The Monthly Market Commentary (MMC), is an update on the world in which we invest. The theme this month is festive films.

Our theme this month is festive films. Intentionally a little more light-hearted as we all need a little levity given the news swirling around as we head for the season of goodwill. Nevertheless, the underlying commentary contains plenty for the serious minded, including any whose first thought here is ‘bah, humbug’. Since we wrote just a month ago, risk assets have been on something of a roller coaster as the threat of a new variant of Covid-19 (Omicron) has hit and very swiftly become headline news.

As we have seen in the more than 20 months since lockdowns first hit the UK, the reaction in equity markets (in particular) has been driven by how investors see the respective sectors (and then individual stocks), rather than throwing the baby out with the bathwater (other than perhaps right at the start in March 2020). Travel and hospitality are again facing the worst of the Covid-19 weather, while tech-enabled retailers and broader services are less affected.

As we finished the November Commentary, we expected an interest rate rise from the Bank of England in their December Monetary Policy Committee meeting (mid-month). Now, as you will read below, that is far from certain, with market expectations falling from 75% certainty to just a third. Indeed, it seems likely that central banks worldwide will be putting a pause on monetary tightening until more is known about the Omicron variant.

In the current investment climate it is unclear whether equity investors will greet a delay in rate hikes positively by buying risk assets, or whether they will interpret the delay as a negative comment on the economic outlook, and sell stocks, high yield bonds, etc. and run for the hills (defensive asset classes).

Next year is likely to see an ever-closer normality set into economic news flow and market returns as the recovery slows and shortages resolve themselves, enabling inflation to come down. The strong stock market returns seen (so far) this year seem unlikely to be repeated next year. Fingers crossed that we end the year calmly and that there is no investment Nightmare Before Christmas!

Remaining cautiously positive for equities feels about right, and we have been more positive on the UK in particular during 2021 than we have been for a long time. Events and news continue, as ever, to have the potential to knock that off course. While we are positive longer term, the new variant, and concerns around quite what we will all face in the coming weeks/next few months as regards restrictions, threaten to take the gloss off the festive period. Keep smiling.

Term or word(s) to watch: platinum – of great interest to many due to its use in catalytic converters (very much a topic you can expect to hear and read more about in the coming months) but also as we look forward to 6 February 2022 – the 70th (and therefore platinum) anniversary of HM Queen Elizabeth II’s ascension to the throne. Platinum’s price has rather been in the doldrums since early February – the price then, hitting $42 a gram, seems a long way off as the latest read is close to $30 a gram.

Meanwhile, official (and unofficial) Platinum Jubilee memorabilia looks sure to fly off the shelves, and the planned celebrations, including extended national holidays, may just be what we need to deliver some momentum into the British economy in 2022. Here’s hoping the health of all concerned holds up and we can look forward to some full-blown celebrating and simultaneous nostalgia in the months ahead.

November saw the US Federal Reserve (Fed) meeting where it was announced that the pace of its purchases in the bond and mortgage markets would be cut by $15 billion a month. Along with the substance of this announcement – which suggests the economy needs less help – the language surrounding the central bank’s announcements remains closely watched by markets to try to garner insights into future policy changes.

In particular, the language surrounding inflation has been of interest. US inflationary pressures are near 30-year highs and since November last year the Fed has been stating that the pressures are ‘transitory’. Since the November meeting of the Fed’s Open Market Committee (FOMC), which sets policy, Chairman Jerome Powell has indicated that the term ‘transitory’ was no longer appropriate given its short-lived impression. In other words, the Fed’s meaning of it not leading to a permanently higher inflation rate was preferable.

At the same hearing Powell suggested that December may see the FOMC further taper their bond buying programmes, which is quicker than markets were expecting and could lead to earlier rate hikes than has been anticipated. Of course, the re-emerging public health concerns over the Covid-19 Omicron variant may yet force these plans to change.

The 1947 film Miracle on 34th Street follows the story of a department store Santa Claus who claims to be the real Chris Cringle and eventually ends up in court. The festive film (Christmas time story) was perhaps surprisingly released in June rather than in the run-up to Christmas, with studio head Darryl F. Zanuck insisting it be released in summer as more people go to the cinema in warmer weather.

