Junior Self-Invested Personal Pensions (Junior SIPPs) harness compound growth over 50-65 years, transforming modest contributions into substantial retirement wealth. This article shows how early investment, combined with time and tax advantages, can realistically build seven-figure retirement funds for your children.

The mechanics: tax relief and compound growth

Parents and grandparents can contribute up to £3,600 gross annually to each child’s pension. With automatic 20% government tax relief, you only pay £2,880 net – an immediate 25% boost before any investment growth.

Moreover, the £3,000 annual gift allowance means that parents and grandparents can gift every tax year (6 April to 5 April) to fund £2,880 into a child’s pension, and it will no longer be part of the parents/grandparents estate for Inheritance Tax purposes.

The money stays inaccessible until age 55 (rising to 57 in 2028), creating enforced discipline that most investors struggle to maintain. Parents control the investments until the child turns 18, then responsibility transfers to the young adult. This structure transforms childhood savings into an intergenerational gift – prioritising long-term security over short-term access.

Case study: A ten-year commitment

In 2018, Simon and Linda began contributing £3,600 gross a year (£2,880 net) over seven years for each of their sons, Ryan (6) and Alex (8), (a total each of £25,200 gross or £20,160 net). At an average 4.7% annual growth, this reached nearly £29,888 per child by 2025 – compound growth added approximately £4,688 despite the short timeframe.

They plan to continue for three more years until 2028, with an additional £10,800 gross for each child. Using a conservative 4% growth assumption, the ten-year total projects to approximately £45,184 per child.

Here’s where time becomes transformative: if Ryan and Alex never contribute another penny, their pensions could grow to between £241,711 and £261,862 each by retirement age, based on 4% average annual growth over 42-44 years. A decade of contributions during childhood creates a significant pension pot by retirement age.

Important: Projections are illustrative only. Investment values can fall as well as rise. Tax rules and pension regulations may change. This article does not constitute as financial advice and you should always seek professional financial and tax advice before making investment decisions. You can watch the full video here: https://youtu.be/nHP-FQXNnlA

How it compares contributing to a Junior SIPP from birth or at 18 years old

There is no guarantee of future investment returns, however, let’s assume a 5% annualised real return for our long term projections, regardless of possible periods of higher or lower inflation.

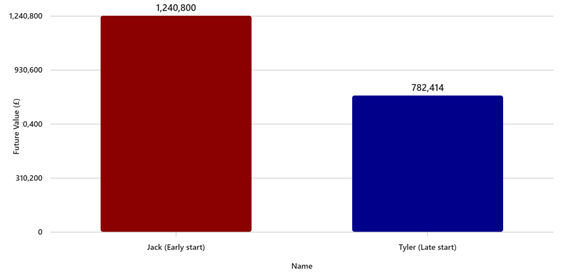

Now let’s imagine that Darren and his wife Victoria started contributing £3,600 gross annually for their twins Jack and Tyler at different stages in life.

If they contribute for Jack until age 18 (early start), then leave it untouched for the next 50 years, assuming 5% annualised growth over the period, it could grow to a future value of approximately £1,240,800.

On the other hand, if Darren and Victoria do not start contributing £3,600 gross annually for Tyler for the first 18 years (late start) but continue to contribute for the next 50 years then, assuming the same 5% annualised growth, it could potentially grow to a future value of around £782,414.

Figure 1 – Illustration of comparison on pension growth, early start versus late start in future value

Both could potentially grow to over £1 million in today’s purchasing power. From the 6 April 2027, the beneficiaries of these sizable pensions are likely to be affected by Inheritance Tax on unused pension funds and death benefits*. Despite contributing £115,200 less overall, Jack ends up with more than £458,385 in his pension pot than Tyler.

This highlights the benefit for parents of concentrating your financial commitment into a defined period rather than requiring perpetual payments. By the time your child is 18 their retirement foundation is secure.

Important: Your benefits are dependent upon a number of factors; the amount you invest, the age at which you commence benefits and external influences such as investment returns, inflation, interest rates, annuity rates and charges. The figures illustrated are only examples and aren’t guaranteed – they aren’t minimum or maximum amounts.

Why Junior SIPPs work

- Tax efficiency at every stage: Contributions receive immediate 20% relief, growth is tax-free within the pension, and 25% can typically be withdrawn tax-free at retirement under current legislation.

- Complementary capacity: Junior SIPPs work independently from Junior Individual Savings Accounts (JISAs) (currently £9,000 annual savings limit), letting you maximise both where possible.

- Structured engagement: At Mattioli Woods, we pair Junior SIPPs with discretionary fund management, creating tailored strategies and establishing an advisory relationship that evolves as your child matures. This continuity proves invaluable when children take control at 18, supporting their transition to financial independence.

Beyond the numbers: building financial capability

Childhood pension planning teaches more than compound growth. Involving children as they mature develops financial literacy and disciplined investment thinking. The enforced patience of pension structures – combined with professional guidance – instils principles that serve them throughout their lives: understanding long-term value, managing costs, and resisting short-term temptation.

Broader wealth planning

For grandparents considering Inheritance Tax (IHT) planning, the annual £3,600 contribution provides a structured wealth transfer method that simultaneously reduces estate values and secures grandchildren’s futures. Junior SIPPs integrate effectively with bare trusts, Junior ISAs, and for substantial estates, family investment companies or discretionary trusts. Each serves distinct purposes around control, accessibility, and tax treatment.

Lastly, parents and grandparents should consider initial and ongoing fees, investments options, any minimum investment amount and the ease of use of the platform where the investments are held.

Important: Projections in this article are illustrative only and not guarantees of future performance. Investment values can fall as well as rise. Tax rules and pension regulations may change. This article does not constitute as financial advice and you should always seek professional financial and tax advice before making investment decisions.

Content correct at time of writing.

For personalised guidance on Junior SIPPs and family wealth planning, speak to an adviser at Mattioli Woods.

* Inheritance Tax on unused pension funds and death benefits – GOV.UK