Global markets summary

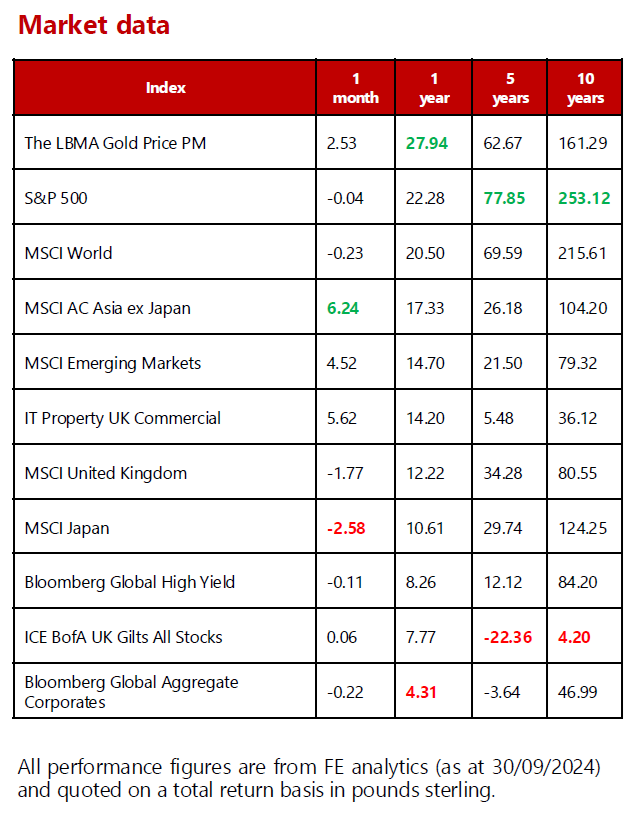

The winds of change blew through global equity markets over September, ushering in monthly moves dramatic enough to shift year-to-date market leadership. China’s stock market surged by almost a quarter (in £ terms) over the month after authorities committed to further monetary and fiscal support. The stimulus measures helped to soothe investor concerns and supported a broad rally across Asia (ex-Japan) equities. As a result, the MSCI Asia (ex-Japan) index has vaulted over the former year-to-date leader, delivering 15.12%, while the US S&P 500 has been relegated to second place, delivering 14.82%. While this is a startling move and the short-term positive sentiment could have further to run, we remain circumspect on Asia Pacific equities, believing that, although these fiscal measures may be enough to sustain the next few quarters of economic growth, the medium to long-term picture remains unclear.

September was a more muted month for developed markets, with the US S&P 500 delivering 2.10% in local currency terms but just 0.04% in £ terms as sterling strengthened against the US dollar. European and UK equities fell in September, with the Euro STOXX Index returning -0.20% (to £-based investors) and the MSCI United Kingdom down -1.77%. The softer month for domestic stocks reflected several disappointing economic data releases.

Fixed income markets were buoyed by the prospect of major central banks continuing to ease their respective policy rates. Developed market government bonds and credit both delivered solid returns while emerging market debt rallied.

The volatile situation in the Middle East has put markets on edge over the course of the past few weeks; however, the relatively contained move up in oil prices in the past several days demonstrates the fact that the conflict, which is regionally contained (though devastating from a humanitarian viewpoint), may have limited impact on the trajectory of the global economy.

2024 has so far been a strong year for multi-asset investors with the majority of asset classes delivering positive year-to-date returns. As we move into the final quarter of the year, our central case is that risk assets can continue to perform well, with central banks bolstering economic and financial conditions through monetary policy easing. More attractive valuations outside of US markets warrant more varied global equity exposure than our previously preferred overweight stance to US equities, as the prospect for a broadening of the rally improves. We are, however, cognisant that more accommodative policy also signals increased risk of an economic growth shock, and as such we have taken a balanced approach to equity risk.

United Kingdom

Having enjoyed a strong run, UK equities fell in September, with the MSCI United Kingdom -1.77%. The softer month for domestic stocks reflected several disappointing economic data releases. Towards the start of the month, GDP came in flat, below the +0.2% that analysts had expected. This was followed by a weak consumer confidence number, which appeared to show that the upcoming budget is weighing on the propensity of consumers to go out and spend.