Away from the central bank, US lawmakers passed a $1.2 trillion bipartisan infrastructure bill in November, with further tests on the horizon. As this commentary was being written, a short-term government funding bill was passed, effectively keeping the government running through to 18 February next year and avoiding a Christmas shutdown. This buys the Democrats time to pass a debt ceiling bill, which needs to occur before 15 December. The Democrats are also trying to pass their social security package, with Democratic Senate majority leader Chuck Schumer publicly stating they would pass this by Christmas, although political divisions within the party may make it difficult to accomplish.

The Fed’s actions continue to be watched by investors, with noises suggesting that an increase in rates has been brought forward. Public health issues may yet impact this, and while it is always noisy, US politics has the potential to create unwanted surprises. We still like US equities, although some areas look overvalued, so we prefer a value tilt to any direct exposure, and indirect exposure through our thematic holdings.

We now know that Olaf Scholz will be the next German Chancellor, and he and the incumbent, Angela Merkel, have announced plans to tighten curbs on the unvaccinated in the country. This is seen as a move towards introducing mandatory vaccinations next year as infection rates increase and vaccination rates stall. The emergence of the Omicron variant has come at a dreadful time for central Europe as it contends with a serious ‘fourth wave’ of the virus and health systems remain under considerable strain.

We know little about Omicron at the time of writing, but the EU health agency has warned it could account for half of all infections in a few months – an arresting prospect considering the current situation. Austria has already had to push the panic button and imposed another round of lockdowns.

Meanwhile, the European Central Bank is under pressure. Inflation in the eurozone hit 4.9% in November, which is the highest level since the creation of the single currency. Voices of concern are growing (not least in Germany) that the situation is becoming serious and that action will be needed soon. If it arrives it will probably take the initial form of a reduction in the bond buying programme as the reluctance to tighten seems pretty ingrained.

Difficulties posed by the new variant are likely to create additional supply pressures, but the recent reduction in energy prices should bring some degree of relief. In the face of an unwillingness to move on policy, the euro has been weak relative to most currencies; this provides an unhelpful headwind for the region’s exporters.

Relative to the US market, Europe looks attractive in terms of valuation but then doesn’t everywhere? A better argument for the region is the sectoral composition of the indices – the skew is much more towards cyclical and value names than the growth-oriented sectors of the US. There are many uncertainties at the moment; ultimately, it looks as if the cyclical recovery post Covid-19 will continue and Europe should fare well against this backdrop.

Joyeux Noël is based on the Christmas Truce during World War I in which soldiers from all sides came together in peace at Christmas. The story is told from the French, Scottish and German perspectives and was nominated as best foreign language film at the Academy Awards, BAFTAs and Golden Globes.

Plenty of challenges, but no changes for us here. A quick reminder – it is not only the UK that has been suffering from supply/pricing issues, from transport to energy, and more – Europe has her fair share of challenges.

Overseas investors turned net buyers of Japanese equities in November having been sellers the previous month. This is partly because two of the major domestic buying ‘forces’ are weakening in potency. This dynamic is going to be important for the fortunes of the Japanese market and in determining whether our allocation proves to be a winner for portfolios.

First, the Bank of Japan has been buying ETFs and now owns around 5% of the market – but they essentially stopped this exercise earlier in the year. Second, the Government Pension Fund has reached its target of holding 25% of assets in domestic equities. So, a fair bit of demand needs to be replaced.

There are good reasons to suspect that overseas investors will pick up the slack. We have previously discussed the valuation case at length and using most key metrics this is solid. If we do see a period of uncertainty in markets, possibly from the difficulties posed by the new variant, then the yen is likely to prove a haven (this often happens in times of market stress), meaning Japan will look attractive for international investors.

This said, Japanese exporters might find the going tougher. If value or safe haven arguments aren’t sufficiently compelling, we have the genuine dynamic of corporate change, which should prove helpful. Under Abenomics, this was seen as one of the key drivers of equity market reform and it seems to be gaining traction despite Abe’s departure. Recent changes at Toshiba point in this direction and there has even been a pickup in takeover activity caused by investor agitation over corporate structures.

