended India’s position on Kashmir, and not content after five hours, he continued for three more hours during the next day’s session.

While investor worries around the Chinese property sector eased slightly after a large property developer made interest payments that had previously been missed in September, it’s an issue that remains at the forefront of investors’ minds. Evergrande Group’s struggles may have dominated the news flow, but the risk to the global property market stems from some of its rivals that have spent the last decade competing to build ever taller and grander skyscrapers.

Modern Land has become the latest Chinese developer to miss a payment on a dollar bond, signalling continuing turmoil in the sector. Investors’ attention is focused on how Chinese authorities will manage regulations in the real estate sector to control spill over risks. This of course adds a high dose of uncertainty to the mix as the Chinese government is not known for its predictability or shareholder friendliness. Valuations suggest that greater regulatory uncertainty may now be better priced in across the market.

We continue to favour investing in broad Asia Pacific funds with the ability to cherry-pick the regions and companies with the best outlook. In some places, we maintain a modest exposure to Chinese equities though investing here remains an almost constant source of debate among the team.

Emerging Markets - November 2021

Our emerging markets exposure tends to favour emerging Asian nations, including our country specific allocations to India and China, rather than either Emerging Europe (& Russia), Africa or Latin America. We regularly review this position and, at present, Latin America in particular looks very unfavourable.

There are 193 members of the UN, but how many of them have the word United in the country’s official name? Answer later in this section …

Brazil has been in the headlines following the recommendation from a Senate committee to prosecute far-right leader Jair Bolsonaro on charges including crimes against humanity, for his mishandling of the pandemic. With a polling score in the low 20s, the leader faces an uphill challenge to stay in power in next year’s elections, with the economy an equally, if not more, significant factor.

October saw the announcement of a $70 monthly payment to voters, which spurred a market sell off as concerns focused on how the country could afford this. Inflation is also high and had crossed 10%, with the central bank having put up interest rates by 5.75% since March 2021.

Further North, Mexico is also having a difficult time, with the Q3 GDP announcement showing a contraction of 0.2%. Supply chain disruptions have hit Mexico particularly hard, especially in the automotive industry where the global shortage of chips has slowed production, although there are signs of improvement in other sectors. Political risk, while nowhere near as elevated as in Brazil, is also a factor.

President Andrés Manuel López Obrador has demonstrated he is willing to be interventionist, and along with new rules that make subcontracting more difficult, has announced plans to increase state control of the energy industry. This includes nationalising future lithium exploration (the metal vital for batteries) and removing independent regulators.

There are five nations with united in their official name. These include the obvious United Kingdom, United States of America and United Arab Emirates and the less obvious full names of the United Mexican States (most commonly known as just Mexico) and the United Republic of Tanzania.

Where we hold broad emerging allocations, we prefer to buy managers focused on companies first, rather than trying to pick the fastest growing economies. We regularly review not just where we are invested but other areas and, for now, Latin America does not appeal to us.

Spotlight on: Private Equity - November 2021

Private equity continues to feature in our portfolios and the investment case for it looks solid. Yes, some have expressed concerns about a rising interest rate environment impacting leveraged deals, but the broader characteristics of private equity appear to make it look especially attractive at the current time. Public equity markets are shrinking in many parts of the globe and many of the best opportunities for investors can now only be accessed away from the public markets arena.

Private equity companies generally take stakes in businesses and via engagement and (often) financial engineering, transforming them ahead of an exit strategy. This can mean a focus on long-term value creation away from the short-term nature of the public markets. We have of course seen a flurry of private equity money in the UK public markets of late, and the influence is growing. Investment trusts are often the most sensible vehicles to employ this type of investing, given the fixed pool of capital that can be invested long term without the distractions of inflows and outflows, again sharpening that long-term perspective.

Given the lack of visibility on positions and the periodic nature of valuations of the underlying business, they typically trade at significant discounts to reported net asset values (NAVs). So, a proven vehicle like Harbourvest, which we use in many portfolios, trades at around a 25% discount to NAV. These sorts of substantial discounts have persisted for decades (given the issue of valuation transparency), and the discount obviously moves around over time, but for the long-term investor it seems like an attractive proposition to be able to acquire assets at such prices.