It’s not just consumers who are cautiously awaiting clarity around the budget; there are a range of potential implications for investors. Indeed, the party’s decision to major on economic difficulties may have backfired, given the weakening level of consumer confidence. More concerningly for the party, the public support for Kier Starmer has collapsed, after a string of controversies around gifts. Indeed, data from The Observer suggests that his approval rating is now lower than Rishi Sunak’s and just 24% of people approve of the job he is doing.

Labour’s cautious rhetoric around the economy and the need for higher taxes, combined with the Bank of England’s decision to hold interest rates in September, also helped the domestic currency to strengthen. Indeed, sterling is one of the best performing developed market currencies over the past year and has recovered almost all the ground lost following the Brexit referendum.

A strong pound supports our view that domestically-focused equities are well placed to outperform, which is reflected in our overweight to mid- and small-cap companies in our UK Dynamic Fund. Towards the end of the month, the fund completed its first full year and pleasingly delivered performance of +15.73%, ahead of the benchmark’s +12.38%. The fund continues to find a number of exciting opportunities and we continue to believe that valuations in the UK remain compelling.

North America

In terms of US equities, September has an overall poor track record, with the S&P 500 averaging -1.16% per month (in local currency terms) since 1926. Suffice to say, expectations for the month were low. However, investors found themselves pleasantly surprised as, though it began with the worst week since March 2023, markets recovered towards the end of the month as the Federal Reserve (Fed) delivered a larger- than-anticipated 0.50% rate cut.

While the S&P 500 ended the month in positive terms for $-based investors, it is important to note that returns were lesser for £-based investors due to the weakening of the US dollar against sterling following the Fed’s first rate reduction since March 2020.

We do not anticipate that the results of the Presidential election will move markets at headline levels but expect that a Trump administration would be more immediately positive for smaller companies while industrials and defence stocks would likely be supported by a Harris victory. Overall, this view supports a broad exposure to US markets that is well diversified in terms of sector, style and market cap.

Although news flow is dominated by politics as we approach the Presidential election, the trajectory of monetary policy continues to hold greater sway over investment markets. It may surprise you to learn that the best performing sector of the US equity market year to date is utilities rather than technology. The prospect of lower interest rates has attracted investors back to high- yield dividend equities like utilities, while the rise of artificial intelligence is expected to contribute to a substantial increase in power usage over the next decade, which could meaningfully drive electricity producers’ businesses.

The US market continues to look expensive, but we maintain a neutral stance, believing that the environment is broadly supportive of risk assets. The Fed dot plot (which shows expectations of where rates will be in the future) suggests that two 25 basis point interest cuts are expected over the next two meetings before year end. These cuts should further bolster equity markets, particularly interest rate sensitive areas. In addition, Q2 2024 earnings officially set a record (while sales fell 0.3% short of one), with more earnings records expected for Q3 and Q4.

Within our core portfolios, we maintain a neutral stance to US equities via a blend of actively managed funds and passive strategies that provide us with a cost-effective, well-balanced exposure to the region.

Europe

European equities have had to face their fair share of uncertainty this year, from anaemic economic growth in Germany, to a snap election in France. It appears, however, that equity markets have taken this in their stride, with the Euro STOXX returning 7.66% year to date (in £ terms). Despite domestic issues, European equities have benefited from cuts to interest rates and falling inflation globally. That said, over September, European equity returns were more muted, as the bloc’s worsening growth outlook came to the fore.

Economic data released over the month reinforced the sluggish nature of the region’s recovery so far this year with the composite PMI reading for September coming in at 49.6 (PMI readings less than 50 indicate a contraction in activity). At present, it looks like much of the risk is concentrated in one country: Germany. The German economy’s reliance on manufacturing has been a particular drag on the overall bloc amid both weak demand from China and increased competition from cheaper Chinese exports. In addition, the lack of clear direction of leadership coming from the German government impedes the possibility of a credible attempt to tackle the region’s economic malaise.