Anime, the Japanese animated art form, has produced several major Christmas-related films. Would Christmas really be Christmas without settling down with a mince pie to watch Tokyo Godfathers, in which a middle-aged alcoholic named Gin, a transgender woman named Hana and a runaway girl named Miyuki discover an abandoned newborn while searching through the garbage for presents?

Exposure to this investment story seems to be at around the right level in portfolios from our positive perspective (we see value here).

What do celebrities, casinos and Taiwanese companies all have in common? Well, all three were in the Chinese Communist Party’s crosshairs last month, as it continues to focus on instilling ‘Chinese values’. With the 20th National Party Congress scheduled for 2022, President Xi Jinping is carefully laying the foundations for an unprecedented third term in power.

It seems that a central tenet of long-lasting power in China is control, and in November the ruling party launched a campaign to get 85% of citizens speaking Mandarin by 2025, stating that the current use of the language is ‘unbalanced and inadequate’. The move threatens regional dialects and is yet another sign of the oppression faced by ethnic minorities. Outside of the mainland, both Taiwan and Macau are increasingly under pressure to tow the party line. In Taiwan, corporate donors to pro-independence groups have faced hefty fines and face being added to a blacklist of companies that are prohibited from making money from the mainland.

A potential crackdown on the Macau casinos also appears to be in the offing, with shares in the sector falling sharply following the arrest of one chief executive. The Cyberspace Administration of China also announced a crackdown on celebrities and their fans, due to the ‘chaos’ that online groups can create and their tendency to promote ‘extravagant pleasure’. Both moves are yet more evidence of the push towards reforming social values and promoting ‘common prosperity’ within the country.

Understandably, this has led some to become hesitant around the future growth potential of listed Chinese investments. Such draconian measures beg the question whether companies in China can truly be run for shareholders, when keeping on the right side of the ruling party is so vital to their survival. Arguably, we are seeing this hesitancy starting to play out domestically. Public listings of technology firms in mainland China look set for their first annual drop in seven years, according to data from Dealogic. Compare that with a 550% increase in India (by value) and it brings into question whether CEOs dare put their head above the parapet and subsequently into the public eye.

The 2013 film, Xmas Without China, is a US comedy telling the story of a US family that tries to have Christmas without any Chinese-made products. It certainly sounds like a challenge, but possibly also a political statement, or are we reading way too much into it?

China remains a key source of debate within the team. We employ expert, active fund managers to manage our client’s money in this space and we believe their local insight and knowledge is invaluable in what is a highly complex market. The recent direction of travel from the Chinese Communist Party is concerning, though we feel we currently have the potential to be appropriately rewarded for the risks involved. We continue to assess that risk–reward profile on an ongoing basis.

It has now been 20 years since a Goldman Sachs paper coined the term BRIC to describe the collective economies of Brazil, Russia, India and China (with South Africa added to form BRICS in 2009), with much hype, forecasting that these nations could become larger than those of the G7 (group of developed economies). There was great excitement about the prospect for this group, with many BRIC investment products being launched, despite the vast differences between the economies, most notably Brazil and Russia being heavily reliant on commodities and India and China more on domestic growth.

The 1976 Soviet romantic comedy The Irony of Fate is still considered to be one of the classic festive films in Russia and other post-Soviet states. The film’s plot occurs because of the grim uniformity of Brezhnev-era architecture that saw functional, identical multistorey apartment blocks built in many cities. After a boozy New Year’s party in Moscow, our protagonist is mistakenly put on a plane to Leningrad where due to a street with the same name and identical buildings he drunkenly goes to sleep in someone else’s apartment causing quite the palaver the next day.

It is fair to say this acronym has not seen the stellar outperformance anticipated at the time, with the four nations behind developed markets over the last decade and the post-pandemic outlook (ex-China) being for weaker near-term growth. Neither of the economies of Brazil and Russia have grown in significance as a share of global growth over the last 20 years, and while the potential remains for the urbanisation and emergence of a strong middle class, it is very difficult to see a catalyst to unlock this potential.

China has been the best performing of the four and has generally met its own growth targets and seen a greater shift to a consumption-based economy, but its place on the global stage has seen conflict with the US. India has also been a good performer, although she has kept pace with expectations rather than shooting the lights out.