A more challenging environment could materialise in coming years – in addition to higher rates, the favourable tax treatment of debt relative to equity may be removed at some point. For now, in a world of elevated asset prices and high valuations in public markets, the niche opportunities in private markets look appealing and private equity exposure is an established part of many of our portfolios.

Fixed Income - November 2021

Investors are continuing to bet that central banks have misinterpreted the nature of the inflationary threat as we recover from the worst of Covid-19 (fingers crossed). Short-dated government bonds have come under particular pressure as inflation is seen persisting over the short term, whereas longer-dated bonds have been less dramatically affected.

This flattening of the yield curve, in bond market parlance, suggests that monetary policy is seen as ultimately containing inflation over the long run, but that challenges over the next few years are very real. These recent movements do rather expose the idea that adjusting the duration exposure by focusing more on short-dated bonds is sufficient to protect against current developments as they have been in the epicentre of the sell-off. Some hedge funds have run into serious difficulties given the speed of the moves and more firms are likely to be revealed to have been caught out.

There is the suggestion that central banks are starting to change their tune slightly having previously embraced the transitory thesis. In Australia, the Reserve Bank has allowed yields on its three-year bonds to move well above its target, and the Bank of Canada has stopped its quantitative easing programme, which has led to a sell-off there. It is very much a process of taking baby steps here, tweaking support programmes before moving to very small rate rises, but it appears that the direction of travel is looking clearer.

We have seen enough to convince us that reducing fixed income exposure is the right thing to do and have taken some more of our sovereign debt and investment grade holdings out of portfolios. We continue to monitor fixed income markets and will make further changes as we see fit.

Commodities - November 2021

After a difficult run that has led to some questioning its role in portfolios, gold enjoyed a decent October. Indeed, along with clean energy funds, those focused on gold were among the top performers over the month. Inflation concerns have moved to the front of investors’ minds so this is not surprising, though we have previously warned how gold can be unpredictable against this sort of backdrop as concerns over the corresponding interest rate increase risk can be a headwind.

Clearly gold equities are geared to plays on the fortunes of gold and many of the funds in the sector produced very impressive double-digit returns, versus a much more modest rise in the underlying gold price. However, gold was significantly behind other commodities with oil again powering ahead, and silver, that close relation of gold, also a strong performer.

As the argument that inflation is transitory starts to look flimsier, we might expect the broader commodity complex to attract more attention as it is proven as an inflation hedge. It is fair to say that the area is underrepresented in many client portfolios, though the academic case for their inclusion from a portfolio construction perspective is worth considering.

Some of this underweight is due to the difficulties associated with mirroring commodity prices through ETF vehicles (the returns are affected by the ‘rolling of contracts’ to maintain positions).

For now, our commodities exposure is overwhelmingly focused on gold. As with other asset classes, the developing inflation story will have a bearing on the attractiveness of the wider space, and we have suitable investment options should we decide to introduce new holdings.

Property - November 2021

UK commercial property is continuing to rebound, with capital values now having recorded nine months of uninterrupted increases. It is pleasing to see this broadly spread with retail, industrials and other sectors all showing progress. The recent Budget announcement regarding a temporary 50% cut in business rates for shops, restaurants, bars and gyms is likely to further help the cause of recovery post Covid-19 and was warmly welcomed.

The UN headquarters (the Secretariat) building is situated in Manhattan. It stands at over 500 feet tall and was completed in 1951. Technically the building and the land on which it stands is extraterritorial (and therefore under the sole administration of the UN) due to a treaty agreement with the US government.

Whether this is sufficient to rescue the struggling high street is of course debatable and we are focused on other areas in portfolios. It still seems like a gamble to have excessive exposure to more sensitive areas of the UK economy, especially in structurally challenged areas, and the relative robustness of cash flows elsewhere makes other sectors much more attractive.

We have a broad opportunity set at our disposal and can shift exposure across all the aforementioned sectors but also invest in niche plays whether it be student accommodation, warehouses, specialist housing ventures or healthcare facilities.

Of course, it can be argued that some of the general drivers that make property interesting exist outside of the UK too and we have indeed been spending some time looking at global property securities. This introduces some additional, niche ideas whether it be German residential or Japanese logistics! This is another illustration of our constant search for ways to add value to portfolios.

Property allocations have been stable in portfolios for several months and maintaining allocations at current levels looks sensible given the attractions relative to other asset classes.