PMIs pointing to weaker eurozone growth, inflation falling below the 2% central bank target and a more dovish tone from the European Central Bank (ECB) have combined to strengthen expectations of an interest rate cut in October. Comments from ECB officials indicated that their gradualist approach to easing monetary policy may be shifting, with President Christine Lagarde hinting that borrowing costs might soon be lowered. This should be broadly beneficial for the bloc’s equity market, but time will tell if it will be enough to offset the weakening growth. The current balancing act is a difficult one, with growth disappointing and service inflation frustratingly sticky.

We maintain a neutral stance towards European equities. We believe that the region should benefit from the recent turn in the interest rate cycle, while attractive valuations as well as high- dividend yields and share buybacks lend further support. However, we cannot ignore the fact that geopolitical uncertainty remains relatively high and additional challenges such as trade disputes and a slowing China persist.

Rest of the world

Following a barrage of disappointing economic and monetary indicators for August, China’s President Xi issued an urgent request to the authorities to take action in order to achieve the 5% real GDP growth target for this year. This was shortly followed by significant coordinated stimulus measures, which include fiscal, monetary, and property-related support. Investors appeared reassured by the stimulus measures and, after a false start in April/May, China’s ‘H’ shares finally recovered 20% from the September low. Domestic ‘A’-shares also appear to have participated in the turnaround, supported by high trading volumes. Gains across Chinese equity markets supported the broad Asia Pacific region leading to strong monthly returns from the MSCI Asia (ex Japan) Index.

The Japanese Topix ended the month -1.93% in £ terms as markets reacted badly to the results of the Liberal Democratic Party (LDP) leadership election. Investors favoured Ms Sanae Takaichi, who is viewed as an expansionist, and as such were disappointed when Shigeru Ishiba emerged as victor. The negative sentiment was compounded when the incoming prime minister said he aimed to call snap elections for 27 October and hinted that tax hikes are on the cards.

Politics aside, looking at Japan’s economic fundamentals, corporate earnings and macroeconomic figures have shown solid progress over Q3. Aggregate quarterly earnings from April to June exceeded expectations. The weakening yen supported this performance, while domestically- focused sectors also demonstrated robust recovery. Real wage growth, taking inflation into account, turned positive for the first time in 27 months in August and its positive momentum continued in September.

Within our core portfolios, we captured the strong performance of the Asia Pacific (ex-Japan) market via our investment in a high conviction, actively managed fund, which we blend with a cost-effective index tracker. We do, however, remain neutral on the space despite the impressive rally and as such, took profit over the period. Our view is that the fiscal measures should be enough to hit the 5% growth target over the next few quarters but fall short of supporting the domestic economy over the longer term.

Fixed income

September was a busy month for global central banks as the US Federal Reserve (Fed) reduced its target rate range by a larger- than-anticipated 0.5% to 4.75-5.00%, while the European Central Bank (ECB) and Swiss National Bank both reduced their respective policy rates by 0.25% pts, to 3.50% and 1.00%. The Bank of England remained on hold, after lowering the base rate in August to 5.00%.

The Fed’s move also paved the way for policy easing in many emerging market economies as rate cuts were delivered in countries on fixed exchange rate arrangements. However, central banks targeting inflation were also quick to move, with further policy easing to come, particularly in Asia. These moves supported developed and emerging market government bond yields, which rebounded from recent lows over the month.

We retain an overall neutral stance to fixed income assets, seeing limited near-term upside with yields having broadly reached our year-end targets. In terms of US government bonds, relative to our soft- landing base case, valuations look rich, and we expect the asset class to underperform after the recent rally. We also prefer to stay neutral to UK gilts, as although inflation is falling and the Bank of England cut interest rates in August, wage inflation remains persistently above BoE target, potentially constraining the Bank’s ability to cut rates much further in the near term. We also remain cautious on the outlook for credit spreads. This is a valuation-based view as there is limited room for further spread compression. Any further positive risk-asset moves should benefit equities considerably more than credit.