The story of the BRIC economies over the last 20 years has been one of potential not being fully unlocked, particularly for the BR part of the acronym. This acts as a reminder that a good story does not always make a good investment case and those emerging markets are not all equal, despite being put together as an asset class. We broadly have allocations to India and China equities, being careful on the ESG risks of the latter, and wider emerging Asia over other areas of emerging markets. We do have selective broad emerging market exposure for higher risk clients through funds that we see as picking the best companies across the set, rather than betting on any one country.

You might think that healthcare would have been one of the main beneficiaries of news developments over the last two years. Awareness of the importance of healthcare is clearly high among both the public and investors, and some companies directly involved in the development of Covid-19 drugs have done astronomically well. It might surprise some then that healthcare has actually lagged the other sectors in global equity indices. Of course, we have seen this phenomenon before, usually caused by political pressures in the US.

This time round, Democrats are trying to reduce the cost of medicines by enabling Medicare and Medicaid to negotiate with drugs companies. Obviously, this uncertainty will create a headwind for drug manufacturers, but this is far from the only opportunity set within healthcare.

Some of the advances within biotech are truly astounding and the development of Covid-19 vaccines owes a lot to them. This is cutting edge stuff but there are more mundane opportunities too – ageing populations make homecare provision incredibly important and video consultation centred companies may find themselves well placed.

Clearly some of these new discoveries and modes of provision will merely replace existing ones, cannibalising existing revenue streams and thus making picking the winners difficult. This is one of the reasons we only use the very best specialist fund managers who have consistently proved themselves to be skilled at identifying winners.

Research indicates that watching Christmas films is good for your health. Studies by psychologists have suggested that the feel-good nature of the films helps to release dopamine. Probably not sufficient a justification to watch Home Alone 2 though.

Healthcare allocations are well established in our portfolios – the main issue for more adventurous investors is what degree of biotech exposure to incorporate. We see this as a long-term theme.

This continues to be a very difficult space to navigate. The persisting inflation concerns have inevitably had an effect here, though the exact nature of it has wrong-footed some. The market still thinks that inflation will be an issue in the short to medium term (as does the Fed, having ditched its use of the word ‘transitory’) but that it will be contained in the long run.

Consequently, yields have been affected most at the short end of the yield curve and this was reinforced after the latest Fed comments. Several central banks have started to increase rates in response to the inflation data while others are stalling or announcing more gradual approaches (tapering etc.).

Emerging markets yet again find themselves in a tough position in this regard. Many do not want to imperil their economic recoveries, but if the US tightens policy, they are forced to defend their currencies given many of them have external dollar denominated debt to contend with. Not ideal. Turkey represents the real outlier here. As inflation continues to soar, President Erdogan is adamant that in fact higher rates contribute to inflation rather than control it, which seems like a recipe for disaster as the country’s economy deteriorates.

Returning to our theme, who can forget the film Neşeli Hayat (‘Jolly Life’), the Turkish film about a man who takes on a job as Santa in a mall. Strangely enough directed by a certain Yilman Erdogan!

The unpredictability is of course compounded by the developments regarding the new variant. It would seem likely that this will delay monetary tightening, but it could add to inflationary pressures via supply issues creating a real headache for central bankers. Whatever the ultimate outcome, it seems there might be life in Treasuries yet. Having made our initial moves to reduce fixed income, we didn’t see any further changes being warranted in November.

The Omicron variant may have stolen the headlines recently, but the gas shortage that caused so much concern a couple of months ago still hasn’t subsided. Prices remain elevated as investors continue to fret over supply issues. In October, President Putin ordered Gazprom to fill its facilities in Germany and Austria, boosting hopes that exports to Europe would rise causing prices to fall. Since then, some have questioned whether Russia has in fact diverted existing flows to these facilities, instead of increasing flows to Europe. With prices high, Russia and its allies continue to use supply as leverage for wider diplomatic discussions. Indeed, President Lukashenko of Belarus has vowed to cut supply to the EU if sanctions against the country in relation to the migrant crisis are escalated.