Responsible Assets - November 2021

Glasgow currently plays host to COP26, the UN’s 26th annual climate change conference (COP – Conference of the Parties). COP26 holds particular significance in that it occurs five years since the Paris Agreement was struck, in which almost every nation around the world agreed to work together to limit global warming to below 2 degrees Celsius, with the ultimate aim of 1.5 degrees. The plan is that every five years nations would come back with updated/more ambitious plans.

The lead-up to the conference was somewhat chaotic, for several reasons. The event is missing several big names: Presidents Xi Jingping, Putin and Bolsonaro of China, Russia and Brazil, respectively, were not among the c. 120 world leaders in Glasgow. This is concerning considering that they represent countries that are among the top 10 worst polluters, accounting for over 30% of the world’s CO2 emissions (Source: Financial Times). Covid-19 has, on this occasion, been a helpful excuse for some …

Many are bracing themselves for disappointment over the fortnight or so of scheduled meetings; we have seen plenty of previous grand ideas fall short. In 2009 developed countries pledged $100bn a year by 2020 to help poorer nations deal with climate change. It was recently announced that numbers have fallen way short and optimistic estimates suggest the pledges may only be achieved by 2023. Worse, many scientists believe we have left it too late to achieve a 1.5-degree target, with planetary changes leading to naturally higher emissions, causing an existential climate crisis.

It is fair to say that behind every headline there are many finer details to be ironed out; likewise, there are plenty of deals still to be done by the key representatives of nations including China, Russia and Brazil. There does seem to be some momentum behind the desire to act – the issue remains, what to do and, importantly, at what financial cost.

While the scientists may be right and it may be too late to hit the Paris targets, the point remains that something has to be done. We look forward to providing a summary of events at COP26 in next month’s edition, and if you can, do sign up for our November webinar, which will also be looking at climate change, among other things.

Currency - November 2021

Investors had driven sterling up against the US dollar ahead of the latest Bank of England decision on interest rates here, seeing a fall of 1% immediately upon the announcement that rates would not change this month. A 1% fall is hardly news, but it does clearly show the sensitivity to what, at best, might have been a move from 0.1% to 0.25%. The volatility of currency movements has long led us to sit on the side, only occasionally straying on to the pitch when hedging into a particular currency seems prudent alongside the main investment reasons for being involved.

UK Interest Rates - November 2021

While the world looks to Glasgow for leadership on climate change and so much more, those with UK deposits/mortgages (and more widely, investors) have been watching the Monetary Policy Committee of the Bank of England … fearful, perhaps, that the climate might be changing for interest rates.

As you have already read in our lead piece, the decision this month is ‘no change’, though with some pretty clear warnings that it was close (as close as a vote of 7–2 can be), and that we must expect rate rises sooner than later. When pressed, the Governor, Andrew Bailey, said the rate rise would come ‘From now onwards’. Hardly forward guidance …

The Monthly Market Commentary (MMC) is written and researched by Simon Gibson, Richard Smith, Scott Bradshaw, Jonathon Marchant and Lauren Wilson for clients and professional connections of Mattioli Woods, and is for information purposes only. It is not intended to be an invitation to buy, or to act upon the comments made, and all investment decisions should be taken with advice, given appropriate knowledge of the investor’s circumstances. The value of investments and the income from them can fall as well as rise and investors may not get back the full amount invested. Past performance is not a guide to the future. Mattioli Woods is authorised and regulated by the Financial Conduct Authority.

The MMC will always be sent to you by the seventh working day of each month, usually sooner, is normally delivered via email, and is free of charge as the MMC is generally made available to clients who have assets under our management in excess of £200,000, and to all clients under our Discretionary Portfolio Management Service (DPM). Normally, the MMC costs £397 + VAT per annum. Professional advisers and their clients should contact us if they are interested in receiving a monthly copy.

Sources:

www.bbc.co.uk,

www.bloomberg.com,

Financial Express,

www.thedragonsblade.com,

www.express.co.uk,

www.pitstoppin.co.uk,

www.sibcyclinenews.com,

www.vr-12.com,

www.smalltalkbigresults.wordpress.com,

www.anonw.wordpress.com

www.avantida.com,

www.plazmedia.com,

www.viewzone.com,

www.mmn.com.

All other sources quoted if used directly; except fund managers who will be left anonymous; otherwise, this is the work of Mattioli Woods.