Importantly, over the quarter, we saw evidence of a shift in the outlook for stock/bond correlations, allowing investors to enjoy the diversification benefits of holding bonds within a portfolio. Amid the equity sell-off we endured at the start of August, the 10-year US Treasury yield fell, and the corresponding bond prices rose, benefiting from a flight to safety and from expectations of future interest rate cuts. We view this as a positive development, providing us with another tool in our arsenal as we look to build resilient portfolios.

Although we expect a more accommodative interest rate environment in the second half of 2024, the US presidential election remains a focal point for markets and could lead to increased volatility. As such, within our fixed income portfolio, we have maintained a globally-diversified approach, prioritising credit quality and managing duration to protect against interest rate risk.

Ask us anything

Q: Have you made any changes to portfolios following escalations of tension in the Middle East? What are your views on how the situation could affect markets?

A: The situation in the Middle East is incredibly fluid at present with the region in the throes of its most dangerous crisis in decades. Hostilities unleashed after Hamas’s 7 October 2023 attack on Israel have sharply escalated over the past two months, propelling Israel, Hezbollah, Hamas and Iran deeper into a war. The main battlefields have been Gaza, Lebanon, and Israel, but the entire region is on the brink of conflict with escalation into Iran in recent days.

While the human toll cannot be forgotten, market reaction has been muted to say the least, with the MSCI World and S&P 500 indices up 0.81% and 1.10% in local currency terms over the past month. Indeed, the latter is sitting close to an all-time high having risen 34.51% over the past year to close yesterday, in $US terms.

Bond markets too have enjoyed a strong month, and while these are sometimes seen as a safe haven in times of heightened geopolitical strife, this is more likely down to the fact that the US Federal Reserve (Fed) cut interest rates by 0.5% on 18 September and inflation continues to trend lower, rather than anything more sinister. Expectations are for further rate cuts in both the UK and the US over the coming months, which should continue to benefit fixed interest assets.

Until Tuesday 1 October, oil prices (Brent crude) had remained at historically low levels, having fallen from $91 per barrel in April of this year to below $72 per barrel end September. Indeed, the events between Israel and Iran this week have seen the price rise to nearer $75. While we acknowledge the impact of a rising oil price on inflation, it is not an area in which we directly invest, other than through the broader funds held within the multi-asset strategies.

In terms of asset classes, the big winner has been physical gold, which is certainly seen as a safe haven asset and indeed, the recent uncertainty has supported the precious metal’s price. Performance of physical gold has been exceptional over the past year, and we have exposure within our multi-asset funds (albeit at low levels, as part of our alternatives allocation), which has been enhancing returns.

Politics rarely impact financial markets drastically and while we have a strong eye on what is currently happening in the Middle East, as well as the inflationary effects of a higher oil price and an awareness of the impact that the closure of the Suez Canal might have on world trade, we are maintaining portfolios in a sensibly diversified manner. We hold assets that can continue to perform well if the situation worsens, and we have the ability to raise cash, likely at the expense of equities. However, now, we are happy to maintain our current approach, with our central case of modest global growth, lower inflation and lower rates driving our asset allocation views.

KEY TAKEAWAYS

- Despite a serious escalation of the conflict in the Middle East, international equity indices are hitting new highs.

- While we remain invested in a diverse portfolio of assets in line with our macroeconomic central case, we have added elements of resilience, acknowledging that there will likely be more volatility ahead.

- We have the flexibility to raise cash quickly should our views change.

If there is a question you would like to pose to our team, please reply to this email or write to [email protected].

The Monthly Market Commentary (MMC) is written and researched by Scott Bradshaw, Lauren Hyslop and Jonathon Marchant for clients and professional connections of Mattioli Woods and is for information purposes only. It is not intended to be an invitation to buy, or to act upon the comments made, and all investment decisions should be taken with advice, given appropriate knowledge of the investor’s circumstances. The value of investments and the income from them can fall as well as rise and investors may not get back the full amount invested. Past performance is not a guide to the future.Mattioli Woods is authorised and regulated by the Financial Conduct Authority.Sources: All other sources quoted if used directly, except fund managers who will be left anonymous; otherwise, this is the work of Mattioli Woods.