The situation was not helped by the decision of the German energy regulator to temporarily suspend certification of the delayed and maligned Nord Stream 2 pipeline in November. As a reminder, Nord Steam 2 is a pipeline that remains a lightning rod for political tensions, with the controversial project ramping up Russian gas exports to Europe. The latest hitch comes as a result of technicalities around the establishment of a subsidiary that has not met German legal requirements. This process and associated approval from the EU could take up to six months, dashing hopes that sign-off could be completed this winter.

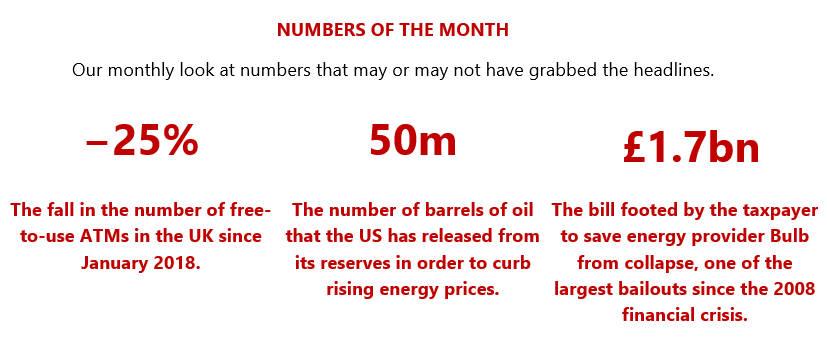

Of course, politicians in Moscow and across Europe will be acutely aware of the wider social and economic impact of higher gas prices. In the UK, taxpayers have funded a £1.7bn bailout of the seventh largest energy supplier, Bulb. The bailout is one of the largest of its kind since the rescue of RBS and HBOS in 2008.

One analyst (at Investec) estimates that the cost of rescuing the circa two million customers affected by corporate failures since August will add £75 to dual fuel energy bills for UK households. The shortage also has significant implications for food prices, with fertiliser production hampered and prices spiralling. While farmers can temporarily lower usage, the move could have a significant impact on long-term yields and prices.

Movies set around Christmas time are often considered Christmas (festive) movies (films). One such is Batman Returns, in which businessman Max Schreck plans to build a power plant for Gotham. Aided by supervillain, The Penguin, Schreck’s is no ordinary power plant and plans to drain Gotham of its energy, leaving the city under his control. There is only one man for the job, and he doesn’t have any reindeer to help (just a Robin).

We retain our conviction in gold, which has the ability to provide protection in these uncertain times. Broad mining remains an area of investment for our more risk tolerant investors.

The emergence of another disruptive Covid-19 variant is enough to cause further concerns in the property space. Although it has rallied very strongly there are still question marks over the demand for office space and the long-term outlook for the asset class. Demand for prime office property is London is very strong but secondary offerings are going to find things much tougher. At least 80% of the UK market is secondary in nature and encouraging tenants is going to prove challenging given the move to working from home for many.

Whether the sector will be the beneficiary of private equity money is uncertain (this is usually focused more on prime property), but it could be material.

Aside from these concerns, owners of commercial property also have to contend with the challenge of meeting new environmental requirements by 2030. Meeting new efficiency targets will be too much for some, which is likely to act as a drag on valuations as properties are offloaded to those with the resources to acquire and then meet the new regulations. Predictably, we are already starting to see the emergence of investment vehicles that will seek to acquire properties where, because of the required capital outlays, the landlords are in some degree of distress.

The issues presented by the new environmental regulations are significant and we ensure that all of the fund managers we employ are addressing any potential exposures within their portfolios. Property faces its challenges for sure, but our current holdings look justified at these levels.

Inflation has been stubbornly low for the best part of a decade. Though it is increasingly talked about in relation to supply chain shortages, could the move to a more sustainable economy be a structural driver for inflation for years to come? It is certainly a question we have been asking ourselves for a while now. Investors are increasingly looking to invest in firms that ‘do the right thing’. However, ‘doing the right thing’ can come at a cost.

One reason that inflation had been so low prior to Covid-19 was because wages hadn’t moved a great deal. However, we are starting to see that change. It isn’t simply because of labour shortages; companies are increasingly willing to pay ‘the living wage’. Indeed, over half of the UK’s largest companies have committed to paying all employees and contractors in their supply chain an hourly rate that is higher than the statutory minimum.

