Working with clients such as John and Martha is every financial adviser’s dream. Having been diligent savers over the course of their working lives, we have worked together in utilising a range of tax-efficient savings vehicles, allowances, strategies and investments, to ensure they are strongly positioned to generate a tax-efficient income in retirement. Now, at 60 years old, they look to bear the fruits of their labour from their combined portfolio of assets, consisting of the following:

| Pensions | £850,000 |

| Direct investment portfolio | £200,000 |

| Stocks & Shares ISAs | £200,000 |

| Offshore investment bonds* | £450,000 |

| Venture Capital Trusts (VCTs) | £200,000 |

| Total | £1,900,000 |

*Initial investment of £350,000

John and Martha are looking to create a combined net income stream of £80,000 per annum to meet their desired expenditure requirements, with a view of maximising tax efficiency and ensuring sustainability for the long term.

We incorporate some assumptions of future growth rates from the various pots of wealth (these are not guaranteed and are for illustrative purposes only), and consider the position if the investments were to deliver annual returns on the following basis:

| Pensions | 4% |

| Direct investment portfolio | 4% |

| Stocks & shares ISAs | 4% |

| Offshore investment bonds | 5% |

| Venture Capital Trusts (VCTs) | 5% |

To achieve their objectives, we look to take advantage of the following allowances and strategies (based on 2025/26 tax year figures).

Tax-efficient pension withdrawal strategy

With a flexible pension vehicle, individuals have the ability to structure their withdrawals so that for each tranche drawn, 25% is tax free and the balance is subject to the individual’s marginal rate of tax and can be sheltered within the unused personal allowance.

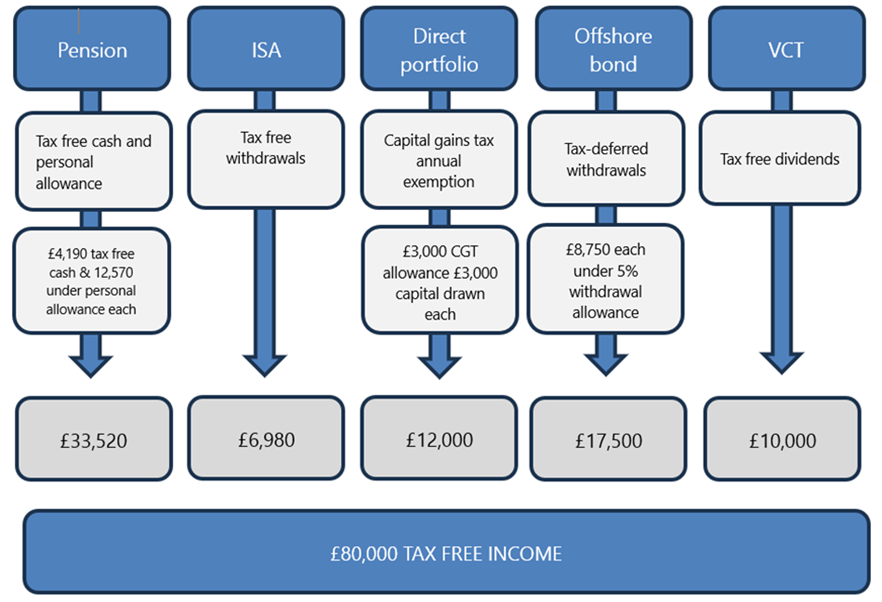

By phasing their tax-free cash with pension income, John and Martha could each draw £16,760 tax free, or £33,520 in total.

Each individual has a personal allowance of £12,570 (assuming they each have their full personal allowance). Any income under this threshold is sheltered from income tax. Of the £16,760 drawn by both John and Martha, 25% (£4,190) is paid tax free and the remaining £12,570 falls within their personal allowance and is also tax free.

As the withdrawal rate here falls just below 4%, we would expect the capital value to remain intact, if not increase slightly over the years.

Tax-free VCT dividends

Dividends from regular stocks and shares are typically taxable on amount over the annual dividend allowance of £500. VCT dividends, however, are completely tax free. With an annual dividend target of 5%, John and Martha could receive a joint £10,000 of tax-free income per annum.

It should also be noted that although VCTs are valuable tax-efficient investment vehicles (which offer tax relief on initial investment, tax-free dividends, scope for capital growth and tax-free capital gains), they are deemed to be higher-risk investments, which are suitable for individuals who have the appropriate capacity for loss to undertake such investments.

Investment bond tax-deferred withdrawals

Investment bond holders can withdraw up to 5% of their original investment for each year the bond has been in force without an immediate tax liability. John and Martha hold investment bonds valued at £350,000 at purchase, and could therefore draw a combined £17,500 for 20 years without incurring an immediate tax liability.

After year 20, tax may be due on withdrawals at their marginal rate of income tax. At this time, we may look to increase the withdrawals from the ISA to maintain tax efficiency. Equally, if the withdrawals can be reduced below the 5% allowance, the investment bonds may be able to provide a tax-deferred income for longer than 20 years (i.e. by withdrawing 4% over 25 years).

Direct investment portfolio withdrawals

Each individual can realise capital gains of up to £3,000 each year without incurring a tax liability. While significantly reduced in recent years, this remains a powerful (and often underutilised) allowance, to take advantage of when drawing down on their direct investment portfolio.

Assuming capital gains account for 50% of the portfolio value, a combined total of £12,000 could be drawn each year tax free. £6,000 of this will be covered under the annual exemption, with the remaining £6,000 treated as return of capital.

The withdrawals from the direct portfolio are greater than the returns being generated and, as such, the portfolio would be depleted over the years. As they will be eligible for State Pension in around seven years’ time, they may have the opportunity to reduce the withdrawals from this portfolio then, to increase its longevity.

Tax-free ISA withdrawals

All withdrawals from their ISA portfolios are free of tax and, therefore, John and Martha can cover the remaining £6,980 by drawing from their ISAs without incurring any tax liability.

Representing a withdrawal rate of 3.4%, the ISA portfolios will continue to grow over time.

In light of the above, we have looked to structure John and Martha’s income as follows:

The above demonstrates how John and Martha can derive a tax-free income for themselves using their various ‘pots’ of wealth. Their income strategy remains flexible and adaptable to changing circumstances. For example, should dividends from their VCTs fall short in a particular year, they can supplement these by drawing additional income from the ISAs, direct investment portfolio or pensions.

Maximising the use of tax-efficient allowances, structures, and investment vehicles means that the underlying investments are not required to work as hard in generating returns to distribute the desired level of income, given they are not hindered by tax.

By combining careful planning with tax-efficient strategies, John and Martha are set to enjoy a financially secure retirement. Their story shows how making the most of tax allowances can help you keep more of what you’ve worked so hard to save.

Should you wish to discuss your long-term income planning, and ensure you are well positioned to derive a tax-efficient income in retirement, please feel free to email [email protected].

Content correct at time of writing (April 2025).

This article was written by Wealth Management Consultant, Max Spencer.

This article has been produced for information purposes only. It is not intended to be an invitation to buy or act upon the comments made. All investment decisions should be taken with advice, given appropriate knowledge of the investor’s circumstances and one must satisfy certain investor criteria before being considered eligible to invest. Any forward-looking statements and forecasted returns represent the current views of Mattioli Woods Limited and may be subject to change. Your capital may be at risk and past performance is not a guide to future returns. Mattioli Woods Limited is authorised and regulated by the Financial Conduct Authority.