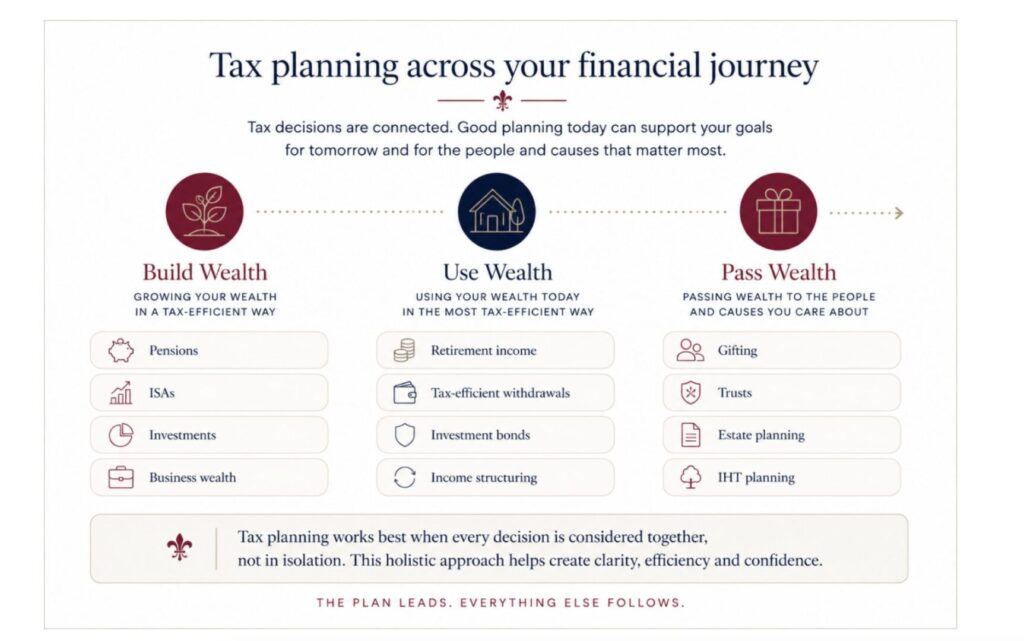

Retirement income planning

How you draw income in retirement can make a significant difference to how long your wealth lasts and how much tax you pay.

We help clients consider how pensions, ISAs, cash, investment accounts and bonds can work together to create sustainable, tax-efficient retirement income.

Investment tax planning

Investments can be structured in different ways depending on your goals, time horizon and tax position.

We can help you consider the role of ISAs, pensions, General Investment Accounts, investment bonds and specialist tax-efficient investments as part of a wider plan.

Inheritance Tax and estate planning

Passing wealth on thoughtfully often requires early planning.

This may include wills, Lasting Powers of Attorneys, gifting strategies, trusts, whole of life insurance, Business Relief investments and wider family wealth planning.

The aim is to help you support the people and causes that matter most, while maintaining your own financial security.

Business owner tax planning

Business owners often face more complex planning needs, particularly around profit extraction, pension contributions, business sales, succession planning and personal wealth structuring.

We help business owners think beyond the business itself and build a plan for the wealth it creates.

Specialist tax-efficient investing

For suitable clients, specialist investments such as VCT, EIS and Business Relief-qualifying investments may support broader tax planning objectives.

These investments can involve higher levels of risk, reduced liquidity and greater complexity, so careful suitability assessment is essential.