Another source of expenditure comes in the form of property, and landlords could face hefty capital expenditure bills in order to make their assets more efficient. As mentioned in the previous section, the minimum energy efficient standards (MEES) regulations state that all non-domestic buildings will need an EPC rating of C or above by 2027 and B or above by 2030. According to a report by IPSX and Carbon Intelligence published earlier this year, 90% of EPCs on the national register are below B. Clearly higher spending on refitting our properties and wider infrastructure to meet environmental standards could create significant inflationary pressure.

Finally, how about consumer habits? Well, many consumers are willing to pay higher prices to reduce their impact on the environment. Albeit from a low base, the growth in electric vehicles appears relentless. Sustainable fashion is another growth area, with The Business Research Company predicting a compound annual growth rate of 9% to 2030. Indeed, according to their 2020 survey, 66% of respondents said that they consider sustainability when purchasing luxury products. Again, consumers being willing to spend more on clothing and other items to ensure product sustainability helps support the case for a period of structural inflationary pressure, driven by a desire to ‘do the right thing’.

Perhaps these higher costs will eventually be offset by lower energy prices from renewable sources and lower costs associated with externalities. However, in the short to medium term, it appears that meeting the goals set by governments and corporates requires higher levels of spending and could provide a tailwind to inflation for years to come.

What currency does Father Christmas (Santa Claus) use? It turns out that far from being a cracker joke, this is a question to which the mine that is Google says there are more than 276 million possible responses (many of which are pretty vaguely connected, it has to be said).

In the US, you can buy a Santa Dollar, which is simply a $1 note with a charming sticker over the image of George Washington, which when peeled off leaves the $1 note as, well, worth a dollar. In ‘circulation’ (they are legal tender) since 1985, it seems that most are in fact kept, rather than spent. Elsewhere, we suspect goodwill is essentially the big man’s main currency and we hope it will be spread far and wide this festive season.

The Monetary Policy Committee of the Bank of England meets more than a week after we publish this month, to agree the UK’s base interest rate – and so much has happened since they last decided (7–2) to leave the historically low 0.10% in place … and yet one main issue has not changed at all – the threat of inflation becoming more than transitory.

The rise of the Omicron variant and resulting slap in the face for a continued recovery comes just as consumers were planning to once again spend, spend, spend. Where’s Viv Nicholson when you need her? Well, while it’s not like the 1960s in too many respects, our modern era of low interest rates does seem to be likely to be extended, as surely the grandees at the Bank will take account of the hit that a resumption of many restrictions will have on demand, even as supply side issues are perhaps beginning to improve. It really could go either way, but don’t be surprised by another ‘no change’ decision.

The Monthly Market Commentary (MMC) is written and researched by Simon Gibson, Richard Smith, Scott Bradshaw, Jonathon Marchant and Lauren Wilson for clients and professional connections of Mattioli Woods plc, and is for information purposes only. It is not intended to be an invitation to buy, or to act upon the comments made, and all investment decisions should be taken with advice, given appropriate knowledge of the investor’s circumstances. The value of investments and the income from them can fall as well as rise and investors may not get back the full amount invested. Past performance is not a guide to the future. Mattioli Woods plc is authorised and regulated by the Financial Conduct Authority.

The MMC will always be sent to you by the seventh working day of each month, usually sooner, is normally delivered via email, and is free of charge as the MMC is generally made available to clients who have assets under our management in excess of £200,000, and to all clients under our Discretionary Portfolio Management Service (DPM). Normally, the MMC costs £397 + VAT per annum. Professional advisers and their clients should contact us if they are interested in receiving a monthly copy.

Sources: www.bbc.co.uk, www.bloomberg.com, Financial Express, www.thedragonsblade.com, www.express.co.uk, www.pitstoppin.co.uk, www.sibcyclinenews.com, www.vr-12.com, www.smalltalkbigresults.wordpress.com, www.anonw.wordpress.com www.avantida.com, www.plazmedia.com, www.viewzone.com, www.mmn.com. All other sources quoted if used directly; except fund managers who will be left anonymous; otherwise, this is the work of Mattioli Woods plc.